One of the most intriguing facets of financial markets of the past two years has been the differing messages offered by bond yields and share prices. The bond market, via the so-called inverted yield curve, has been predicting a recession. The stock market has instead priced in a cooling in inflation, a gentle economic landing and a pivot to interest rate cuts from central banks, with the result that headline equity indices from America to Australia, France to Taiwan and Canada to Germany have set new all-time highs.

“Usually, the yields on long-term bonds are higher than those on short-term paper. This is simply because lenders (or bond buyers) demand a higher return to compensate themselves for the increased scope for something to go wrong during the additional time, such as changes in interest rates, higher inflation or, at worst, a default by the issuer (or borrower).”

Usually, the yields on long-term bonds are higher than those on short-term paper. This is simply because lenders (or bond buyers) demand a higher return to compensate themselves for the increased scope for something to go wrong during the additional time, such as changes in interest rates, higher inflation or, at worst, a default by the issuer (or borrower).

The usual shape of the yield curve therefore goes from the bottom left of a screen to the top right, in a gently steepening path.

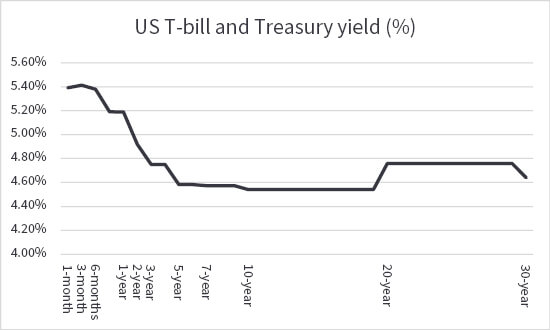

The US yield curve currently has the hump

Source: LSEG Datastream data

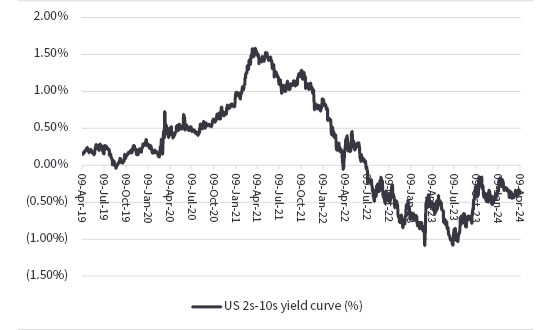

An inverted curve means long-term rates are lower than near-term ones. This means markets think that interest rate cuts are coming in response to a slowdown or recession. A shorthand version of this can be provided by comparing just the yield on two- and ten-year government bonds.

The US yield curve is starting to steepen and become less inverted

Source: LSEG Datastream data

“But the yield curve changes shape according to variations in the yield on each individual maturity, as it flattens or steepens, and there are four possible scenarios here.”

But the yield curve changes shape according to variations in the yield on each individual maturity, as it flattens or steepens, and there are four possible scenarios here:

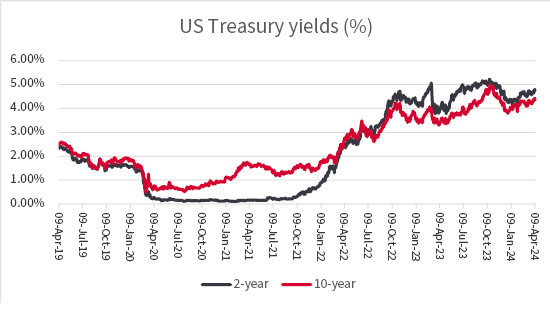

“Right now, we have a bear steepener on our hands in the USA.”

Right now, we have a bear steepener on our hands in the USA.

The US yield curve showing a ‘bear steepener’

Source: LSEG Datastream data

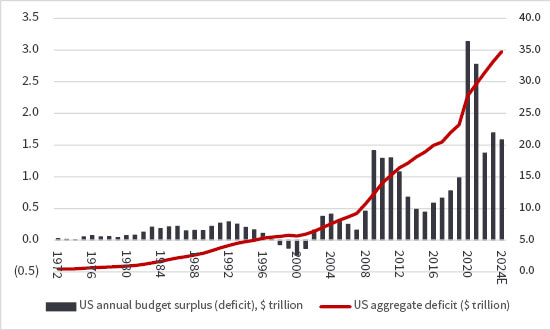

If the US economy slows down, then there could be trouble ahead for equities. But given the amount of fiscal stimulus being applied, that does not seem so likely for now, almost irrespective of who wins the US presidential election in November. The issue at hand could therefore be inflation instead, especially as the Biden administration is on course to add $7 trillion to America’s national debt during its four-year term (and the total deficit only reached that level for the first time in 2003).

America’s federal deficit continues to rocket

Source: LSEG Datastream data, FRED – US Federal Reserve database, Congressional Budget Office

That does not mean it is game over for the stock market’s bull run. It could mean a more difficult environment for bonds and yield-offering bond proxy stocks like utilities and consumer staples. It could mean a more difficult environment for long-duration sectors like tech and biotech. It could mean a more interesting environment for companies with pricing power and also commodities, if investors repeat the 1970s’ strategy of looking toward ‘hard assets’ as a store of value relative to paper ones, such as cash and bonds, the real value of which may be eroded by the ravages of inflation.

“The bond market could just be flat out wrong. It has wrongly been predicting a recession. It is now predicting inflation. But the signals emanating from bonds still do not sit easily with the equity markets’ preferred narrative of cooling inflation, slow growth and interest rate cuts.”

The bond market could just be flat out wrong. It has wrongly been predicting a recession. It is now predicting inflation. But the signals emanating from bonds still do not sit easily with the equity markets’ preferred narrative of cooling inflation, slow growth and interest rate cuts. Someone is going to be wrong somewhere.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.