Aficionados of British pop music in the late 1960s and early 1970s may well remember The Move, a band perhaps best known for their only chart-topping single, Blackberry Way (even if one of the group, Roy Wood, eventually went on to form Wizzard and record a song that has received guaranteed airplay ever since, namely I Wish It Could Be Christmas Everyday).

But the MOVE index – or the Merrill Lynch Option Volatility Estimate to use its full name – is more than capable of striking a chord or two of its own, at least from the perspective of financial markets.

The MOVE can help advisers and clients gauge current sentiment from the perspective of the bond market and even stock markets, given how influential yields in the former are across the latter. The good news, for the moment, is the MOVE is not offering too much by way of movement at all

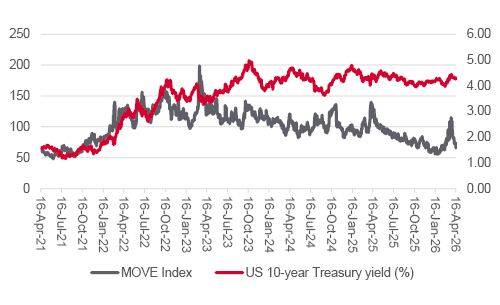

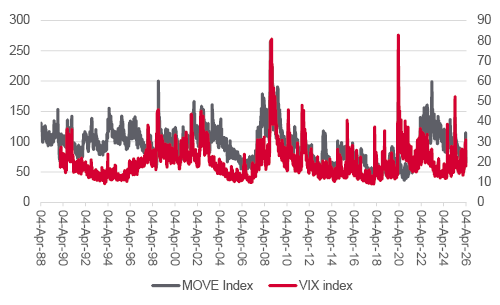

The MOVE index is the US government bond (or Treasury) market’s version of the US stock market’s VIX index. The VIX (also known as the ‘Fear Index’) tracks market expectations for volatility in equities, and the MOVE does the same for Treasuries and the fixed-income markets. Given the size of the US federal debt, and therefore the US bond market, and the importance of US Treasury yields as a reference point for the risk-free rate, advisers and clients may wish to keep up with the MOVE’s mood.

In crude terms, the higher the MOVE goes, the more nervous fixed-income investors are, and vice-versa, just as is the case for the VIX. In the latter case, extremely high readings can suggest that panic is taking over, sentiment is washed out and it may be a chance to buy and pick up bargains. Conversely, extreme lows can imply complacency and mean that it may not take much to cause an equity market correction.

A similar rule of thumb looks to apply to the MOVE, too. For example, when America and Israel launched their first military assault on Iran on the weekend of 28 February, the MOVE spiked and so did US Treasury yields, especially at the longer end of the yield curve.

Source: LSEG Refinitiv data.

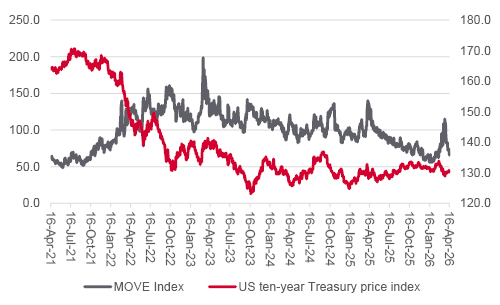

That, in turn, meant that Treasury prices fell. Fixed-income markets fretted over whether the war would lead to both higher inflation and higher US federal deficits, thanks to oil and gas price increases in the case of the former, and worries about to a hit to the American economy in the case of the latter, as a result of how tax revenues could fall and welfare spending rise.

Source: LSEG Refinitiv data.

However, such worries have started to dissipate.

The VIX jumped to 31.1 from 19.9 as the war developed. But history suggests the ‘Fear Index’ needs to go above 40 before share prices start to wobble in earnest, and it is already back below 20, at the time of writing, a mark that is barely above its long-term average. In plain English, the US stock market thinks the war will be short-lived and its after-effects limited.

The MOVE index broke briefly above 100, up from 73.4 upon the start of the conflict. It now stands at 66, some way below its lifetime average of 93 and its pre-war starting point. The US sovereign bond market may therefore be saying that the commencement of talks between Washington and Tehran, no matter how convoluted and initially unsuccessful, means the worst of the military conflict is already behind us.

Source: LSEG Refinitiv data.

The lack of fear in equities or movement in bonds is a telling combination. Major shifts in the MOVE have proved particularly telling when the VIX has travelled in the same direction shortly afterwards. Prior instances of this include 1994’s Fed interest rate shock, the emerging market debt crisis of 1998, the Great Financial Crisis of 2007-08 and the US Federal Reserve’s shift to tightening monetary policy in 2022 after inflation finally broke out in the wake of the Russian attack on Ukraine.

Note how unexpected changes in monetary policy, or a perceived loss of central bank control, all prompted the MOVE and the VIX to rise from (overconfident) lows.

Financial markets have reined in expectations for rate cuts from the Federal Reserve, from two or three to none for this year, with maybe one by Christmas 2027, according to the CME Fedwatch service, owing to fears of an oil price shock.

The key therefore now is whether the Fed, under chair-elect Kevin Warsh, feels that circumstances will permit a loosening of policy after all, in which case the MOVE and VIX may both decline to signal further upside in share and bond prices, and drops in bond yields.

Equally, a long war, or protracted, unsuccessful peace talks and sustained increases in the price of oil, gas and fertiliser, and thus higher inflation could limit the US central bank’s room for manoeuvre, with increases in the MOVE as an early warning sign of a potential monetary policy dilemma as well as a fiscal problem, should US federal growth accelerate.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.