Any client who seeks income, or is of the opinion that cash remains king, could be forgiven for casting a covetous eye at the UK stock market, for all that London continues to attract criticism for lacking the glamour, valuation, or deal flow of some of its global counterparts.

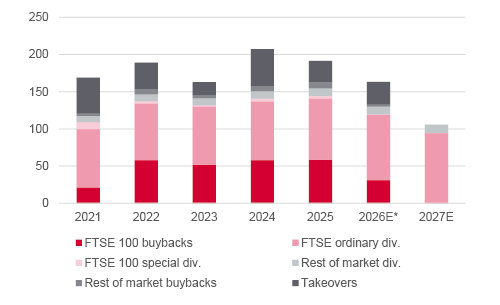

The combination of ordinary dividends, special dividends, share buybacks and takeovers means that the UK market is already set to return £163 billion to equity investors this year, a figure that equates to a 5.8% ‘cash yield’ on the FTSE All-Share.

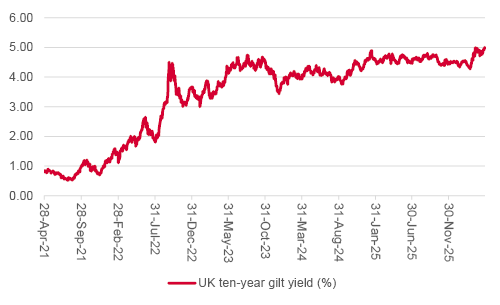

That figure easily beats the Bank of England base rate, the prevailing rate of annual rate of inflation, based on the consumer price index, and also the benchmark ten-year gilt yield, to perhaps suggest the UK is not the dullard it is perceived to be.

Advisers and clients are unlikely to have the time to get involved in the practical details of individual stocks, but they may be intrigued to learn that a fourth member of the UK’s elite FTSE 100 index is now the subject of a bid.

The putative approach for Irish energy specialist DCC, made by two American private equity specialists, Energy Capital and KKR, comes after offers for Schroders, Beazley, and Intertek. Two further members of the benchmark, miners Rio Tinto and Glencore, briefly held merger talks at the start of this year, too.

All of these deals are yet to close successfully, but the wave of merger and acquisition activity suggests that the UK equity market continues to offer value, judging by how prospective trade and financial buyers from home and abroad seem keen to snap up London-listed companies.

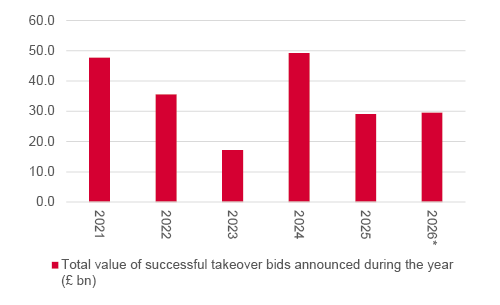

Of the twenty-one bids tabled so far this year, fifteen have a firm offer attached to them, with a total value of £29.7 billion. This sum already exceeds the total value of all successful bids made in 2025 and the other six targets yet to receive a set price have a combined stock market valuation of £7.6 billion between them.

Source: Company accounts. *2026 based on all live bids announced as of 29 April, most of which are yet to close.

But it is not just the pace of deal-making that catches the eye. The price paid is notable, too.

The average takeover premium on all of the deals tabled so far in 2026 is 39%.

That does not quite match the 52% and 47% average uplift gratefully banked by shareholders in 2023 and 2024 respectively, but it stands up well to the averages posted in 2021, 2022 and 2025, despite substantial gains in the UK’s headline equity indices over that period.

Source: Company accounts. *2026 based on all live bids announced as of 29 April, most of which are yet to close.

The £29.7 billion in cash, or cash-and-stock, bids that is already on the table this year equates to just over 1% of the FTSE All-Share’s stock market capitalisation.

Analysts’ consensus forecasts suggest that the FTSE 100’s members are primed to pay out £88 billion in ordinary and special dividends this year, and the FTSE All-Share some £98 billion in total. That is 3.5% of the FTSE All-Share’s market cap.

The FTSE 100’s members have also announced share buyback plans worth £32.1 billion, with another £3.4 billion declared by other UK-listed companies, a further 1.3% of the UK market’s valuation.

Add up those and the £163 billion total cash return comes to ‘cash yield’ of 5.8% on the FTSE All-Share.

Six more takeovers could add at least £7.6 billion to that and there is scope for further bids and buybacks as the year goes on.

In this respect there is scope for further upside in UK equity market cash returns and 2024’s record aggregate return from dividends, buybacks, and takeovers of £207 billion could be within reach.

Risks do remain all the same.

First, any escalation of the conflict in the Middle East could drive oil and gas prices higher still, hit trade flows, burden companies and consumers with extra costs and ultimately crimp global growth. A slowdown or recession could persuade companies to conserve rather than distribute cash.

Second, some FTSE 100 firms have paused their share buyback programmes as they digest acquisitions. Animal spirits in British boardrooms could mean acquisitions take precedence over cash returns.

Finally, advisers will have to keep an eye on inflation and the ten-year gilt yield.

Source: LSEG Refinitiv data

A sustained period of strength in oil and gas, or disrupted global supply chains, could stoke inflation – and the higher inflation goes the greater the challenge to corporate profits, and also the benchmark it provides relative to the total UK cash yield.

Higher inflation could also push up the ten-year gilt yield, the proxy for the so-called risk free rate, and the closer that gilt yield gets to the equity cash yield, the more attractive gilts may start to look as an alternative to equities, especially if a difficult global macro backdrop prompts any bouts of wider risk aversion.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.