The UK is the world’s sixth biggest economy, third biggest individual stock market and arguably still punches above its weight in terms of global geopolitical influence. It has a track record for excellence in the creative media, life sciences, and technology (despite all the worrying, the UK ranks second all-time in the list for total Nobel Science Prizes since 1901 and the University of Cambridge has more all on its own than France).

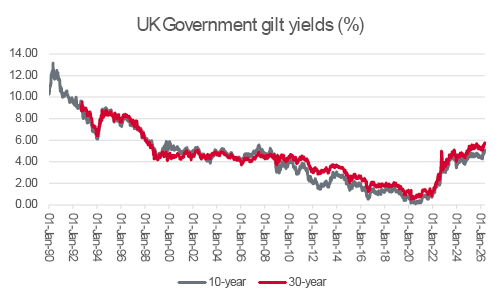

Yet the Government bond, or gilt, market is not having any of it. The benchmark ten-year yield stands above 5.00% for the first time since 2008 and the 30-year is at levels last seen in 1998.

An uneven economic outlook, heavy sovereign debt burden, and a further round of political turbulence in Westminster all explain bond markets’ sceptical view and demands for such a lofty yield. Advisers and clients now have the chance to decide whether the yields on offer are sufficient compensation for the risks and what portion of a balanced portfolio can be allocated to fixed income, and UK sovereign bonds in particular.

A ten-year yield of around 5.00% should not necessarily be a reason for dread. UK Government ten-year paper yielded between 4.50% and 5.50% for most of Tony Blair’s ten-year stint in office as a Labour Prime Minister. The economy ticked over nicely and the FTSE All-Share rose by two-thirds during that spell, even though the 2000-2003 bear market did a lot of damage in Blair’s second term.

Yet there are differences between then and now.

There are further additional complications, notably a prevailing rate of inflation that exceeds the Bank of England’s 2% target every month bar one since August 2021. That has forced the Old Lady of Threadneedle Street to finally take interest rates up from all-but-zero and obliged the Monetary Policy Committee to start to sell gilts under Quantitative Tightening. The danger of the war in the Middle East further fuelling inflation, thanks to higher oil prices and second-round effects from fertiliser, food, and other sources, also lingers.

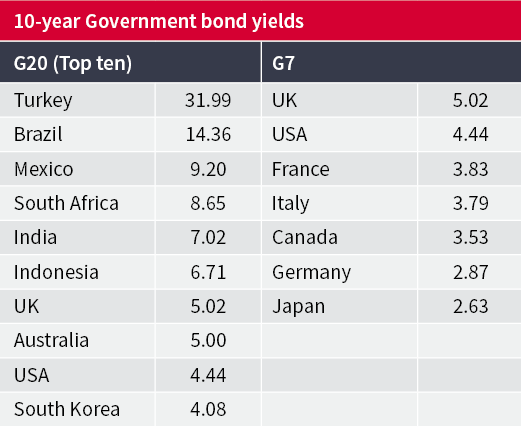

Given such circumstances, it is easy to see why fixed-income investors take such a dim view of the UK. Britain has the seventh-highest borrowing costs within the G20, as benchmarked by the 10-year sovereign bond; the highest in the G7; and its paper offers a higher yield than any of Portugal, Greece, Ireland, Italy and Spain, the so-called PIIGS whose public finances were such a shambles at the start of the last decade.

UK’s 10-year gilt yield compares unfavourably with developed Western peers

Source: LSEG Refinitiv data

Some degree of political stability may help UK gilts to catch a bid, but advisers and clients must now assess the risks that come with any fixed-income investment:

Source: LSEG Refinitiv data

Inflation and money-printing are the biggest dangers, and any chatter of an expansive Budget under a new Labour leadership team would only fuel the fears of bond vigilantes. As such, advisers and clients could be forgiven of bearing in mind the warning given by J.H. Clapham in his magisterial Economic History of Modern Britain about “blind capital, seeking its 5%.”

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.