Students of history and voters may be aghast that the ruling Labour Party seems determined to engage in the sort of blood-letting that has cast Conservatives, Liberals and Labour alike from office and into the electoral wilderness across the nineteenth, twentieth and twenty-first centuries, but financial markets have tended to approach such episodes with a fair degree of indifference.

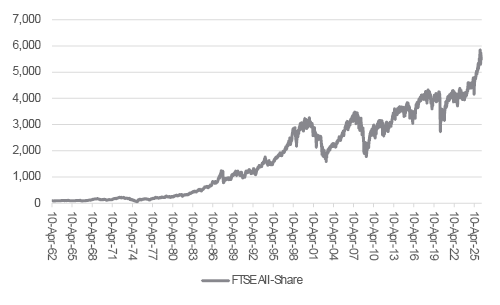

Political squalls have not tended to knock the FTSE All-Share off course for long

Source: LSEG Refinitiv data

Much will now depend on how any potential leadership challenge to Sir Kier Starmer develops and who spearheads it.

June’s Makerfield by-election may be the next development to watch, while advisers and clients can also study any statements from putative candidates, in the knowledge that it is policy shocks rather than policy intentions that have more potential to move bond yields and share prices.

Any student of British history will be tempted to argue that voters shun political parties or Governments which seem to put their own internal disputes and self-interest above those of the nation.

The electorate may give internal politicking the cold shoulder when the ballot box gives them the chance to do so, but financial markets seem to take a more detached view of proceedings, primarily because their focus remains pounds and pence, in the shape of corporate profits, cash flows and dividends, rather than opinion polls.

Since the inception of the FTSE All-Share in 1962, seven Prime Ministers have taken office mid-way during a Parliament, following the departure of their predecessor – James Callaghan and Gordon Brown for Labour, in 1976 and 2007, and John Major, Theresa May, Boris Johnson, Liz Truss and Rishi Sunak for the Conservatives in 1990, 2016, 2019, and 2022 respectively.

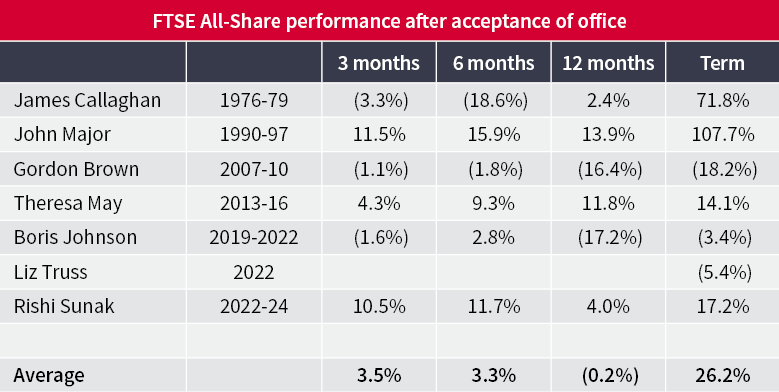

On average, the FTSE All-Share made no immediate progress under the septet during their first 12 months in the hot seat, rising 3.5% over the first three months of the new PM’s tenure, gaining 3.3% over six months and coming in almost flat over a year (although Liz Truss did not manage to last that long).

Wider economic and macro issues have tended to determine equity returns than the identity of the PM …

Source: LSEG Refinitiv data

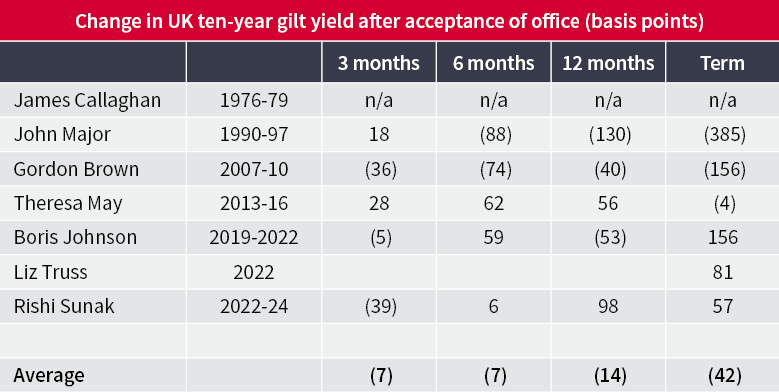

At first glance, the gilt market, as benchmarked by the ten-year issue, tends to be more sanguine still.

Across those terms in office for which there is data available, the average movement in gilt yields is DOWN, not up.

However, the averages are flattered by the sharp declines seen during John Major’s term in office, which encompassed sterling’s ejection from the Exchange Rate Mechanism in autumn 1992. Freed of the obligation to defend the pound, Major, and his appointed Chancellor Norman Lamont, were able to slash interest rates, which in turn helped to drag down the benchmark ten-year gilt yield.

… and the same seems to apply to the gilt market, although the range of outcomes is wide here, too

Source: LSEG Refinitiv data

This suggests that while political stability is welcome, there are many other factors at work when it comes to how the stock market performs, and over their full term in office all seven encountered hugely different economic circumstances, with the result that the FTSE All-Share provided very different returns.

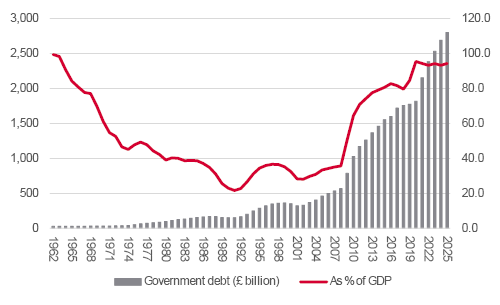

Source: Office for National Statistics

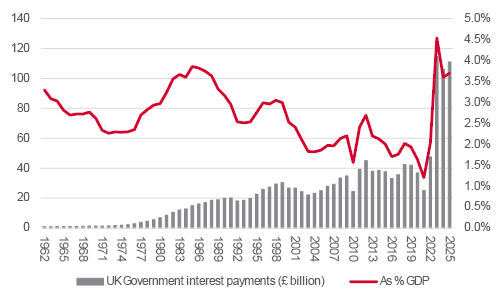

The issue of government indebtedness is one that is yet to be resolved. The UK still spends more than it generates in tax income each year, total borrowing continues to grow, and the interest bill now exceeds £100 billion a year and gobbles up more than the annual defence budget.

Source: Office for National Statistics

The economy is therefore one factor regarding stock market performance – and a successor to Sir Kier Starmer could have an impact here, depending upon their policies for taxation, investment, and regulation – while others are corporate profits and cash flows – and the price (or valuation) investors are prepared to pay to access them.

Politics and policy can, to some degree, affect the earnings, or E in the price-to-earnings valuation calculation, as will external events. But investors’ views of a country’s political stability and acumen will influence the ‘P’ in the P/E, or the price they pay to access those earnings and cash flows.

“From the point of view of the gilt market, advisers can now decide, with their clients, whether the recent increase in yields is a chance to add some fixed-income exposure, once interest rate risk, inflation risk and liquidity risk are all considered.”

If so, our expanded Gilt Managed Portfolio Service (or MPS) range may be worthy of further research. There are seven different maturities on offer, one per year out to 2032, so clients can use the yields to liability match according to their personal needs and time horizons. Any capital gains are free from capital gains tax, so there are some potential advantages over sitting in cash, especially for those clients who are additional or higher rate taxpayers. Upon maturity of a portfolio, cash can then be kept or rolled over into a different product with a different maturity.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.