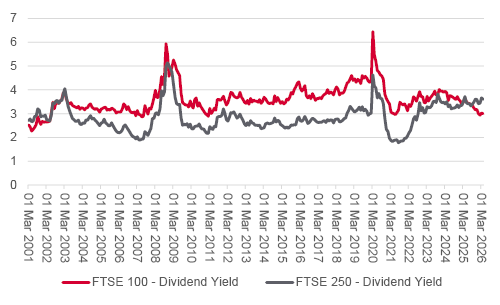

The UK stock market has hit a striking milestone – and income investors should take note. Mid-cap stocks are now paying higher dividends than the blue-chip giants, marking the longest stretch since 2001 where the FTSE 250 offers a bigger yield than the FTSE 100.

On average over the past 25 years, the FTSE 100 has yielded 3.6% and the FTSE 250 has yielded 2.9%. The tables have now turned.

Historically, the FTSE 100 index of large-cap stocks was the place to find the most generous dividends, reflecting the fact it contains more mature companies than mid-caps.

FTSE 100 companies typically generate rich cash flows that help to fund generous dividends, and they are less likely to make large-scale acquisitions. In contrast, mid-caps are often growing their earnings faster and have more pressing needs for surplus cash such as expanding operations or making acquisitions, hence they typically pay lower dividends.

The old rule of thumb was simple: look to the FTSE 100 for solid income and to the FTSE 250 for lower yields but faster dividend growth.

The rulebook changed in October 2025, when the FTSE 250’s yield eclipsed the FTSE 100. We have seen that happen from time to time, but it tends to be a blip. What is interesting this time is how the trend has stayed intact.

Source: LSEG, 22 April 2026

The yield trend is down to the success of the FTSE 100, which has grown at a faster pace than its mid-cap peer. Yields move in opposite directions to prices – so the more the FTSE 100 goes up, the lower its yield – unless analysts upgrade dividend forecasts. The FTSE 250 has still enjoyed a good run; it has just lagged its sister index.

The global market selloff in April 2025, following Donald Trump’s tariff-laden ‘Liberation Day’ saw the FTSE 100 yield spike to 3.9%, before gradually falling to 2.8% in February 2026 as the index recovered and then moved higher. As of 21 April 2026, the FTSE 100 yielded 3% versus 3.6% from the FTSE 250.

The FTSE 100 and FTSE 250 are market cap weighted indices, which means the biggest companies by market valuation have the greatest influence on the direction of the index and its headline yield. For example, four of the top 10 names by market value in the FTSE 250 currently offer a prospective yield above 6%.

Anyone considering the FTSE 250 as a potential source of income should study the component parts of the index. Half of the index (46%) contains financial companies, specifically investment trusts, asset managers, and a couple of banks – and these can be useful sources of income. Industrials account for approximately 15% of the index, and it is common to see 2– 3% dividend yields from this part of the market.

The other big FTSE 250 sector is consumer discretionary, which spans a variety of industries. Dividends are more variable in this broad space, with certain names like housebuilder Taylor Wimpey and broadcaster ITV yielding between 6% and 8%, building materials group Marshalls and rail-to-bus operator FirstGroup in the 4–5% range, and retailers Currys and Moonpig yielding 2% or less.

Source: LSEG, 17 March 2026

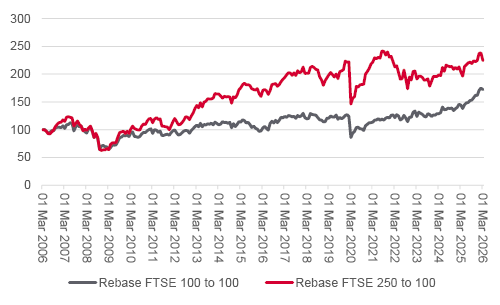

While the FTSE 250 has lagged the FTSE 100 in recent years, it has better long-term returns. Over the past 30 years, it has generated an 8.7% compound average annual return versus 7.2% from the FTSE 100. These figures factor in reinvested dividends.

Furthermore, while the headline yield is currently higher for the FTSE 250 versus the FTSE 100, income investors should note capital growth has historically been a bigger component of the mid cap index’s overall returns than dividends. Excluding dividends, the FTSE 250 has generated a 5.7% average annual return over 30 years compared to 3.5% from the FTSE 100.

There are three core ways to get broad exposure to the FTSE 250 index. First is a range of tracker funds or exchange-traded funds designed to mirror the performance of the FTSE 250.

The UK mid cap ETF with the lowest fees is HSBC FTSE 250 ETF which has an in-built charge of 0.09% a year. Cheaper at 0.05% is Amundi Prime UK Mid and Small Cap ETF, which has a blend of medium and smaller companies.

Secondly, there are various mid-cap-focused investment trusts, including Mercantile and Schroder UK Mid Cap Fund. Lastly, mid-cap-related open-ended funds include FTF ClearBridge UK Mid Cap Fund and Jupiter UK Mid Cap Fund.

The FTSE 250 is more exposed to the UK economy than the FTSE 100. With GDP trends still underwhelming, confidence in the government’s growth plan remains a waiting game. But that does not mean FTSE 250 earnings are stuck in the mud – far from it. Certain companies in the index continue to make steady progress, creating the right environment for the dependable, rising income streams investors want.

One note of caution: anyone buying an actively managed UK mid-cap fund without an income mandate should understand that the managers may not prioritise dividend sustainability – they focus on earnings growth, with income just a ‘nice-to-have'.

A dedicated equity income fund would look closely at a company’s ability to keep paying dividends, yet UK funds in this space are likely to focus on larger companies than mid-cap ones. One exception is Man Income, which has a blend of mid and large cap names.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.