Certain people might have been surprised at how lower-risk investments have not provided complete protection as the Iran conflict unfolded. But they are not meant to, and it is an important reminder that diversification is vital when investing.

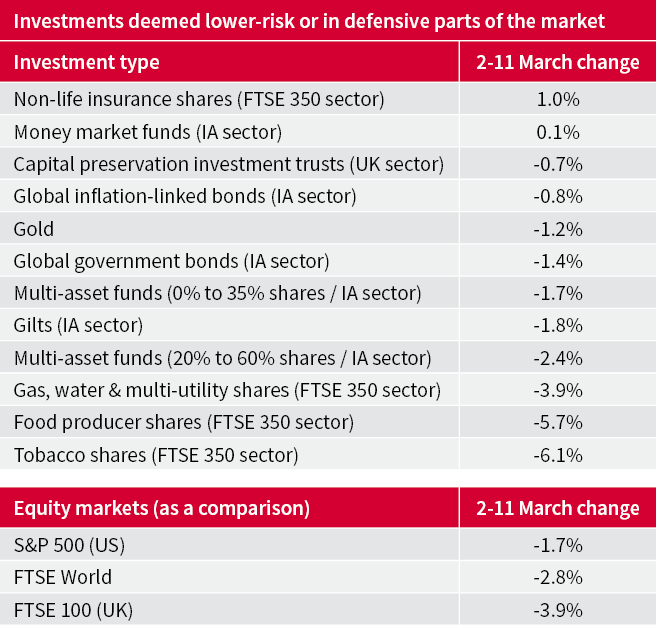

Research by AJ Bell, looking at investments one might expect to offer ballast in challenging times, found that only money market funds and shares in non-life insurance companies have truly preserved investors’ capital since the Middle East crisis unfolded. Defensive-style sectors like food and tobacco have not lived up to their reputation.

While this might sound gloomy, the key takeaway is that so-called lower-risk investments in general have been useful during the latest market wobble. They have provided stability – which is often an underappreciated factor. Investing should be viewed as a long-term pursuit and remains an attractive way to make money along the way, and the current environment has shown the importance of having a blend of assets to ride out the ups and downs.

It is also important to remember that despite the recent slump, markets are up considerably from where they were this time last year. For example, the FTSE 100 is up 24% in the 15 months since January last year, while the S&P 500 is up by 13.8%, based on total return data from ShareScope.

Certain areas like capital preservation investment trusts have done a fair job, falling by less than the broader market, and global inflation-linked bonds have done heavy lifting in a challenging time for portfolios.

Bonds should cushion a portfolio when equity markets retreat, and to some extent they have ticked the right boxes so far in March. However, on a broad basis they have still lost value, albeit only minor compared to stocks and shares. That is what you should expect to happen, rather than bonds not falling at all.

Even though markets staged a minor recovery earlier this week when Donald Trump gave the impression the Iran conflict could soon be over, there is no guarantee this will be the case.

Certain areas with defensive qualities such as tobacco, healthcare and food left investors with a sour taste and a dent in their portfolio. Even gold and gilts pulled back in value, and left portfolios with scrapes along the side.

The speed at which the Middle East crisis unfolded caused shockwaves across both energy and financial markets. Certain investors balked at how fast oil and gas prices went up, causing indiscriminate selling from portfolios and dragging down asset prices left, right and centre.

Consumer staples – a broad term that includes food, drink and household products – are often seen as defensive parts of the market because their products are consumed no matter what’s going on in the world. One might have expected them to do well during the crisis. However, shares in this part of the market fell on fears of new inflationary pressures, including a 17.3% slump from health and hygiene products giant Reckitt, an 11.4% decline in deodorant‑to‑cleaning products provider Unilever, and a 7% drop in cigarettes‑to‑vaping group Imperial Brands since the start of last week.

Consumer staples companies theoretically have pricing power, namely the ability to push up prices without depressing demand. In a gradual inflationary environment, this might be possible, but the past fortnight has not been a normal one.

The sheer pace of oil price hikes presents a major risk that consumers could face a sharp increase in the cost of living. This could potentially lead to a drop in consumption or more selective purchases until consumers get a better grasp on whether higher prices are a short‑term issue or a permanent change.

Gold is a haven in troubled times, but what many people do not realise is that its price can still drop in a falling market. Investors often sell what they can in the face of trouble, and gold is a liquid asset.

In 3 of the 10 worst quarterly global equity market declines of the past 25 years, gold fell in price before rebounding. At times, gold has been able to cushion portfolios when equities dip, but this is far from a certainty. Other assets, such as short duration bonds, have functioned as a more stable diversifier.

Money market funds aim to provide a return slightly above cash. They contain a portfolio of higher‑quality, low‑risk investments such as bonds issued by governments or companies that mature within twelve months, some as short as two to three months. This makes them far less sensitive to changes in interest rate expectations than longer‑dated bonds. They also invest in certificates of deposits – a type of savings account that pays a fixed rate on money over a set period.

Money market funds were popular with investors during 2025 but started to lose traction as more people showed an interest in UK and global funds, according to analysis of AJ Bell DIY investor behaviour in January. Investors who maintained exposure to this fund type might be thankful for their decision to have a cautious element in their portfolio.

Last week saw a sell‑off in gilts as the market reassessed expectations for interest rates considering higher energy prices. Prior to the Middle East crisis, markets had expected the Bank of England to cut rates by at least half a percentage point during the whole of 2026 – now there is talk of rates staying higher for longer. Probability data from LSEG implies traders believe rates could remain at 3.75% for the next 12 months at least.

The two‑year gilt yield jumped from 3.53% to 3.76% last week and now trades around 4%. In bond market terms, that is a big movement in a short space of time. The rise in gilt yields makes existing bonds with lower coupons less attractive, as investors sell gilts if they believe newer bonds will be issued at a higher yield.

Conversely, the large drop in gilt prices since the start of last week might attract investors who believe the Middle East conflict could be short‑lived and that interest rate expectations could shift once again towards looser monetary policy.

In this situation, an investor might buy short‑dated gilts in the hope of making a capital gain, as UK government bonds are exempt from capital gains tax on any profit made from selling or redeeming them at maturity. That is particularly attractive to investors who might have used up their ISA allowance and want further ways to make money and minimise tax.

No‑one knows if the worst is over for the sell‑off in financial assets following the US and Israel’s strikes on Iran. There are mixed messages coming from the White House, with Trump recently implying everything will soon be fine versus US defence secretary Pete Hegseth suggesting the assault was ‘only just the beginning’.

Advisers are likely to be fielding questions from clients. Offer them reassurance and remind them market wobbles are common. No‑one knows how long the Middle East crisis could last, but a well‑diversified portfolio and patience create the best recipe to ride out volatility.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.