This column is being written just before the next meeting of the Federal Open Market Committee on Wednesday 20th and the working premise is that chair Jay Powell and his colleagues at the US Federal Reserve will leave the headline interest rate unchanged at 5.50%. If that does not turn out to the case then readers can immediately turn over the page, not least to spare the writer’s blushes.

That caveat aside, three datasets released last week are moving markets in what may be very important ways. This is because they challenge the consensus narrative that the US inflation is cooling, the US economy will encounter a soft landing (at worst) and the Fed will be able to pivot to cutting interest rates, with the result that cheaper money (and a less testing benchmark in the form of returns on cash and bond yields) will propel US share prices onwards and upwards.

“This test of the consensus comes at an interesting time, since the Dow Jones, S&P 500 and NASDAQ all trade at all-time highs.”

This test of the consensus comes at an interesting time, since the Dow Jones, S&P 500 and NASDAQ all trade at all-time highs. Also bear in mind that consensus view in 2022 was that a recession was coming – and that proved to be wrong. The consensus view in 2023 was that inflation would cool and rate cuts would come quickly – and that proved to be wrong, as markets are still waiting for the first move from the Fed (and the Bank of England and the European Central Bank, for that matter).

The markets’ misjudgement of 2022 laid the groundwork for a big rally in global equities in 2023 and their inaccurate analysis of 2023 did no damage either, as the Germany’s DAX, France’s CAC-40, Japan’s Nikkei-225 and Australia’s ASX-200 all barrelled to new peaks, just like America’s headline indices. But at the very least advisers and clients might like to consider the possible implications of a rather unfortunate hat-trick of poor forecasts in 2024.

The three datasets that probed the cosy consensus of cooler inflation, a shallow slowdown and lower rates were as follows:

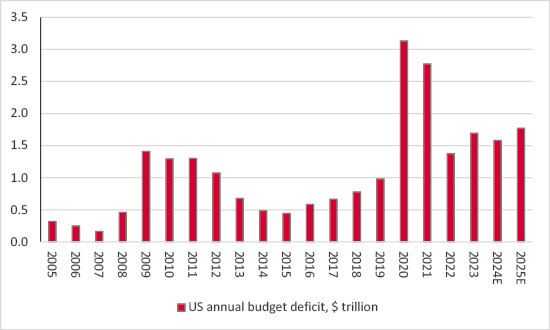

Biden administration plans further deficit accumulation in 2025

Source: LSEG Datastream data, FRED - US Federal Reserve database, Congressional Budget Office

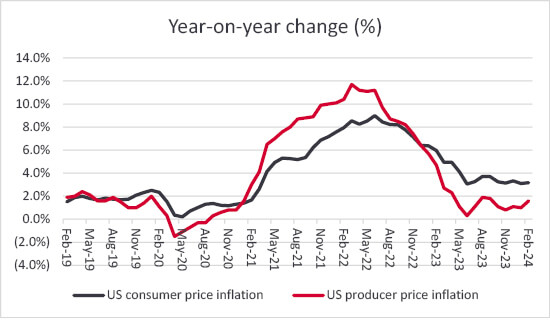

“The US inflation rate, as measured by the consumer price index, reaccelerated to 3.2% year-on-year in February, to mean that the rate of increase is higher now than it was in June 2022.”

US inflation may be reaccelerating

Source: US Bureau of Economic Analysis, FRED – St. Louis Federal Reserve database, LSEG Datastream data

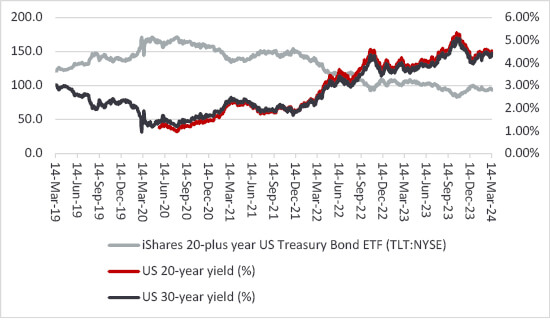

“Bond markets are paying attention. The iShares 20-year Plus Treasury Bond Exchange-Traded Fund, which has the ticker TLT:NYSE, is down by nearly 8% from its December high, as long-dated US Treasury yields go higher once more, in a rout that is wiping out two years’-worth of coupons at a stroke.”

Bond markets are paying attention. The iShares 20-year Plus Treasury Bond Exchange-Traded Fund, which has the ticker TLT:NYSE, is down by nearly 8% from its December high, as long-dated US Treasury yields go higher once more, in a rout that is wiping out two years’-worth of coupons at a stroke.

US long-dated bond yields are responding …

Source: LSEG Datastream data

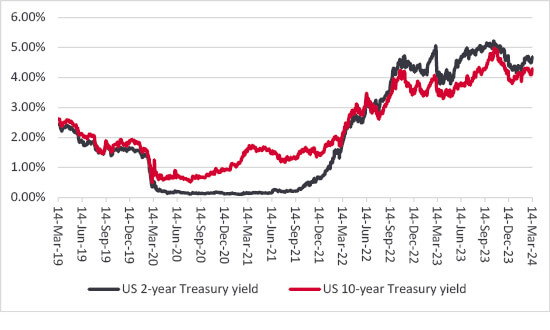

The yields on two-year and ten-year US Treasury bonds are creeping higher again (and their prices sliding lower). This is in response to both the sticky inflation numbers but also, presumably, the prospect of increased bond issuance by the US government should President Biden win the election in November and get to implement his planned budget (and even if he does not prevail, the alternative, Donald Trump, is hardly known for being spendthrift).

… and so are two- and ten-year Treasuries

Source: LSEG Datastream data

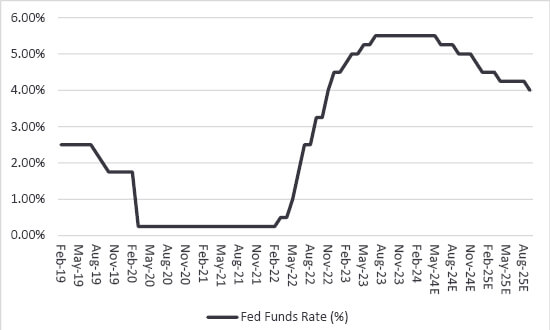

“At the start of 2024, the CME Fedwatch data service suggested markets were looking for six, one-quarter point rate cuts from the US Federal Reserve this year, with the first coming in March. Now consensus is for three cuts, starting in June, with the sixth cut of the lowering cycle only coming in September 2025.”

Higher bond yields reflect a recalibration of expectations for interest rate cuts, for the second year in a row. At the start of 2024, the CME Fedwatch data service suggested markets were looking for six, one-quarter point rate cuts from the US Federal Reserve this year, with the first coming in March. Now consensus is for three cuts, starting in June, with the sixth cut of the lowering cycle only coming in September 2025.

Markets are cutting back on their hopes for Fed rate cuts

Source: CME Fedwatch, US Federal Reserve, LSEG Datastream

This is not guaranteed to derail the equity bull market, not least because economists were off beam in 2022 and 2023 and it mattered not a jot. But just as weight stops trains, higher rates tend to slow stocks down in the end, especially long-duration sectors such as technology and biotechnology, which is exactly where equity markets’ optimism feels most prevalent at the moment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.