The combination of Liberation Day’s tariffs, wars in the Middle East and Eastern Europe, worries over the long-term impact of artificial intelligence upon jobs, galloping government debts and stretched budgets, and active debate about stock market bubbles does not look like a favourable one for advisers and clients, but many will look back upon 2025 with contentment. Equities, bonds and commodities all provided positive returns, at least in local currency terms.

However, there are some discordant notes, notably the ongoing surges in gold and silver, which may yet be harbingers of heightened volatility in the year ahead. From this perspective, the calm in the equity and fixed-income markets may look odd, especially as Western governments continue to overspend and pile up fresh borrowing, the interest payments for which could crimp growth and crowd out more productive investment elsewhere.

However, there may be method in markets’ thinking, and the core thesis seems to be the so-called ‘debasement trade’.

A backbench rebellion over the two-child welfare cap by Government MPs in the UK, the ‘Bloquons Tout’ public protests over changes to pensions in France and the debate over Obamacare subsidies that led to the government shutdown in America all had the same starting point as their origin: sovereign debt.

All three nations have longstanding records of spending more than they generate in tax, with the result that borrowing is up in absolute terms, but also as a percentage of GDP. That may not be such an issue when interest rates are zero, as for much of the 2010s and early 2020s, but even small increases in headline borrowing costs, and thus sovereign bond yields, mean the interest bill can surge quickly.

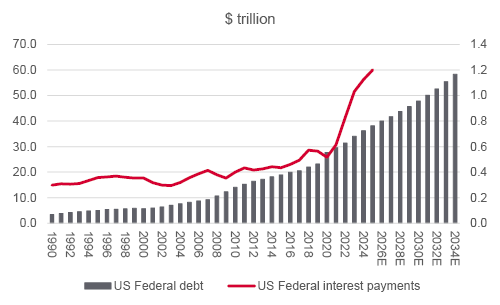

According to Congressional Budget Office estimates, the second Trump administration will add $7.4 trillion to the federal debt across its four-year term. It took America until 2003 to amass a total Federal debt of $7 trillion. Add in Federal Reserve interest rate hikes, and the need to issue new Treasury bonds as old ones mature, and America’s interest bill now exceeds $1.1 trillion, or a fifth of the tax take.

US federal debt pile, and the interest bill, continue to grow

Source: St. Louis Federal Reserve database

President Trump and Treasury Secretary Bessent are alert to the danger.

They are trying to boost growth, raise tax income from tariffs and hector the US Federal Reserve into lowering interest rates, all in the cause of making the interest bill more manageable and reducing the debt-to-GDP ratio.

And it is the prospect of rate cuts that is supporting the US Treasury market, where the benchmark ten-year yield is grinding lower, with the result that US sovereign bond market prices are grinding higher – even though supply continues to rise.

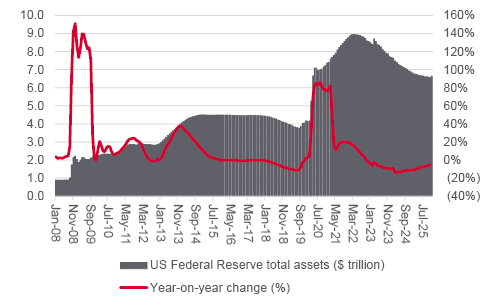

Given that interest rates seem much more likely to trend down than up, not least because the government cannot really afford higher borrowing costs, the risk-reward profile for Treasuries seems skewed toward return, all things being equal, especially now the US Federal Reserve’s balance sheet is no longer shrinking as Quantitative Tightening comes to an end.

There is surely zero chance of Fed asset holdings going back to their pre-Financial Crisis levels. Moreover, chatter already abounds that the Fed could return to Quantitative Easing (QE) and bond-buying in the event of any unexpected economic or financial market turbulence.

US Federal Reserve has halted Quantitative Tightening

Source: FRED – St. Louis Federal Reserve database

Such price-insensitive bond purchases could bring near-term gains, but there are still two long-term dangers here.

Both represent the risk of currency, or asset, debasement owing to inflation and galloping supply (of money, bonds, or both).

It does therefore make sense that all three asset classes – fixed-income, equities, and precious metals – can go up at once. But it seems unlikely to last forever, given the fragile nature of government finances, and the Scylla and Charybdis of inflation and recession which lie in wait on either side of the scenario currently priced in by financial markets, namely steady growth, cooler inflation and gently lower interest rates.

Markets expect lower inflation, falling rates and steady growth in 2026 – but any one of these assumptions could be challenged. Advisers may want to focus on three quick checks:

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.