President Donald J. Trump is already one year into his second term in the White House and advisers and clients may therefore like to bear in mind that one statistical quirk of America’s S&P 500 is how the US benchmark equity index tends to do least well during the second year of a presidency. Trump’s first term lived down to historical type, as the Dow Jones Industrials fell by nearly 6% in 2018. Given lofty earnings expectations, and equally lofty valuations, advisers and clients may therefore wish to assess their US equity exposure, even if they are safe in the knowledge that the past is no guarantee for the future.

Source: LSEG Refinitiv data

The mid-term elections, set for 3 November, are already looming, and the chances are they will become the usual protest vote that sees the incumbent party lose seats in the House of Representatives, the Senate or both. Given the narrow Republican majorities in each, Trump could lose control of at least one, and thus find his room for policy manoeuvre greatly constrained in the last two years of his term.

Savvy operator that is he, Trump is aware of this danger. Hence his ongoing campaign to get the US economy to run hot, with help from a lower dollar, a lower oil price, lower interest rates, tax cuts and deregulation. If this plan succeeds, and the combination of monetary and fiscal stimulus leads to upside surprises from US corporate earnings, then the S&P 500 could yet confound the historical pattern of a relatively quiet second year to a presidency.

Sharp-eyed advisers and clients will also notice that the Dow Jones Industrials has a better record in the second year of a presidency under Republican leaders than it does under Democrat ones.

One theory here is that the Republicans come in and use their first year to introduce hair-shirt policies in response to what they see as Democratic fiscal laxity, and then ease off as their reforms bear fruit and mid-term and then end-of-term polls beckon.

Neither of Trump’s terms has followed this script, given his governments’ propensity to spend and borrow. His supporters will argue that income from tariffs and growth in investment and jobs from onshoring will help the numbers to add up, but the import levies will have to be impressive indeed if they are to fund new tax cuts, let alone those coming through this year as part of 2025’s One Big Beautiful Bill, and cover $500 billion in additional annual defence spending.

The combination of fiscal stimulus from tax cuts and monetary stimulus from lower interest rates, for which the President continues to call loudly, is a potentially beguiling one, especially once the potential productivity gains from Artificial Intelligence (AI) are added to the mix.

Analysts already think that AI is adding more than one percentage point to US GDP growth, thanks to the boom in data centres and the boost this provides to not just silicon chip and server providers, but also construction firms, the engineers who provide the water cooling systems and heavy equipment, and even utilities as they add to the capacity of the electrical grid.

The flipside, however, is that AI fails to deliver the expected productivity gains, or at least quickly enough to justify further massive investment by the so-called hyperscalers. Consensus forecasts suggest that the aggregate capital investment bill at Amazon, Alphabet, Meta Platforms, Microsoft and Oracle will jump by another 40% in 2026, to $600 billion, even after surges of 72% in 2025 and 60% in 2024.

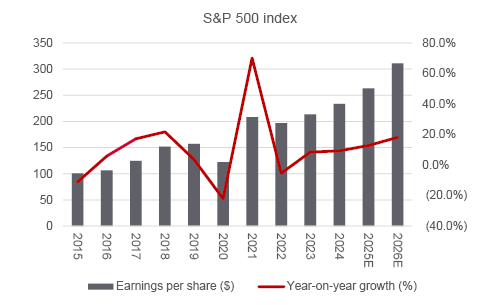

If delays or cuts chip away at the 2026 budgets there could be trouble ahead, especially as the US equity market trades on 22 times forward earnings for this year, which compares to a ten-year average of 19 times according to FactSet.

Even that assumes 18% earnings growth in 2026, more than twice the long-term run rate, after a healthy 13% advance in 2025, according to research from Standard & Poor’s.

Source: LSEG Refinitiv data

Any earnings disappointment could therefore hit home hard, although the White House will doubtless do all it can to keep the stock market show on the road ahead of the mid-terms, even if that means leaning on the US Federal Reserve and a few neighbouring countries for good measure.

Any such pressure could yet take its toll on the dollar, and weakness in the buck did erode returns from US assets last year, which is another consideration for advisers and clients with hefty exposure to American equities. In sterling terms, the UK beat the US hands down in 2025, helped by lower starting points in terms of valuation, sentiment and earnings expectations.

Source: LSEG Refinitiv data

The US could therefore do well and still underperform other arenas which look cheaper. Advisers and clients who take a truly long-term view will be aware of how US equities stand close to a record high as a percentage of global stock market capitalisation. In this context, markets may already be pricing in to the full the concept of American exceptionalism, at least barring an epic, crack-up economic boom.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.