The FTSE 100 continues to largely paddle sideways and is barely any higher now than it was in spring 2017, some six-and-a-half years ago. Such a turgid capital return has at least been supplemented by dividends and also share buybacks, which have played an ever-greater part of shareholder returns in the past few years, both in the UK and the USA.

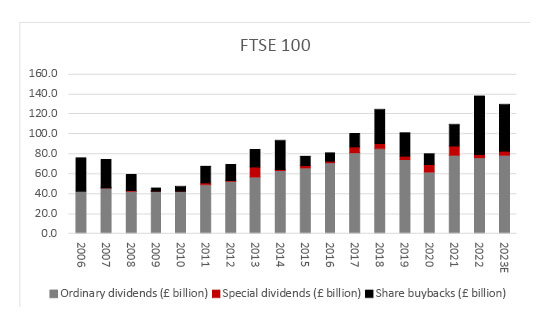

“Members of the UK’s elite index, the FTSE 100, have announced share buyback schemes worth £46.9 billion so far in 2023. That is the second-highest sum on record and trails only the £58.2 billion returned via this mechanism in 2022.”

Members of the UK’s elite index, the FTSE 100, have announced share buyback schemes worth £46.9 billion so far in 2023. That is the second-highest sum on record and trails only the £58.2 billion returned via this mechanism in 2022.

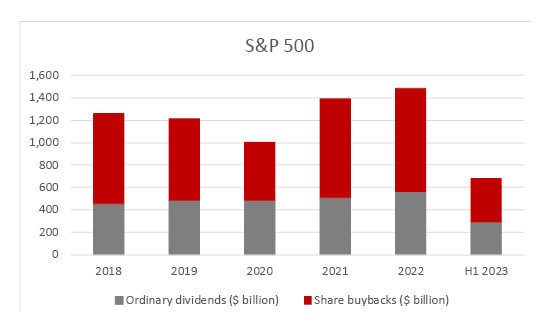

Buybacks reached a record in the USA last year as well but the pace of cash returns via share repurchase schemes has just started to slacken on the other side of the Atlantic. Research from Standard & Poor’s reveals that the total value of buybacks by members of the S&P 500 index fell 20% year-on-year in the second quarter.

“Those advisers, clients and fund managers who view buybacks as a good thing must now decide whether a slower run rate is a potential warning sign of tougher times ahead, at least for the buoyant US equity market. Equally, they may view any pick-up in volumes as a good thing.”

Those advisers, clients and fund managers who view buybacks as a good thing must now decide whether a slower run rate is a potential warning sign of tougher times ahead, at least for the buoyant US equity market. Equally, they may view any pick-up in volumes as a good thing.

Those who view them as financial engineering, and thus with greater scepticism, could be forgiven for thinking that the 2021-23 buyback splurge is a contrarian indicator, since share repurchase schemes proliferated near the equity market tops of 2006 and 2018 and all but disappeared when stocks were at their cheapest in 2009 and 2020.

America’s Securities Exchange Act of 1934 outlawed share buybacks as it deemed large-scale share buybacks could be a form of wilful share price manipulation. That was only repealed in 1982 by the Reagan administration, with rule 10b-18, and since then buybacks have become increasingly popular.

“There are four arguments put forward in favour of share buybacks.”

There are four arguments put forward in favour of share buybacks.

All of these have been put forward to justify the boom in buybacks in both the UK and USA.

UK buybacks on course for at least second-biggest total on record in 2023

Source: Company accounts

US buyback rate has cooled a little in the first half of 2023

Source: Standard & Poor’s research

“Equally, there are four reasons to treat share buybacks with some degree of caution.”

Equally, there are four reasons to treat share buybacks with some degree of caution.

Advisers and clients will have neither the time nor the inclination to look at stock-specific instances of buybacks – that sort of research is one reason why they may choose to pay active fund managers. Equally, any adviser or client that uses a passive index tracker will need to keep abreast of share buybacks and the implication for fund flows and liquidity if nothing else.

Buybacks can provide support to share prices, and thus indices, thanks to the steady stream of purchases they provide. Advisers and clients must therefore ask themselves what might happen if that crutch is kicked away, although they can perhaps take comfort (to varying degrees) from the identities of the biggest share repurchasers on both sides of the Atlantic.

Buybacks can provide support to share prices, and thus indices, thanks to the steady stream of purchases they provide. Advisers and clients must therefore ask themselves what might happen if that crutch is kicked away, although they can perhaps take comfort (to varying degrees) from the identities of the biggest share repurchasers on both sides of the Atlantic. Again, they may not have time for stock specifics, but they will need to be aware of the major stock sensitivities, should they go down the passive or active route when it comes to country asset allocations and fund selection.

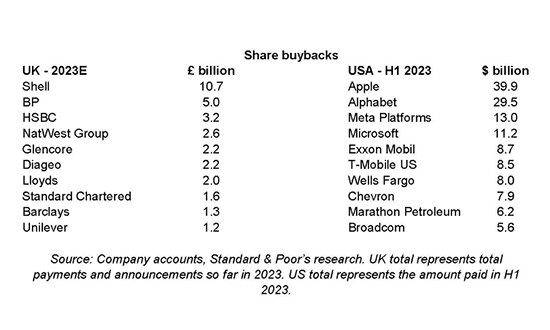

Ten biggest stocks for share buybacks in 2023

Source: Company accounts, Standard & Poor’s research. UK total represents total payments and announcements so far in 2023. US total represents the amount paid in H1 2023.

Sceptics will be on the look-out for any signs of a deceleration in buybacks, especially in the USA. Accusations of financial engineering may mount if there are any more accidents like those that have befallen General Electric or Intel, where share buybacks limited investment in the products and core competitive positions of those firms, with deleterious effects.

Some argued big buybacks meant those firms focused too much on financial engineering and not enough on product engineering, in an uncanny echo of the terse accusation outlined by J.M. Keynes in his 1936 book, General Theory of Employment, Interest and Money: “When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.”

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.