This column is no adherent to ‘efficient market hypothesis’, not least because there would not be equity booms and busts, or even marked day-to-day volatility, if investors really knew what was coming around the corner – it simply would not be possible to make a profit if everything was perfectly priced. However, it does have a lot of sympathy with the argument that a security’s price is a very fair reflection of what is known, and thought, about what is happening to it now, especially given the number of very smart professional (hedge, pension and institutional) funds and retail investors who will be looking at it, day in, day out.

In sum, the market may not always be right, but its views must be respected and so it is always worth paying attention to what the market is saying – either because the adviser and client (or appointed active fund manager) feel it is wrong, and there is a contrarian opportunity to be had, or because a subtle shift in sentiment that runs against the prevailing wisdom is underway.

In this context, a return to favour among more defensive equity sectors very much catches the eye, at a time when advisers and clients are grappling with whether central banks are getting it right with the timing of their interest rate changes and whether the US may be about to slow down just when the world is relying more heavily than ever on its key economic engine for growth.

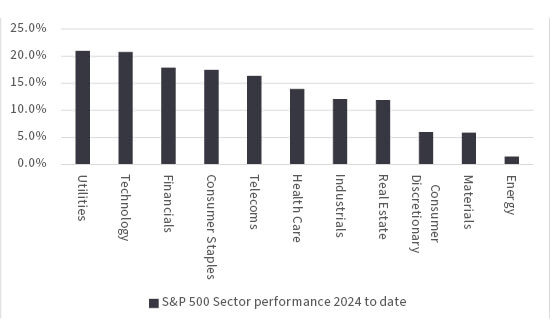

Given all of the headlines still grabbed by, and the $14.5 trillion aggregate stock market valuation attributed to, the so-called ‘Magnificent Seven’ of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla, it would be logical to assume that tech stocks are still doing rather well, even after the summer stumble. Nor it is far from the truth, as Technology is the second-best performer in 2024 to date among the eleven super-sectors which comprise the S&P 500 index.

However, the best performer is Utilities.

Utilities is now the best-performing sector in the US in 2024

Source: LSEG Refinitiv data, as of 10 September 2024, based on S&P 500 sectors

This could be down to the possible boost to demand for electricity from data centres that run the Large Language Models behind Artificial Intelligence and store vast swathes of digitised information and content. It could be because utilities are seen as so-called ‘bond proxies’, and a sector that usually does well when interest rates (and bond yields) are falling, as this makes the yield on utility stocks seem more attractive on a relative basis. And it could be because investors are subtly looking for a haven, and industries where demand is relatively predictable and not too sensitive to the wider economy, just in case an unexpected slowdown is coming around the corner in the USA.

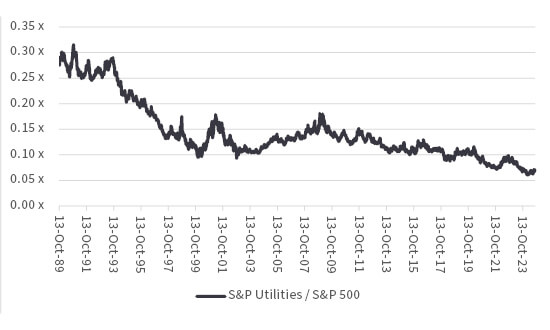

Utilities have offered the best relative performance during recessions

Source: LSEG Refinitiv data, based on S&P 500 sectors

“The long-term chart for Utilities’ performance relative to the S&P 500 remains ugly, but it is worth noting how the sector’s defensive, economically insensitive characteristics enabled it to outperform during 1990-92, 2000-02 and 2007-08, just as the US entered a recession or encountered some form of financial market meltdown, or both.”

The long-term chart for Utilities’ performance relative to the S&P 500 remains ugly, but it is worth noting how the sector’s defensive, economically insensitive characteristics enabled it to outperform during 1990-92, 2000-02 and 2007-08, just as the US entered a recession or encountered some form of financial market meltdown, or both.

The presence of Financials among the leaders offers some reassurance, as does how every US sector is still in positive territory this year, but the presence of Consumer Staples and Telecoms in the top five is not necessarily what you would expect to see if investors were truly confident in America’s economic outlook.

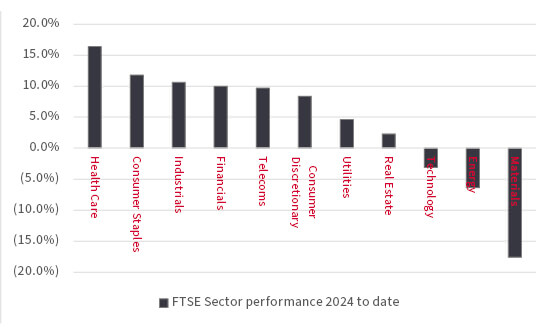

“Relatively defensive sectors are to the fore within the FTSE UK indices, in the shape of Health Care, Consumer Staples and Telecoms. Materials and Energy are the laggards, just as they are in the USA, and commodity price weakness could speak of nerves regarding the global economic outlook.”

According to the official data from the Office for National Statistics, the UK is emerging from the shallow recession suffered in the second half of 2023, but it is making heavy weather of doing so, if the UK equity market is to be believed. Relatively defensive sectors are to the fore within the FTSE UK indices, in the shape of Health Care, Consumer Staples and Telecoms. Materials and Energy are the laggards, just as they are in the USA, and commodity price weakness could speak of nerves regarding the global economic outlook.

Defensive sectors are also at the fore in the UK

Source: LSEG Refinitiv data, as of 10 September 2024, based on the FTSE UK sectors

Utilities have fared less well on this side of the Atlantic, and that could be down to uncertainty over the new AMP8 regulatory cycle for water companies that begins in April 2025, especially as water and wastewater treatment providers are still the subject of much public opprobrium over the quality of their services, the prices they charge and the bonuses they pay. Utilities were also the subject of windfall taxes when Tony Blair’s Labour Government took over in 1997 and those market participants with UK equity exposure may have taken some evasive action with this year’s General Election in mind.

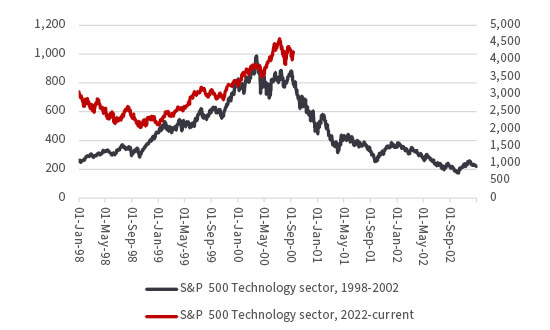

“These trends could yet prove ephemeral, and sentiment could switch again – technology for one is unlikely to go down without a fight, if indeed it is to go down at all any time soon.”

These trends could yet prove ephemeral, and sentiment could switch again – technology for one is unlikely to go down without a fight, if indeed it is to go down at all any time soon. If indeed summer’s ructions are the first signs of a top in the sector which, for the moment at least, peaked on 10 July there may be many attempted rallies before the bull market cracks, just as there were in 2000 when the tech bubble burst. The telling indicator back then was each rally failed to reach the prior peaks and that may be a trend to note this time around, too.

Technology investors will be looking for new highs for reassurance

Source: LSEG Refinitiv data

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.