Working out exactly what (outgoing?) US President Trump wanted was not always easy but one of the topics upon which he seemed most consistent was the dollar. He spent much of his four-year tenure in the White House complaining about how the greenback was too high and ultimately he got his way, even if he may have finally come around to the view in 2020 that a rising currency was a backhanded compliment from markets about the relative strength of the US economy.

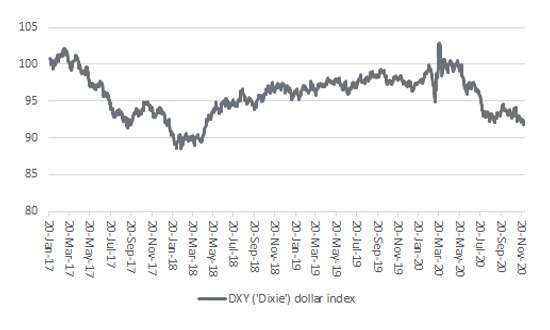

Since his inauguration on 20 January 2017, the dollar is down by 9%, using the trade-weighted basket of currencies that makes up the DXY (or ‘Dixie’) index as a guide, and now trades at a two-and-a-half-year low.

The US dollar weakened during the Trump Presidency

Source: Refinitiv data

“A loss of value in the globe’s reserve currency, and a major haven asset, has potential implications for a range of markets, and not just foreign exchange.”

A loss of value in the globe’s reserve currency, and a major haven asset, has potential implications for a range of markets, and not just foreign exchange.

There are multiple possible reasons for the buck’s case of the blues.

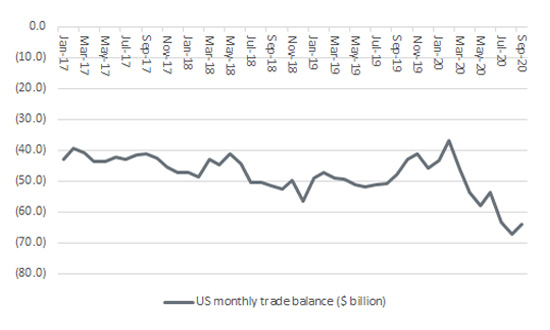

“The US trade deficit has surged back toward its all-time highs, with the result that dollars are flowing out of America to pay for the overseas-produced goods that consumers are sucking into the country.”

Second, the President’s trade war with China unsettled markets and seemed to bring no great economic benefit. The US trade deficit has surged back toward its all-time highs, with the result that dollars are flowing out of America to pay for the overseas-produced goods that consumers are sucking into the country.

In some ways, this can be seen as a good sign. Way back in 1960, Professor Robert Triffin argued that America would always have to run a trade deficit, and pay out more dollars than it received, to ensure the world had enough of the reserve currency to go around. The alternative would be a painful liquidity squeeze on the globe’s economy and financial markets alike as dollars flooded home.

Trump administration has failed to reduce the US trade deficit

Source: FRED – St. Louis Federal Reserve database

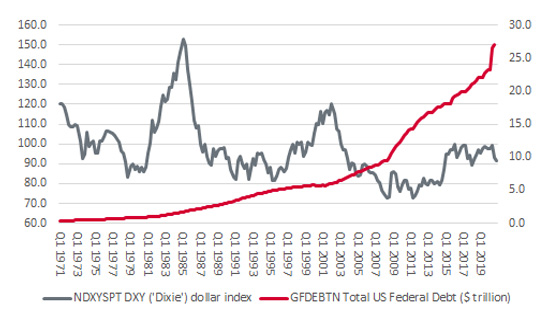

The more debt the US has taken on, the weaker its currency has become

Source: FRED – St. Louis Federal Reserve, Refinitiv data

“It took America 237 years to get to 2013’s suspension of the debt ceiling at $16.7 trillion. That persuaded Moody’s to downgrade the US credit rating but Uncle Sam has taken just seven years to overspend by a further $9.3 trillion.”

This argument is not unique to America – something which may be sparing the dollar a few more blushes – but it will surely continue a trend of ever-higher Government debt ceilings. That really dates back to the early 1970s, when Richard M. Nixon took America off the gold standard so he could pay for welfare programmes and the Vietnam War, but the trend is clearly accelerating. Remember that Moody’s downgrade of America’s credit rating, and a summer of turmoil in financial markets, came after 2013’s debt ceiling suspension, when the limit was $16.7 trillion. It had taken America 237 years to get there but Uncle Sam has taken just seven years to overspend by a further $9.3 trillion.

Anyone who takes the view that American debt is not a sustainable path will be wary of the dollar. Anyone who feels that COVID-19 can be contained and the world can build a reliable recovery will also fight shy of the buck, especially if they buy into Triffin’s theories, which imply that a weak dollar is the natural result of a strong US economy and robust global trade flows – both of which would logically benefit emerging markets and commodities, asset classes that traditionally do well when the dollar is weak.

“Any attempt to reset currencies – and debts – could yet be spearheaded by central bank-backed digital currencies (CBDCs), a trend which must be closely watched.”

The dollar is likely to hang tough for a while yet, not least as suitable candidates to replace it as the world’s reserve currency are in short supply: China's renminbi is not fully convertible, a return to gold will impose disciplines which no politician or central banker will accept (or can afford) and cryptocurrencies do not have universal acceptance. But any attempt to reset currencies – and debts – could yet be spearheaded by central bank-backed digital currencies (CBDCs), a trend which must be closely watched.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.