The Conservative Party’s Benjamin Disraeli, twice Prime Minister and thrice Chancellor of the Exchequer, once said of his bitterest political rival, who held each post on four occasions, “Well, if Mr Gladstone fell into the Thames that would be a misfortune; and if anybody pulled him out, that would be a calamity.”

The Tories’ latest Chancellor, Rishi Sunak, will be hoping for a warmer welcome for Wednesday’s Budget (3 March) and he is likely to measure success in terms of jobs, economic growth and ultimately opinion polls and votes.

“Advisers and clients will be looking to their portfolios to gauge the effect of the Budget and history suggests that the UK stock market has, for whatever reason, done better on average under Conservative Chancellors than Labour ones, at least once inflation is taken into account.”

Advisers and clients will be looking to their portfolios to gauge the effect of his policies and history suggests that the UK stock market has, for whatever reason, done better on average under Conservative Chancellors than Labour ones, at least once inflation is taken into account.

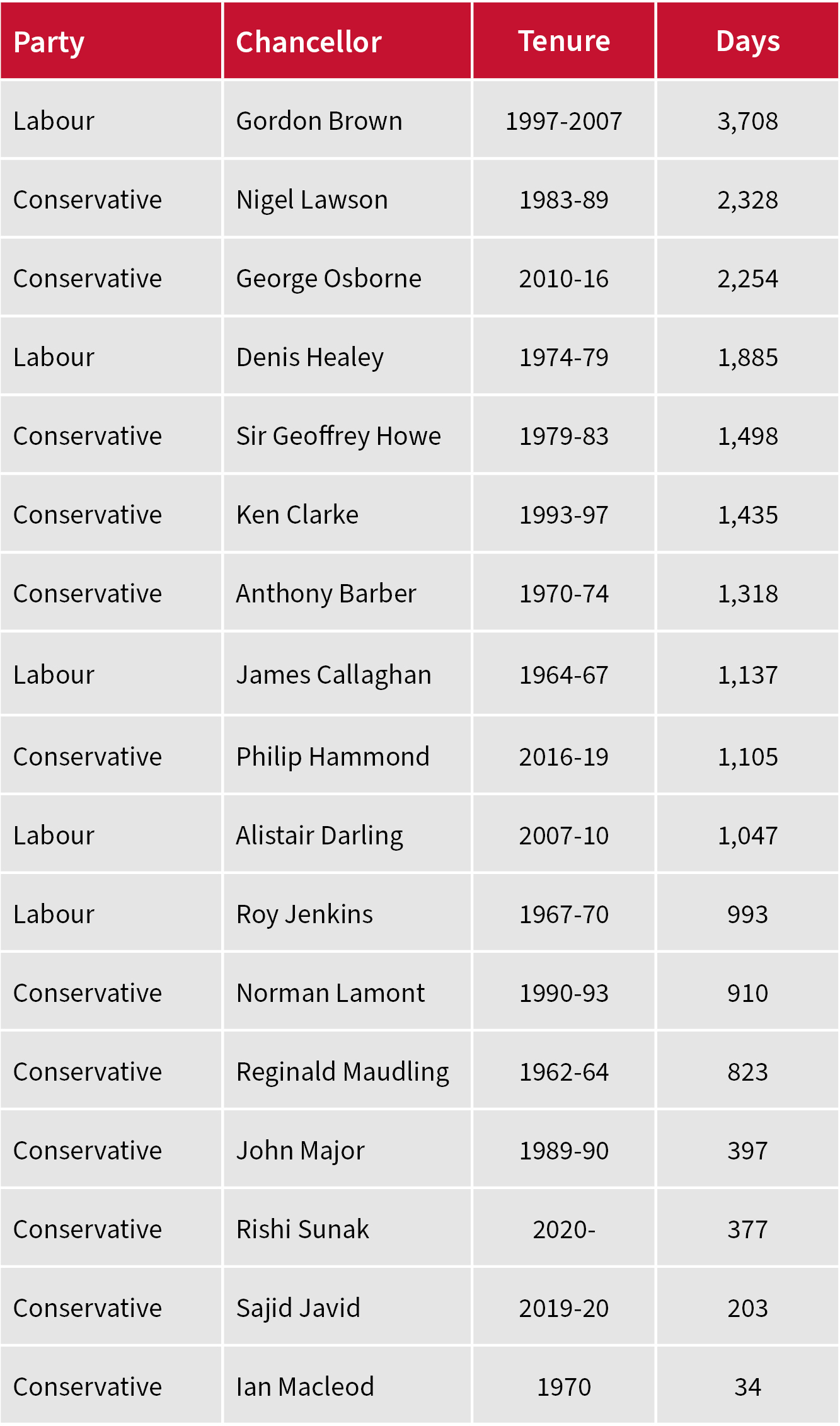

Since the inception of the FTSE All-Share index in 1962, the UK has had 17 Chancellors, 12 of whom have been Conservative and five Labour. The longest term in office was that of Labour’s Gordon Brown, the shortest that of the Conservatives’ Iain Macleod, who held the post for barely a month before his sudden, unexpected death.

There have been 17 Chancellors since the launch of the FTSE All-Share

Source: gov.uk

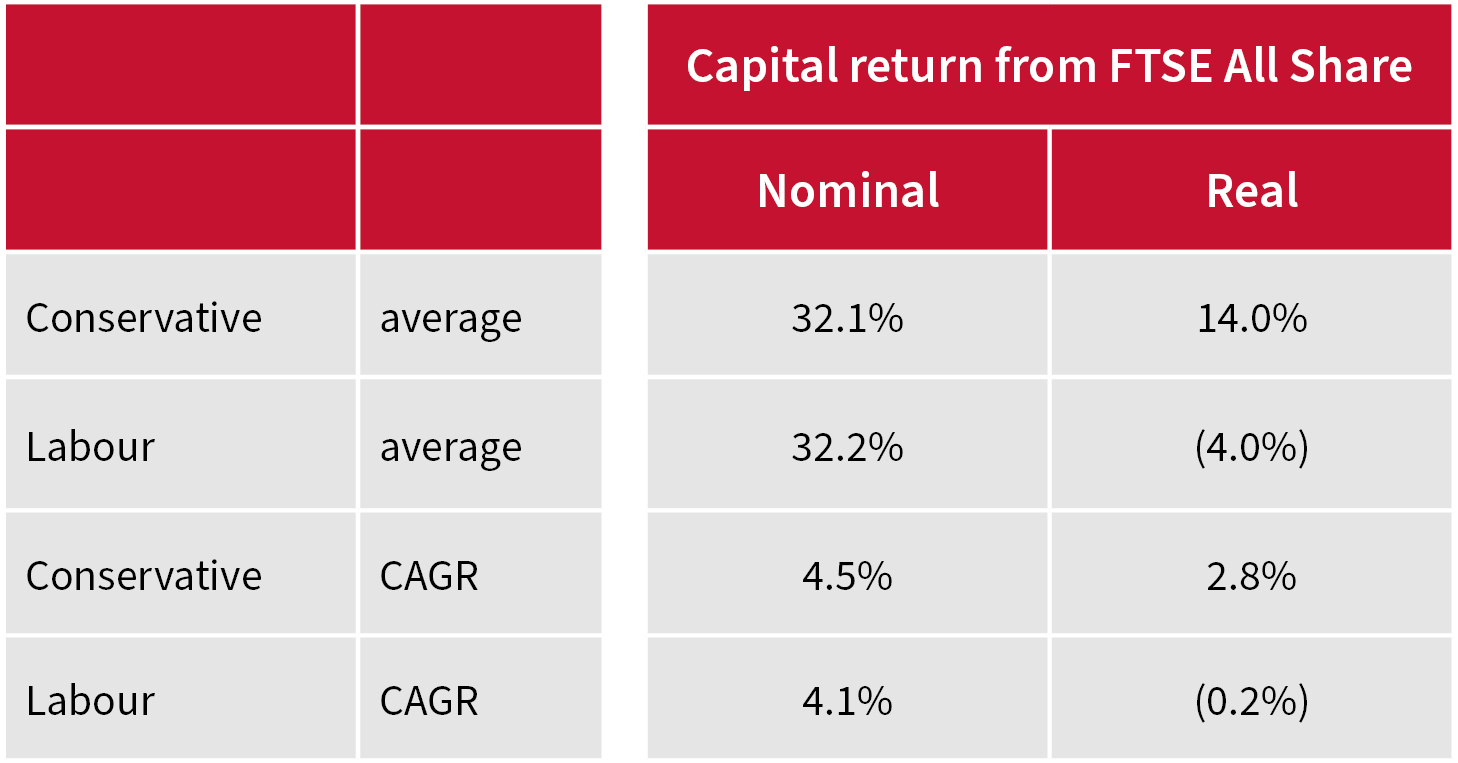

At first glance, there is nothing in it between the two parties. Under Conservative Chancellors, the FTSE All-Share has chalked up a total capital gain of 355%, in nominal terms.

That equates to an average advance per Chancellor of 32.1% (including Mr Macleod’s brief term with that of his successor, Anthony Barber), while under Labour the benchmark has risen by 161% for an average gain of 32.2%.

Across 34 years of Tory Chancellorships, that is a compound annual growth rate (CAGR) of 4.5% against 4.1% under 24 years of Labour in 11 Downing Street, and two of the top-five best spells under a single Chancellor actually come under Labour – again in nominal terms.

Party affiliation of Chancellors does not affect historic All-Share capital returns in nominal terms…

Source: Refinitiv data, gov.uk

However, the picture changes profoundly when inflation is taken into account and capital returns from the FTSE All-Share are assessed in real (post-inflation) terms rather than nominal ones.

“In real, rather than nominal, terms, Conservative chancellors come out well on top, as the withering effect of inflation upon investors’ returns from the stock market under Labour’s Healey Chancellorship of the mid-to-late 1970s comes into play.”

Here, Conservative chancellors come out well on top, as the withering effect of inflation upon investors’ returns from the stock market under Labour’s Healey Chancellorship of the mid-to-late 1970s comes into play.

… but it does seem to do so once inflation is taken into account

Source: Refinitiv data, www.gov.uk

It must be noted that inflation also chewed up the nominal gains made by the FTSE All-Share under the Tory Chancellors Sir Geoffrey Howe (1979–83) and Tony Barber (1970–74).

Investors will be looking for any return of inflation under Sunak

Source: Refinitiv data, gov.uk. Adjusts nominal return by change in the retail price index (RPI) as CPI data only goes back to January 1989 in current format.

“As financial markets today ponder whether inflation is about to make a return, and the yield on the benchmark UK 10-year bond, or Gilt, rises as prices fall, a repeat of the Barber Boom is something that Mr Sunak will be determined to avoid, even if he will be looking to support and boost growth as best he can.”

As financial markets today ponder whether inflation is about to make a return, and the yield on the benchmark UK 10-year bond, or Gilt, rises as prices fall, a repeat of the Barber Boom is something that Mr Sunak will be determined to avoid, even if he will be looking to support and boost growth as best he can. The economic fallout that followed was very painful for the UK – so painful that the Tories fell from office after a pair of General Elections in 1974.

Not all of the inflation that tore through the British economy in 1973–94 could be laid at the door of Mr Barber’s policies, as the 1973 oil price shock had a huge amount to do with it, and this highlights the importance of factors which are beyond the control of any Chancellor, no matter how diligent or skilled.

Alastair Darling could hardly have expected to inherit the Great Financial Crisis which prompted a deep recession and a wicked bear stock market. Norman Lamont inherited British membership of the Exchange Rate Mechanism, fought to defend the pound and a policy in which he did not believe and oversaw a devaluation of sterling which actually helped the FTSE All-Share to rally. Mr Sunak has had to contend with COVID-19 and the worst recession for three centuries, so perhaps he has been given the worst hand of all.

Even so, advisers and clients, looking at the world through the narrow perspective of their portfolios, will be wanting Mr Sunak to think back to Barber. Inflation mangled portfolio returns for much of the 1970s and all the way through to the Thatcher-Howe Prime Minister-Chancellor team of 1979–83. Bizarre as it may sound, markets may therefore want to see a little inflation – and growth – but not too much, especially as any sustained surge in prices could force bond yields higher and even oblige the Bank of England to act and raise interest rates.

Markets came close to falling out of bed last week, as they pondered such a prospect, so as ever Mr Sunak has a difficult balancing act going forward, as he juggles growth, jobs, the deficit and inflation, as well as votes.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.