The SpaceX initial public offering (IPO) continues to stimulate debate over the structure of the deal; the company’s valuation; whether it will prompt rivals to also come to market; the direction of the Artificial Intelligence (AI) industry; how AI’s development is to be funded; the impact of AI spending and investment on the economy and jobs, good or bad; and whether all of this means stock markets, or at least the AI- and technology-related parts of them, are in bubble territory.

All views on all of these topics are subjective, especially the one on the subject of SpaceX’s equity valuation, and this column has no intention of preaching one way or the other, not least because it does not have a crystal ball.

However, bearing in mind legendary, if now retired, investor Warren Buffett’s aphorism that, “Rising prices are a narcotic that affects the reasoning power, up and down the line,” it may be worth trying to step back from the pushing and shoving between the bulls and the bears and look at the potential wider implications for strategic asset allocation in advisers’ and clients’ portfolios.

Space X does not affect just Mr Musk’s personal wealth and the development of the space and AI industries, but the wider economy and also stock markets. Colossal investment in the data centres that drive the Large Language Models (LLMs) that power AI, and all of the construction work and components behind them, from silicon chips to cables to cooling kit to earthmovers, is boosting US GDP right now.

The idea is also that AI drives long-term growth thanks to productivity gains, although questions over the expense of developing and using the services remain – and the technology must prove that energy, water and mineral resource restraints do not mean the cost of usage offsets the benefits, which could include lower wage bills and smaller, if more efficient, workforces.

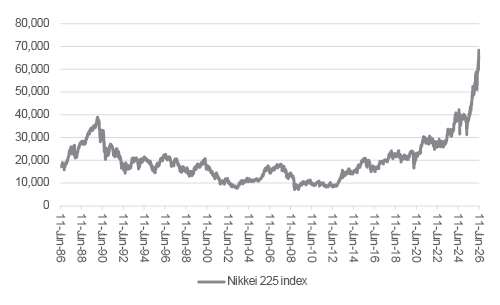

Bears will growl about malinvestment to match the Japanese property bubble of the 1980s, the global internet bubble of the 1990s and US real estate boom of the early 2000s, and this remains a risk. An investment bust to match those could have deleterious consequences for the real economy as well as the financial one, where any downturn could play to the nay-sayers’ fears a bubble is forming.

Source: LSEG Refinitiv data

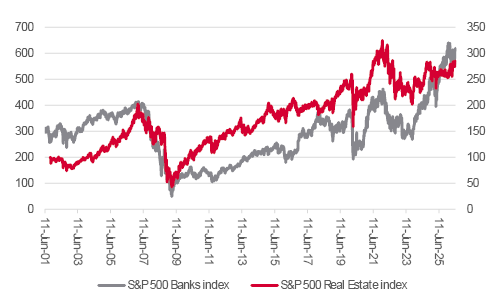

Source: LSEG Refinitiv data

Stock markets do trade at or near all-time highs across many benchmark indices, and SpaceX’s initial $1.8 trillion stock market capitalisation makes it the eighth- biggest company in the world using this valuation benchmark. Twelve of the world’s fourteen biggest firms by market cap are technology- or AI- related in the form of NVIDIA, Alphabet, Apple, Microsoft, Amazon.com, TSMC, Broadcom, SpaceX, Tesla, Meta Platforms, Samsung Electronics and Micron. The only exceptions are oil major Saudi Aramco and Berkshire Hathaway.

Such a skew does seem reminiscent of prior episodes where one industry, sector or group of companies fired investors’ imaginations and came to dominate sentiment and stock market indices as a result. Others include the ‘onics and ‘tronics stocks of the late 1960s in the US; America’s Nifty Fifty in the early 1970s; technology, media, and telecom stocks worldwide in the late 1990s; and residential real estate and mortgage-lending specialists in the early 2000s.

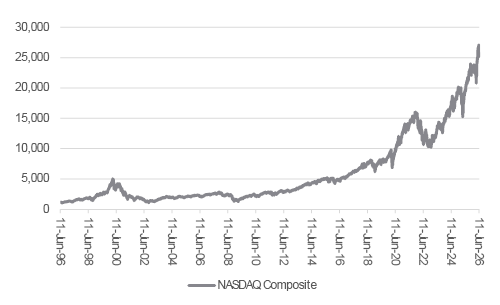

All of those were rewarding for supporters during the boom and deeply painful during the subsequent bust. Spotting the turning points is the hard bit. Anyone who went bearish on the technology-laden NASDAQ Composite in June 1999 at 2,500, on the grounds it had shot up by 70% in nine months, eventually looked pretty smart, given how the index bottomed at 1,114 in autumn 2022 and took until 2015 to recapture its eventual high. But in the meantime, the benchmark did motor from 2,500 to a peak of 5,048 in March 2000 to leave any bears looking very foolish for another nine months, while the internet, mobile telecoms technology and semiconductors eventually delivered everything of what investors thought they were capable – and then so much more besides.

Source: LSEG Refinitiv data

Market timing is a fiendish business, as noted by another retired money management titan, Fidelity Magellan fund’s Peter Lynch, when he asserted that, ‘Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.’

Selling everything in a particular asset class and then buying it all back is not practical, for reasons of expense, liquidity, and tax, as well as market timing. But exposures can be adjusted and flexed to help calibrate risk, protect wealth, and potentially augment it, so advisers and clients might like to use this checklist as a guide to where they think tech and AI stocks, and equities more generally, may be in this particular upcycle.

Based upon both 35 years’ experience in the markets and extensive reading about prior cycles, helped by the work of writers such as Charles P. Kindleberger, Edward Chancellor and Jeremy Grantham, it is presented without comment. Classic developments in the later stages of an equity bull market – and especially a bubble – can include:

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.