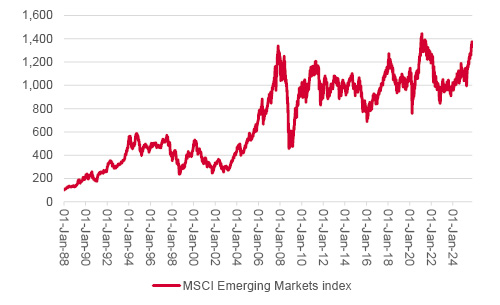

This column has little truck with technical analysis, or the study of price charts, and prefers to stick to what it sees as the firmer ground of fundamental research and valuation, but it has learned one lesson (often the hard way) over the last thirty-plus years: watch out for break-outs beyond prior all-time highs, as they can often presage dramatic further moves.

In this respect, the MSCI Emerging Markets (EM) equity index’s rapid move toward its 2021 zenith is eye-catching, and all the more interesting because so few people seem to be talking about it, given how America and AI-related stocks continue to hog the headlines.

The MSCI Emerging Markets index is nearing a new all-time high

Source: LSEG Refinitiv data

In some ways this raises the stakes for 2025’s version of the annual Asia-Pacific Economic Cooperation (APEC) forum, which is due to take place in Gyeongju, Korea at the end of this month. This year’s themes are connectivity, innovation and prosperity and all three are linked in some way shape or form to trade, tariffs and thus President Trump. Markets continue to expect a meeting between him and China’s President Xi at this event, or at a time adjacent to it, and the outcome of that could shape sentiment toward emerging markets for some time to come.

Yet EM equities are prospering even as key markets such as India and China continue to bear the brunt of American trade policy and there are three possible reasons for this.

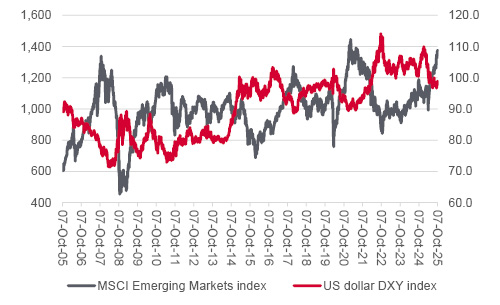

A weaker dollar is traditionally seen as bullish for EM assets

Source: LSEG Refinitiv data

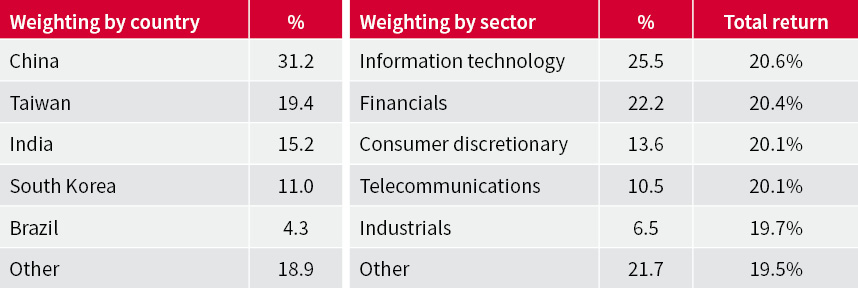

MSCI Emerging Markets index’s country and sector mix

Source: MSCI

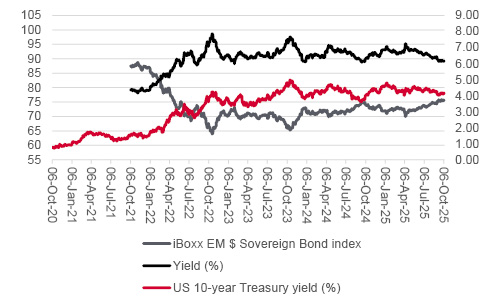

EM fixed-income markets are paying attention, too. Many EMs went through a major debt crisis in the late 1990s, and the memories have persisted. The result is that many EM sovereign balance sheets carry much lower debt-to-GDP ratios than DMs like the US, France, or UK, who are looking to policies to help then salt down that very same ratio.

The iBoxx EM Sovereign Bond index is on a run, and the running yield on the benchmark is down to just above 6%. The spread over ten-year Treasuries is down to 2.02%, though, down from this decade’s high of 3.7 percentage points, so advisers and clients must decide whether that provides them with sufficient compensation for the risks involved, even allowing for the tattered nature of many Western government balance sheets.

The spread between EM sovereign yields and US Treasuries continues to narrow

Source: LSEG Refinitiv data

And risks do remain. Trade tensions between the US and India and China remain high. China continues to grapple with a real estate bust and is looking for way to improve upon what are, for Beijing, modest rates of GDP growth – and the needs of the ruling Communist Party will always come before those of (overseas) shareholders. The Indian equity market is paddling sideways as it waits for earnings to grow into the lofty multiples afforded to the BSE Sensex index by investors. Argentina’s experiment with hair-shirt austerity is wobbling, to perhaps impede Latin America’s right-ward political swing, a prospect to which investors have warmed, while Eastern Europe continues to look over its shoulder at events in Ukraine. One day, the US Federal Reserve may even get tough on inflation, and financial markets hike rates rather easing policy at the first sign of trouble, to the benefit of the dollar and detriment of EMs. A unexpected global slowdown or recession could also dampen risk appetite and mean all emerging bets are off.

Nothing can be taken for granted. But the outcome of any Trump-Xi summit, and the fine details, should be scrutinised closely, especially if it turns out that America had a little less leverage than it thought. The White House’s dash to buy stakes in rare earth mineral producers so it can guarantee supply, and China’s increasing independence from the US in areas such as silicon chips and AI, suggest this could yet be the case.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.