To talk about asset prices during a time of strife and humanitarian suffering feels more than just a little trite, so there is a bigger picture here. But the matter of clients’ financial health and wealth is not a trifling one, either, and from the very narrow perspective of financial markets one issue related to the Middle Eastern conflict that continues to exercise minds is the trajectory of oil and gas prices.

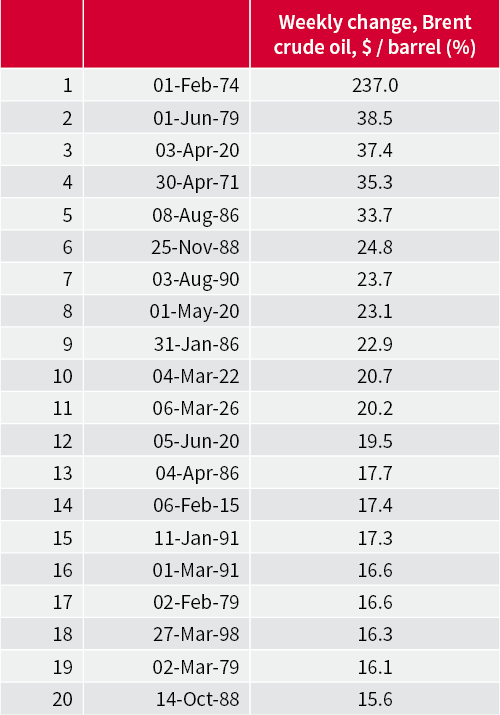

Wars and oil price shocks in 1973, 1979 and 1990 shook markets and the global economy alike, as these periods ushered in inflation, or even stagflation, as well as higher interest rates, a recession or two and asset price volatility.

In this context, it is worth considering several potential scenarios this time around, and to do so bearing in mind the aphorism from the legendary New York Yankees’ baseball player, Yogi Berra, that “it’s tough to make predictions, especially about the future.”

Within the very confined context of global markets, advisers and clients do know that five of the world’s ten largest oil producers are to be found in the Middle East, in the shape of Saudi Arabia, Iraq, Iran, the UAE and Kuwait, while a fifth of global crude supplies are shipped through the Straits of Hormuz. In addition, Qatar is one of the three largest exporters of liquified natural gas. Any sustained conflict could conceivably affect supply.

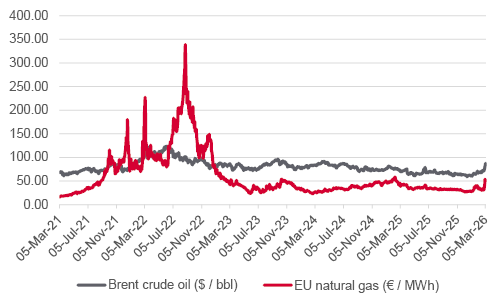

This helps to explain why the price of Brent crude oil is up by a fifth and the European benchmark for natural gas, the Dutch TTF price, by nearly two-thirds since the outbreak of fighting.

Source: LSEG Refinitiv data

The good news, however, is that these moves still pale next to the ones witnessed in the early and late 1970s, which came after the Yom Kippur war and resulting Arab oil embargo and the fall of the Shah of Iran, respectively.

Source: LSEG Refinitiv data

The bad news is that this month’s move is close to that which followed Iraq’s attack on Kuwait and 1990’s First Gulf War. The surge in the Dutch TTF gas price cannot be dismissed either, because Europe and the globe now rely more heavily upon gas more than they do upon oil.

The question now is whether the commodity prices make sustained gains after a lengthy period in the doldrums. The increases of 2022, in the wake of the Russian attack on Ukraine, did not last long, after all, but the after-effects upon inflation, interest rates and consumer confidence lingered, and can be felt even now.

The rebound in global equities, and relative calm across sovereign bond yields, suggests markets still feel the war will not last long, and that the increase in hydrocarbon prices will peter out.

The risk, therefore, is that the conflict drags on beyond this month, or even gets worse, either because other nations across the region join in, or Iran descends into the sort of chaos that characterised Iraq, Libya and Afghanistan this century after American, or multi-national, military intervention.

Markets have thus far sought protection from the tail risks with some sporadic, indiscriminate selling, generally of assets that had done well and offered sufficient liquidity to facilitate a quick escape from profitable positions, such as US and South Korean equities and even gold.

Increasing allocations to cash provides one form of protection, and welcome optionality in the even of a wider market dislocation, but it also exposes clients and advisers to the risk of inflation, should hydrocarbon prices stay high, or go higher.

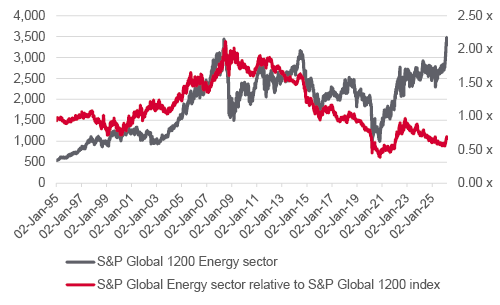

One bolthole to consider could therefore be energy equities. The Energy sector is ranked first of eleven super-sectors that make up the S&P Global 1200 index on a twelve-month view, but this is after years in the doldrums which leave the sector trading near all-time relative lows compared to global benchmark.

Source: LSEG Refinitiv data

This improved momentum may have been the result of value-hunters looking for potential bargains, or even investors rebalancing their portfolios away from technology companies on the grounds of valuation, worries over the spending boom on Artificial Intelligence and indeed the potential impact of AI upon many companies’ business models, including software specialists.

It may have also reflected wider worries about supply chains and security of access to vital raw materials, an issue raised by COVID-19 and brought into even clearer relief by the Russian attack on Ukraine and the subsequent jousting over rare earths and minerals between America and China. Either way, someone is paying closer attention to energy stocks (and who can blame them when all economic activity is, in effect, the transformation of energy into goods and services).

In this respect, the much-criticised UK equity market may be better placed than many. Oil majors BP and Shell represent some 10% of the FTSE 100’s stock market capitalisation, a figure which compares to barely 4% across the S&P Global 1200 and just 3.2% in the S&P 500.

Moreover, analysts think they will generate between 10% and 12% of the total profits and cash returns expected from the index in total in each of 2026 and 2027. That factors in little or no upside from higher oil and gas prices, and the UK could therefore offer some protection if the war does it worst, in every sense, even as we must all bear in mind American economist Joseph Stiglitz’s warning that, “The only perfect hedge is in a Japanese garden.”

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.