This column is not a specialist in the field of technical research, and the taking of signals from price charts, but two things jump out from a graphic which shows the trajectory of the MSCI Emerging Markets (EM) equity index, even to the most casual observer.

Source: LSEG Refinitiv data

Emerging stock markets have a weighting of around 10% in the FTSE All-World equity index, which is big enough to oblige advisers and clients to take a view, one way or the other, within the equity portion (and perhaps even the fixed-income element) of balanced portfolios, now that EMs may finally be coming in from the cold, after suffering more than a decade of indifference.

No-one can, in all honesty, pretend to know what America’s President, Donald J. Trump, is going to say, or do, next, or what the full asset allocation and portfolio implications of his policies on issues such as Greenland, interest rates and the US Federal Reserve and tariffs and trade could be.

In this context, it must be borne in mind that the US stock market is trading in the top ten percent of valuation ranges on any metric advisers and clients care to mention, relative to their history.

As such, US equities are not priced for any sustained bout of turbulence, be it geopolitical, economic or financial. It would be logical to expect any advisers and clients who are of a nervous disposition, and fear further policy, and financial market, volatility to consider doing one of two things:

Intriguingly, US assets have gently underperformed since December 2024, when the S&P 500’s market capitalisation peaked at 64.3% of that of the FTSE All-World index. That weighting now stands at 60.0%.

Perhaps markets are already subtly sending the message that the era of US exceptionalism is fully priced in, and there may be better value to be had elsewhere, especially as the S&P 500 topped out at 59.2% of the All-World benchmark in early 2002, by which time the technology, media and telecoms (TMT) bubble had already started to burst.

One area which may be worthy of further research, at least for risk-tolerant contrarians, is emerging markets, given the momentum in absolute terms and the value which may be on offer, at least compared to the USA, in relative terms.

The past, as all advisers and clients know, offers no guarantees for the future.

But a weaker dollar is traditionally seen as a boost for emerging markets, as it makes it easier for those nations who borrow in dollars to service their debts, and rising commodity prices can be a tailwind for them, too, as many developing nations are major producers of precious and industrial metals, as well as oil and gas and agricultural crops.

And, right now, the dollar is weakening, and many commodities are surging to all-time, or at least multi-year highs, most notably gold, silver, copper and platinum.

Careful research is still required, as emerging markets are not homogenous by any means, and they come with a range of risks, including politics, currency movements, corporate governance and how easy it is (or otherwise) to buy and sell on local exchanges.

Advisers and clients could be forgiven for seeking broad-brush exposure via actively or passively managed funds, which will provide access to a basket of countries and industry sectors in either equities or bonds, or both, rather than tackling the nitty-gritty of individual stock selection, if they feel these arenas fit with their long-term strategy and portfolio allocation.

But it is possible that at least some of those not-so-hidden dangers are already factored into emerging market valuations.

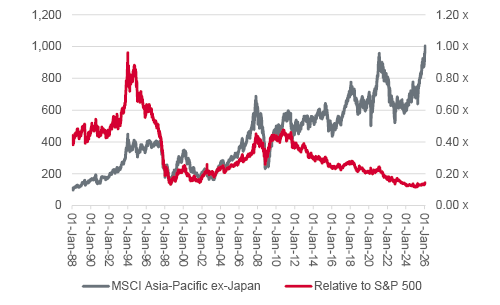

The MSCI Asia-Pacific ex-Japan index is currently benefiting from the technology exposure provided by Taiwan’s TSMC, Korea’s Samsung Electronics and SK Hynix and the AI magic dust associated with Chinese internet giants Alibaba and Tencent. The index is hitting new all-time highs, but the index’s relative rating compared to the S&P 500 is near historic lows.

Eastern Europe may just be too tricky for some, given the proximity of the war in Ukraine and the imposition of sanctions upon Russia in 2022 after Moscow’s invasion of its neighbour.

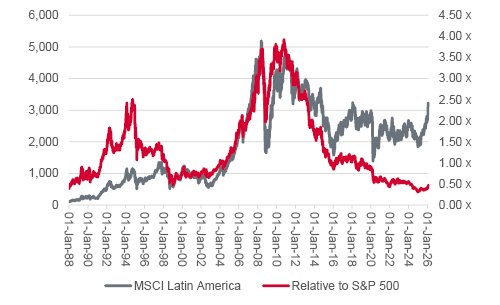

Latin America has a tiny weighting in the All-World indices, with Brazil, Chile, Colombia and Mexico chipping in barely 1% of the benchmark’s capitalisation.

But the MSCI index is rallying, helped by a right-ward shift in politics in Argentina, Peru and Bolivia, scope for interest cuts as reforms put a lid on inflation and strong industrial and precious metal prices.

The old gag about emerging markets deserving the name because advisers and clients cannot emerge from them unscathed, or quickly, enough in the event of trouble still gets a smile for good reason. Risks do abound. A strong dollar would be one challenge, an unexpected global economic slowdown another, while country-specific challenges from politics to corporate governance can catch out the unwary.

But the reflationary power of falling US interest rates and a weaker dollar could yet offer a timely boost, just when advisers and clients may be questioning US equity valuations and the dominant role played by US- and dollar-denominated assets in so many portfolios.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.