In the coming week (22-24 October), Russia will host the latest annual BRICS summit in Kazan. For all that one of the meeting’s key goals is to tackle neglected tropical diseases, few investors may be inclined to pay attention, not least given the economic sanctions imposed upon the host nation. The concept of the Brazil, Russia, India, China and South Africa (the BRICS) as an investable grouping is not as popular as it was either, more than twenty years after (then) Goldman Sachs (GS:NYSE) banker Jim O’Neill first coined the phrase, partly because of geopolitical, or local political, trends; partly because of economic woes, notably in South Africa; and partly because of the bursting of stock market and then property bubbles in China in 2015 and 2023 respectively.

Yet India’s headline Sensex stock market index trades at all-time highs, as does Brazil’s BOVESPA and South Africa’s JSE All-Share benchmark. China has been the one to let the side down, as until recently the CSI 300 had traded no higher than it did in 2007.

“It remains to be seen whether the recovery can be sustained, but this is a timely reminder that Emerging Markets (EM) overall have underperformed Developed Markets (DM) for more than a decade.”

Fresh measures from Beijing to stimulate its flagging economy have given the headline indices in Shanghai and Hong Kong a huge boost, as they have gone from worst to first among global equity benchmarks in 2024. So downbeat was sentiment, and so lowly were valuations, that it took relatively little to stoke fresh interest. It remains to be seen whether the recovery can be sustained, but this is a timely reminder that Emerging Markets (EM) overall have underperformed Developed Markets (DM) for more than a decade.

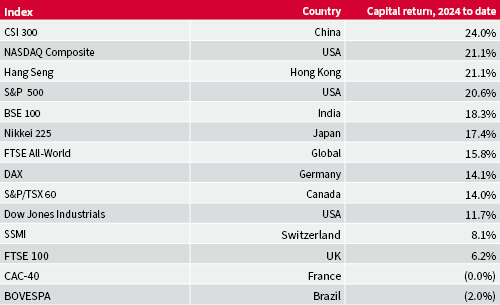

China is now the best performing major equity market in 2024

Source: LSEG Refinitiv data, as of 9 October 2024

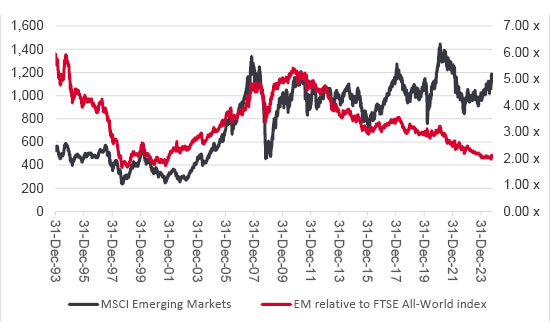

“On a relative basis, EM trade no higher now compared to DM than they did in 2001, after which point the bursting of the tech bubble and return to favour of cyclical, value stocks brought EM back into favour.”

On a relative basis, EM trade no higher now compared to DM than they did in 2001, after which point the bursting of the tech bubble and return to favour of cyclical, value stocks brought EM back into favour.

Emerging Markets trade at two-decade relative lows compared to Developed Markets

Source: Sharepad, LSEG Refinitiv data

Contrarian advisers and clients could therefore be forgiven for asking themselves whether it is now time for a fresh look at EMs, given how the world is once more in thrall to tech stocks and US equities in particular.

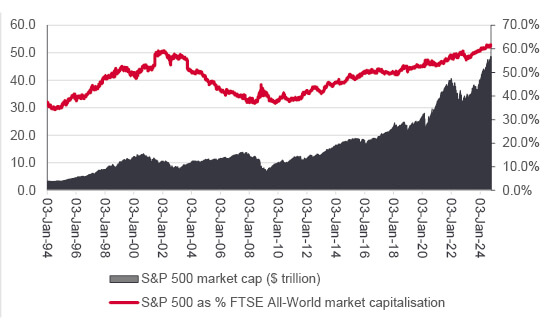

US equities represent more than 60% of global market capitalisation

Source: LSEG Refinitiv data

“China and Hong Kong have given one hint of what could be a potential catalyst for stronger performance from EMs, in relative and absolute terms, namely fiscal and particularly monetary stimulus.”

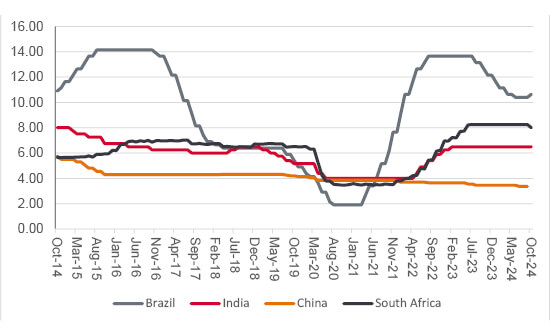

China and Hong Kong have given one hint of what could be a potential catalyst for stronger performance from EMs, in relative and absolute terms, namely fiscal and particularly monetary stimulus. Beijing has cut interest rates, lowered the amount of capital that banks have to hold (so they can lend more) and eased the rules on consumer purchases of property. There is still much more to do, if China is to sustainably boost growth and ensure that consumption becomes its main economic engine instead of construction and exports, and the July’s proposals for land reform at July’s Third Plenum offer a hint of what may be to come. More widely, interest rate cuts could help EMs, whose central banks were generally quicker to hike headline borrowing costs as inflation broke out in the wake of the pandemic. They now have scope to cut rates, especially as the US Federal Reserve has started to do the same. EMs have had to wait, because their currencies would have weakened (and given inflation fresh impetus) had they moved before the Fed.

Lower rates could boost local GDP growth and benefit corporate earnings across markets which can be heavily exposed to cyclicals and financials, and other economically sensitive sectors, either domestically or across international markets.

EM central banks have the chance to cut interest rates

Source: LSEG Refinitiv data

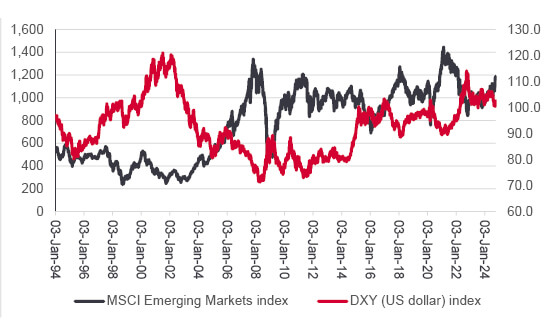

“A drop in the buck, as benchmarked by the trade-weighted DXY (or ‘Dixie’) index, is traditionally seen as helpful for EMs, especially those with dollar borrowings.”

If the Fed really gets going on interest rate cuts, then the dollar could weaken. A drop in the buck, as benchmarked by the trade-weighted DXY (or ‘Dixie’) index, is traditionally seen as helpful for EMs, especially those with dollar borrowings. Lower rates and a softer dollar lower the cost of servicing those overseas debts and the reduced interest bills leave scope for more pro-active government investment elsewhere.

EM equity markets traditionally do well when the dollar is weak

Source: LSEG Refinitiv data

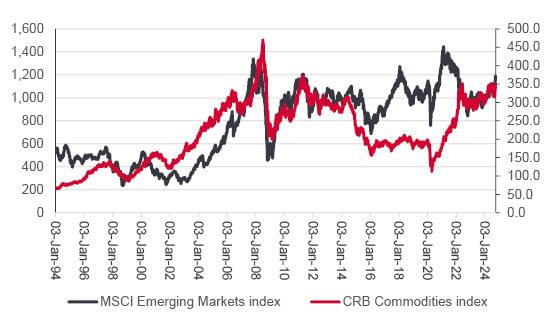

“If interest rate cuts and a weaker dollar are two possible catalysts for improved EM equity market performance, then a third is strength in commodity prices.”

If interest rate cuts and a weaker dollar are two possible catalysts for improved EM equity market performance, then a third is strength in commodity prices.

This could reflect how some EMs are key producers and exporters of raw materials, notably Brazil and South Africa. It may also be the result of how EMs are plugged into global growth more widely through their exports (and if global growth is strong then demand for commodities is likely to be elevated). Commodities can also do well when inflation is running strongly, as investors seek havens and assets that can protect wealth relative to cash and paper assets, and also feel less inclined to pay up for secular growth assets when cyclical growth is more freely (and probably cheaply) available from value plays, such as EM.

EM equity markets traditionally do well when commodity prices are strong

Source: LSEG Refinitiv data

The dangers to EM are therefore that the US cuts rates more slowly than thought, the dollar gains ground, inflation remains subdued and commodity prices soften, to continue the world’s love affair with tech and America – in other words, the trends of the last two decades continue for the next one. Investors can only decide for themselves how likely they think this is.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.