There are two ways to look at the second Trump Presidency.

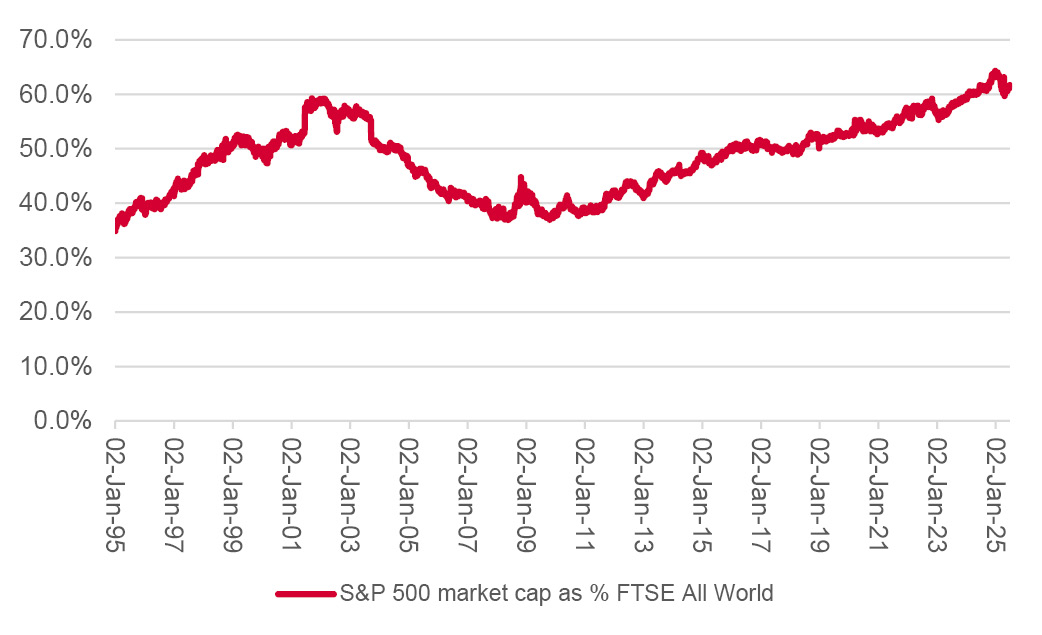

US equities still dominate global equity market capitalisation

Source: LSEG Refinitiv data.

A clear choice between those potential scenarios will at least provide investors with a framework for deciding whether current portfolio allocations are sufficiently well balanced to protect, and have the scope to augment, their savings and wealth.

“It is not hard to see why the dollar, as benchmarked by the trade-weighted DXY index, nicknamed ‘Dixie’, is losing ground in the second Trump Presidency.”

It is not hard to see why the dollar, as benchmarked by the trade-weighted DXY index, nicknamed ‘Dixie’, is losing ground in the second Trump Presidency.

The dollar continues to slide

Source: LSEG Refinitiv data.

Further dollar declines therefore are not impossible, especially as the DXY sits a lot nearer the top of its twenty-year trading range than the bottom. That said, currencies do have a habit of self-correcting, as a decline can help exports, drive growth and increase inflation, and thus force higher interest rates which should, by rights, serve to attract capital once more. Advisers and clients must also be aware that the bear case usually seems most compelling at or near the bottom.

“Those who do fear, or expect, a weaker dollar or believe that the post-Financial Crisis era of American exceptionalism is ending may therefore be left looking for alternatives to the USA.”

Those who do fear, or expect, a weaker dollar or believe that the post-Financial Crisis era of American exceptionalism is ending may therefore be left looking for alternatives to the USA.

Can emerging markets finally turn the corner after fifteen years of underperformance?

Source: LSEG Refinitiv data.

It may not therefore require a huge leap of imagination to see why China and Hong Kong, Brazil (and the UK and Europe) sit above the USA in terms of stock market performance in 2025 date. Emerging markets in particular have been in the doldrums for so long and they still offer long-term growth potential. Research from GaveKal and Aubrey Capital Management shows that 69 of the world’s 100 cities lie within a four-hour flight of Hong Kong, a circle that holds half the world’s population. Demographic trends are favourable, income trends are positive and technological innovation is evident in everything from China’s excellence in electric vehicle batteries to Indian prowess in software development.

“Those advisers and clients who a keen sense of market history will also be aware of the historical inverse relationship between the dollar and emerging market equities.”

Those advisers and clients who a keen sense of market history will also be aware of the historical inverse relationship between the dollar and emerging market equities. The past is no guarantee for the future, but a softer greenback has tended to help emerging markets in the past, as it eases the burden on developing economies’ overseas debts and enables them to spend the money on themselves rather than on interest for lenders.

“Another asset class which has tended to do well during times of dollar weakness is commodities, not least because they are priced in the US currency.”

Another asset class which has tended to do well during times of dollar weakness is commodities, not least because they are priced in the US currency. They become cheaper to non-dollar users and lower prices tend to fuel higher demand, though, again, there is no certainty this pattern will repeat itself even if the dollar does go lower.

Gold’s all-time high may be no coincidence but it may also deter contrarians from getting heavily involved now. Silver, oil and platinum, to name but three, look cheap relative to gold on a historic basis and the wider CRB Commodities index continues to outperform equities almost unnoticed, some five years after forming a bottom relative to the FTSE All-World equity benchmark.

Was 2020 the bottom for commodities’ performance relative to equities?

Source: LSEG Refinitiv data.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.