Stock, bond, currency and commodity markets continue to try and second-guess what the implications are of President Trump’s trade and tariff policies. It is hard to be dogmatic – which may be part of the problem – but all we can probably say with any certainty is that 2024’s surge in US equity valuations reflected the view that inflation would cool, interest rates would fall, and growth would be steady in 2025 (and beyond).

“Anything in terms of tariff deals or concessions that gets the world back on track toward lower inflation, lower rates and steady growth is therefore likely to be seen as a good thing for share prices and anything that takes them further away may well be taken badly by equity investors.”

But Trump’s initial tariff moves in his second term are shaking faith in the rosy trifecta: inflation could be higher; interest rates may be falling more slowly than expected and the growth outlook is less clear. Anything in terms of tariff deals or concessions that gets the world back on track toward lower inflation, lower rates and steady growth is therefore likely to be seen as a good thing for share prices and anything that takes them further away may well be taken badly by equity investors.

The fixed-income markets may have a different view, however, and it is here that Trump, and Treasury Secretary Scott Bessent may be focusing their attention anyway. Thus far, Trump seems impervious to stock market volatility, in contrast to his first term, and willing to embrace some near-term pain in exchange for what he views as the long-term gain: higher revenues from tariffs, more jobs on US soil and higher growth with, further down the road, perhaps the chance to cut income taxes as a result.

Bessent seems equally determined, judging by his televised interview comments about the need for America’s economy, and companies, to wean themselves off their addiction to government spending.

“Whether we agree with them or not, therefore, it may pay to judge the efficacy of the White House’s policies more through the prism of the US government bond, or Treasury, market than via the S&P 500, Dow Jones or NASDAQ Composite equity indices.”

Whether we agree with them or not, therefore, it may pay to judge the efficacy of the White House’s policies more through the prism of the US government bond, or Treasury, market than via the S&P 500, Dow Jones or NASDAQ Composite equity indices.

Bessent appears concerned by four, interconnected, issues.

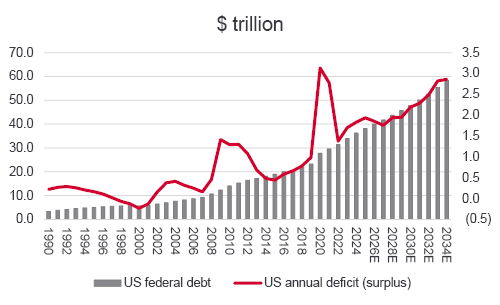

The US federal deficit continues to soar

Source: FRED – St. Louis Federal Reserve database, US Congressional Budget Office

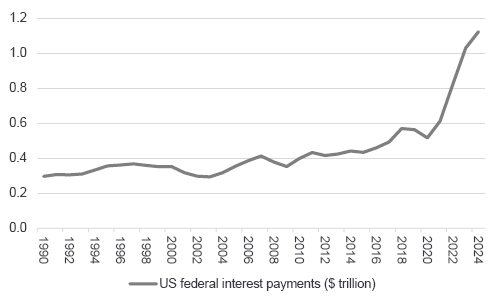

The interest bill is rocketing, too

Source: FRED – St. Louis Federal Reserve database, US Congressional Budget Office

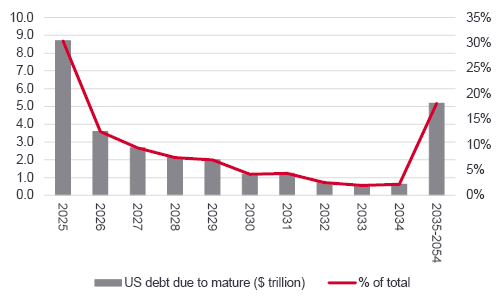

The maturity profile of US federal debt is short

Source: fiscaldata.treasury.gov. Based on publicly held debt only and excludes $7.3 trillion of intra-governmental holdings

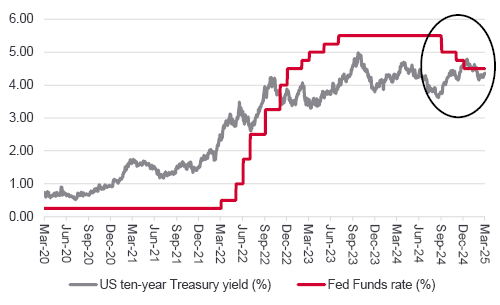

US benchmark Treasury yields are ignoring Fed rate cuts

Source: LSEG Refinitiv data, US Federal Reserve

All of these numbers focus the mind and mean America must at least make a good show of tackling the national debt. Otherwise, the cost of borrowing could soar and mean the interest bills either become so crushing they hobble the economy, or the US has to print its way out of trouble so it can pay, with all of the inflationary implications that has, even for the globe’s reserve currency.

This is also at a time when the US economy is growing. An unexpected recession would hit tax income, increase welfare spending, and make things look even worse.

“In this context it is easy to see why Trump and Bessent are focused on the bond market, not the stock market, because the stakes are potentially very high. At least they can draw some comfort from how the ten-year yield is no higher now than when Trump prevailed in the 2024 election, in contrast to the trends evident elsewhere.”

In this context it is easy to see why Trump and Bessent are focused on the bond market, not the stock market, because the stakes are potentially very high. At least they can draw some comfort from how the ten-year yield is no higher now than when Trump prevailed in the 2024 election, in contrast to the trends evident elsewhere.

Tough talk is helping to anchor US Treasury yields

Source: LSEG Refinitiv data

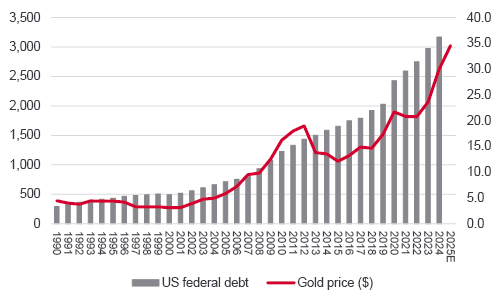

“And that could just be why gold continues to march higher, seemingly in lockstep with the US deficit, as investors seek a bolthole, just in case something really unusual develops.”

But the danger is that the sort of austerity promised by the Department of Government Efficiency’s spending cuts leads to the slowdown or recession that simply blows up the numbers, or at least forces some more highly unorthodox policies. And that could just be why gold continues to march higher, seemingly in lockstep with the US deficit, as investors seek a bolthole just in case something really unusual develops.

Gold seems to be pricing in an unorthodox solution to any debt drama

Source: LSEG Refinitiv data

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.