Much as this column would like to offer something which does not mention words such as ‘Trump,’ ‘trade,’ and ‘tariffs,’ it is rather difficult to do so, and at least the approach of the one-hundredth day of the President’s second term in office gives us chance to take stock.

At the time of writing, Trump’s second time in the White House looks set to give investors in US equities their roughest start to a new Presidency since the Second World War, using the S&P 500 index as a benchmark.

Trump’s second term could offer US investors the toughest start to any post-war Presidency

Source: LSEG Refinitiv data. * John F. Kennedy assassinated in November 1963 and replaced by Lyndon B. Johnson. ** Richard M. Nixon resigned August 1974 and replaced by Gerald R. Ford. ***Donald J. Trump up to 24 April 2025

“The imposition of blanket tariffs, an escalation of tensions with China and then a flurry of sidesteps and backtracks, as additional reciprocal levies are delayed, exemptions are provided for technology hardware and tentative olive branches are offered to Beijing leave everyone confused and seem to be shaking markets’ prior strong faith in American exceptionalism.”

This is a remarkable change of heart, given the rapturous welcome given to Trump’s election victory last November, when the S&P 500 (and the dollar) soared, while US Treasury yields remained stable. The imposition of blanket tariffs, an escalation of tensions with China and then a flurry of sidesteps and backtracks, as additional reciprocal levies are delayed, exemptions are provided for technology hardware and tentative olive branches are offered to Beijing leave everyone confused and seem to be shaking markets’ prior strong faith in American exceptionalism.

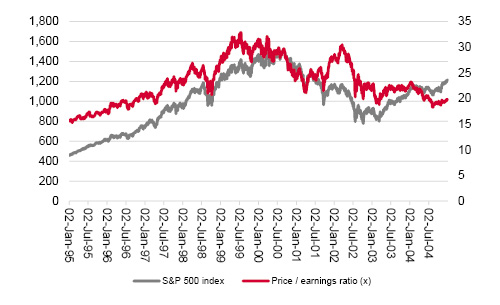

The outperformance of US equity indices, the concomitant surge in the stock market capitalisation of the S&P 500 to an all-time high as a percentage of global market cap, and the lofty (and in some cases record high) earnings multiples applied to the US market all reflected how markets thought America was already great.

Their reassessment of this view shows in how US indices have retreated and taken valuation multiples lower. Now advisers and clients must wait to see if corporate earnings start to weaken to provide another challenge.

“The good news is the data show a sticky start does not mean a Presidency is doomed to provide poor returns over its full term. Truman and Eisenhower’s first stints in office are clear about this. However, it is noticeable that the only Presidencies which offered beginnings as weak as this one presented what may be uncanny echoes of current circumstances.”

The good news is the data show a sticky start does not mean a Presidency is doomed to provide poor returns over its full term. Truman and Eisenhower’s first stints in office are clear about this. However, it is noticeable that the only Presidencies which offered beginnings as weak as this one also presented what may be uncanny echoes of current circumstances:

George W. Bush took office at an unpropitious time

Source: LSEG Refinitiv data.

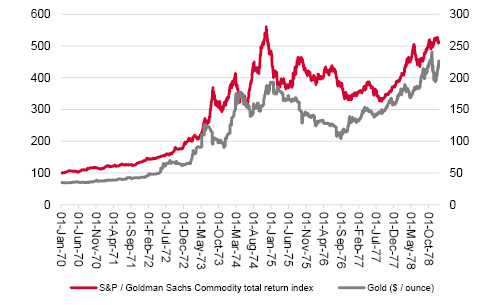

Gold and equities sheltered investors from the Nixon shock

Source: LSEG Refinitiv data.

“Trump’s determination to lessen America’s trade deficit, weaken the dollar and re-set global trade terms smacks of Nixon’s plan, and also comes at a time when Federal finances hem in the President, albeit this time in the form of record borrowing levels rather than the straitjacket of the gold standard.”

Trump’s determination to lessen America’s trade deficit, weaken the dollar and re-set global trade terms smacks of Nixon’s plan, and also comes at a time when Federal finances hem in the President, albeit this time in the form of record borrowing levels rather than the straitjacket of the gold standard.

Advisers and clients must now answer two sets of (inter-related) questions when they assess portfolio allocations:

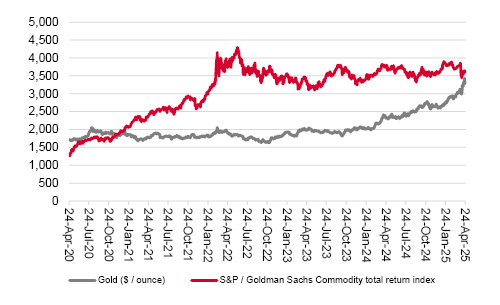

Gold and commodity prices are hinting at a major change in the macro backdrop

Source: LSEG Refinitiv data.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.