This Friday (23 July) heralds the one-hundredth anniversary of the first meeting of the Chinese Communist Party and the country’s leadership continues to mark its birthday with a series of high-profile events, speeches and actions.

Whether the centenary is anything that advisers and clients can mark with pleasure remains more of a moot point, even if the benchmark Shanghai Composite index trades some 15% above the levels reached just before the news of the pandemic seeped out of the Middle Kingdom in early 2020. These doubts persist for three reasons.

“China is trying to combat the economic fall-out of the pandemic and keep the economy going on the one hand with a combination of fiscal and monetary stimulus, yet seeking to avoid letting financial markets, asset prices and debt get out of hand on the other, thanks to that very same policy package.”

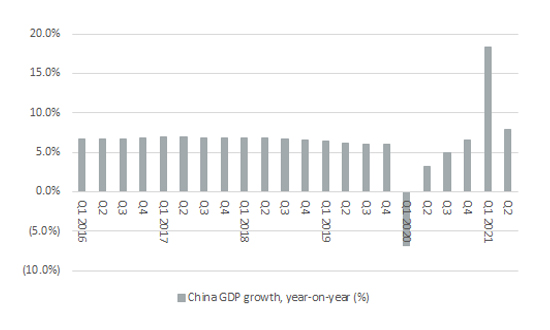

China’s second-quarter GDP growth rate slightly undershot economists’ forecasts

Source: National Bureau of Statistics of China, Refinitiv data

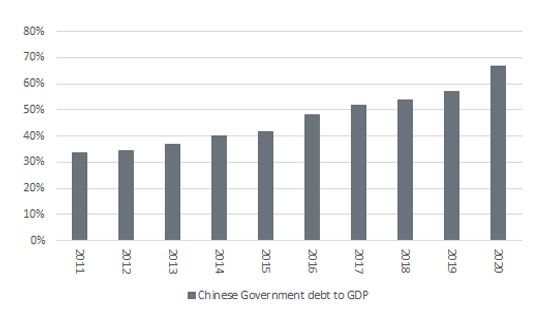

The last point is perhaps the easiest to tackle. Granted, China has a relatively low Government debt-to-GDP ratio of 67% but that number is rising quickly. Moreover, the opaque structure of Chinese State-Owned Enterprises, let alone the so-called shadow banking system, means the overall national debt-to-GDP figure is a less healthy 270%, according to China’s own National Institution for Finance and Development.

China’s debts continue to grow

Source: IMF

“The Shanghai Composite index is trading well below its 2007 and 2015 highs, even as the economy keeps expanding, to perhaps offer a timely reminder that advisers and clients should never use macroeconomic data alone when it comes to selecting which indices and funds (be they active or passive) to research and follow.”

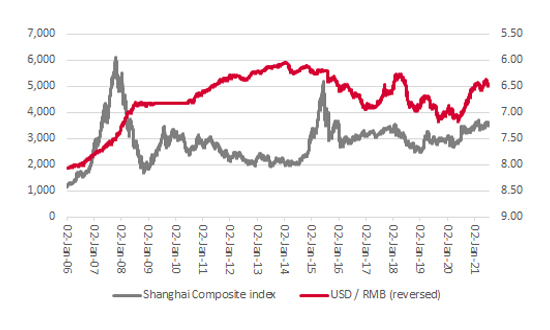

China may therefore be generating growth, but the quality of that growth looks questionable, given its reliance on fiscal stimulus and cheap debt. This perhaps explains why the Shanghai Composite index is trading well below its 2007 and 2015 highs, even as the economy keeps expanding in a timely reminder that advisers and clients should never use macroeconomic data alone when it comes to selecting which indices and funds (be they active or passive) to research and follow.

Strong economic growth is not translating into new stock market highs even as the renminbi ends a six-year slide

Source: Refinitiv data

In the interests of balance, it must be noted that China’s currency is trading relatively strongly against the dollar, after a six-year slide, so markets may not be too worried about the economic foundations (although again the US faces the same challenges).

“Geopolitical risk is something with which all advisers and clients must live but there is little they can do about it, barring factor it into the risk premiums they demand when buying assets in certain countries – or, in plainer English, pay lower valuations to compensate themselves for the potential dangers involved.”

Geopolitical risk is something with which all advisers and clients must live but there is little they can do about it, barring factor it into the risk premiums they demand when buying assets in certain countries – or, in plainer English, pay lower valuations to compensate themselves for the potential dangers involved. Sino-American relations remain strained, to say the least, as Beijing and Washington wrestle for supremacy in key industries, notably fifth-generation (5G) mobile telecommunications and semiconductors.

This is prompting talk of a new Cold War, a view perhaps supported by President Xi’s powerful speech on 1 July. Investors will be hoping it does not spill over into a hot war over Taiwan, for example, whose strategic importance is only heightened by the global semiconductor shortage.

“But if advisers and clients can do little about geopolitics, they can do everything when it comes to corporate governance or at least make sure that their selected fund managers do the donkey work for them. And perhaps the greatest concerns lie here, at least when it comes to Chinese equities.”

But if advisers and clients can do little about geopolitics, they can do everything when it comes to corporate governance or at least make sure that their selected fund managers do the donkey work for them. And perhaps the greatest concerns lie here, at least when it comes to Chinese equities.

Beijing’s indifference to the damage done to Didi Chuxing’s share price in the wake of the security investigation and assertion that US regulators cannot check Chinese audits of firms with listings in America is a big red flag (if you will pardon the expression). No-one, from a private individual to a trained fund manager, can invest in a firm if audited, verifiable and reliable accounts are not available.

This reminder that China has its own agenda – one that is designed to preserve the Communist Party’s hegemony well beyond the first hundred years – affirms that advisers’ and clients’ needs are secondary. They are welcome to keep buying stakes in Chinese firms, or funds which track Chinese indices or own Chinese equities, if they wish. But they need to be sure they are paying suitably lowly valuations to accommodate the potential risks, which should also be in keeping with their overall tolerance levels.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.