Wild swings in the price of oil and gas continue to transfix financial markets as they monitor the potential implications of the war in the Middle East from their very narrow perspective. Investors continue to ponder where hydrocarbon prices may settle and what the impact could be upon inflation, central bank interest rates and even global economic growth, especially if they stay elevated; oil is some 60% higher than when the war began and Europe’s Dutch TTF gas benchmark is up by 70%, at the time of writing.

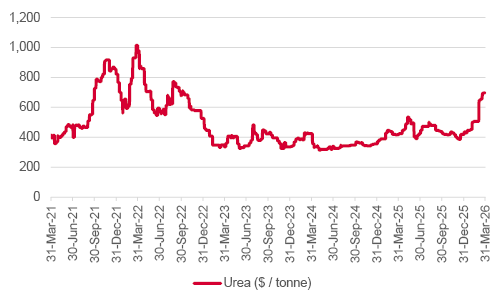

But there are other good reasons for hoping that oil and gas prices recede in the wake of a peace deal, beyond the obvious humanitarian ones. Modern production techniques for fertiliser are energy- and hydrocarbon-intensive and natural gas is an important feedstock for nitrogen fertilisers for good measure, where a key end-product is urea. To further complicate matters, a third of the world’s urea travels through the Straits of Hormuz, thanks to major production facilities in Saudi Arabia and Qatar.

Under these circumstances it is no surprise to see the price of urea shooting higher. At the time of writing, it trades near $700 a ton for only the fourth time across a dataset that goes back to 2009, and the potential impact upon food prices, the wider commodities asset class and inflation are potentially substantial.

Source: LSEG Refinitiv data

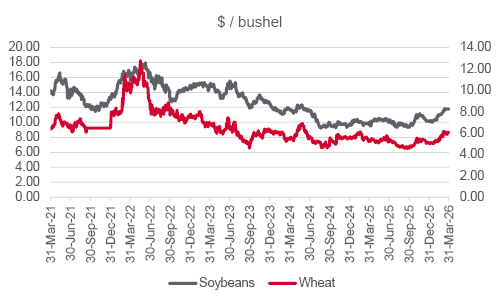

In some ways the spike in urea and fertiliser prices, and possible disruptions to supply, could hardly come at a worse time for farmers in the northern hemisphere, as they prepare for spring planting season. Agricultural crop prices are already responding. Wheat is up by a fifth and soybeans by a sixth this year, while corn prices are up by a fifth from the multi-year lows reached last summer.

Source: LSEG Refinitiv data

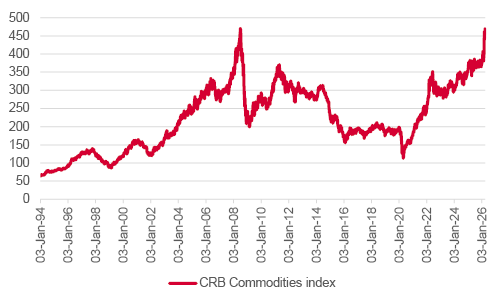

Soybeans, corn, and wheat are three of the ten agricultural – or ‘soft’ – commodities that comprise the CRB Commodities Index. The others are live cattle, sugar, cotton, cocoa, coffee, lean hogs and orange juice, and the ten between them make up 41% of the benchmark.

Given the price gains just mentioned, the strength in energy prices (a further 37% of the index) and last year’s ripping runs in gold and silver (7%), it is easy to see why the CRB Commodities index is moving back toward its all-time high, reached all the way back in 2008.

Source: LSEG Refinitiv data

But this is not an overnight development, even if precious metals wrote a lot of headlines last year and oil and gas have done the same so far in 2026.

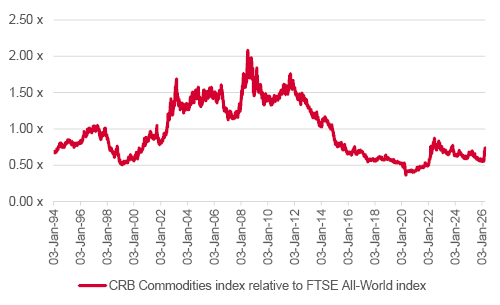

The CRB Commodities index is up by 139% this decade, a gain that outpaces the FTSE All-World’s capital return of 70% and its total return, including dividend reinvestment, of 93%.

Source: LSEG Refinitiv data

This is suggestive of a wider change in the macroeconomic and wider market environment. The post-Financial Crisis era of 2009-2021 was characterised by low growth, low inflation and low (if not zero) interest rates, and as a result, long-duration assets and those capable of generating secular growth, notably technology stock, or reliable yield became highly prized and performed accordingly well.

The picture looks different now, given how inflation, interest rates and nominal growth are higher, or are at least more volatile. In this respect, it makes little sense to expect what did well and has become expensive in the past decade to do well in this one, unless we quickly return to the low growth, low interest rate, low inflation murk of the 2010s.

Dollar weakness, the lack of capital expenditure on new supply and the importance placed upon supply chains and sourcing of raw materials as a matter of national security by both COVID-19 and wars in Eastern Europe and the Middle East are also factors that may raise the profile of commodities.

Only time will tell, but in this context, it may be worth considering the words of former Merrill Lynch (now Bank of America) strategist Bob Farrell, quoted in a recent edition of Marc Faber’s Gloom, Boom, Doom monthly market commentary:

“Change of a long-term trend is usually gradual enough that it is obscured by the noise caused by short-term volatility. By the time secular trends are even acknowledged by the majority they are generally obvious and mature,” wrote Farrell. “In the early stages of a new secular paradigm, therefore, most are conditioned to hear only the short-term noise they have been conditioned to respond to by the prior existing condition. Moreover, in a shift of long-term significance, the markets will be adapting to a new set of rules while most market participants will be still playing by the old rules.”

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.