2025 delivered gains across equities, bonds and commodities despite global volatility — and there are reasons for cautious optimism in 2026.

Tariffs, wars, AI job fears, rising debts and bubble concerns made the backdrop look tough, yet markets ended the year positively. Hopes for rate cuts, cooling inflation and steady growth support optimism for the year ahead.

Still, late-year crypto turmoil and surging gold and silver may signal more volatility. It’s worth reviewing 2025’s drivers and whether five key trends can continue.

2025 provided positive returns across a range of asset classes

Source: LSEG Refinitiv data. *2025 to close on 1 December

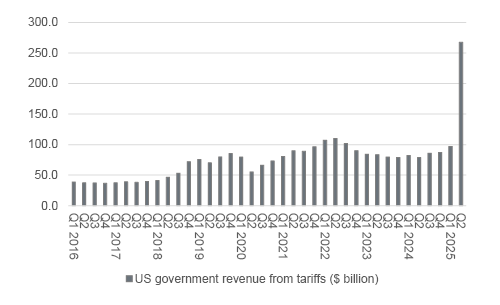

By November, the effective tariff rate was 17.3% - the highest since 1934, according to Yale Budget Lab.

Although tariffs only fully applied in summer and later fell through country-specific deals, government revenue surged. Trump even suggested they could fund $2,000 tax cuts, while the Supreme Court debated whether tariffs imposed under the International Emergency Economic Powers Act are legal. Repealing them could cut the overall tariff burden by about eight percentage points.

If that court case fails to knock down the IEEPA tariffs, it’s still unclear what tariffs may mean for trade, corporate profits and prices in 2026, but markets seem convinced the worst is over.

Any unexpected slowdown in growth, margin pressure or stickiness in inflation could therefore be a nasty surprise.

US tax revenue from tariffs has surged

Source: FRED – St. Louis Federal Reserve database

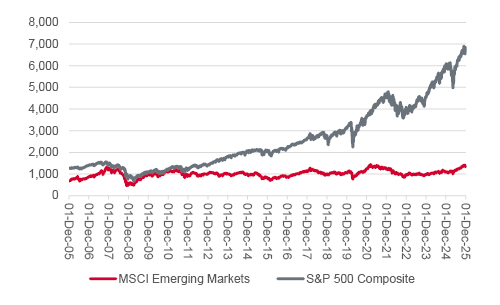

The best individually-performing stock markets to date in 2025 are South Korea, Greece, South Africa, Poland and Chile. That would be a nap hand for emerging markets, had Greece not recaptured developed market status in September.

Nearly two decades’ worth of relative underperformance means emerging markets, in general, offer more tempting valuations than those available in the all-conquering USA.

They also, in many cases, acted more quickly to quell inflation at the turn of the decade and thus have more scope for monetary stimulus in the form of interest rate cuts. Prolonged dollar weakness would be a further bonus, as a soft greenback would lessen the burden of dollar-denominated debt held by emerging nations.

Emerging markets have a long way to go to erase two decades of lagging returns

Source: LSEG Refinitiv data

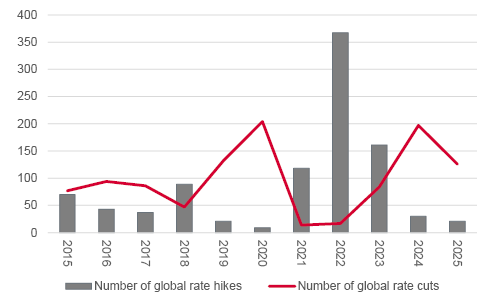

After a fallow 2024, the fixed-income asset class came back into fashion in 2025 as investors reacted to interest rate cuts from central banks and priced in further monetary easing in 2026 for good measure.

Further rate cuts could help in 2026, but sticky inflation would pressure sovereign, investment-grade and corporate debt. A growth shock could also leave high-yield spreads uncomfortably thin. Bond vigilantes remain wary of rising government borrowing in the West, though expectations of a return to zero rates and QE in any downturn may ease those concerns.

Global monetary policy remains tilted towards easing, not tightening

Source: www.cbrates.com

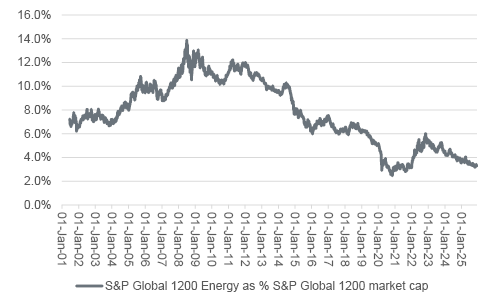

Oil prices slid despite wars, sanctions and steady demand. Brent peaked just above $80 in January before falling, pressured by OPEC+ output, Trump’s push for cheaper oil and the global drive toward net zero.

Energy stocks suffered: the S&P Global 1200 Energy sector now makes up just 3.3% of the index - near 2020’s COVID low and far below the long-term 7.7% average.

Tight spending by oil majors means supply growth is slow. If demand beats forecasts, prices could rebound - especially if inflation or rising Western debt push investors toward hard assets. Renewables and peace deals could also reshape the outlook.

Weak oil prices are helping with inflation

Source: LSEG Refinitiv data

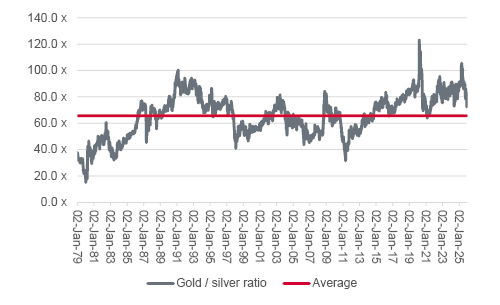

Gold and silver are both into their third bull markets since President Richard M. Nixon withdrew America from the gold standard and ended the Bretton Woods monetary system in summer 1971.

Silver’s late-year surge has closed up the gold: silver ratio to 75, from a figure above 100 earlier in 2025, but that is still above the modern-day average of 66. In this respect, precious metal fans may be inclined to believe that the so-called devil’s metal is cheap, relative to gold.

“Interest in both could cool if equity markets’ dream scenario of cooler inflation, steady economic growth and lower interest rates pans out as hoped and central banks prove they are on top of the situation.”

Equally, any diversion from that path, and any sense that central banks are not fully in control, or that they may chance their arm with inflation as they keep interest rates low to try and help governments manage their debts and interest bills, could yet give silver and gold a further boost.

Gold and silver came into their own in 2025

Source: LSEG Refinitiv data

Our Managed Portfolio Service offers ready-made portfolios designed to help advisers deliver strong outcomes for clients - without the complexity of building from scratch.

Each portfolio is actively managed by our investments team, with a clear focus on risk, cost and long-term performance. Explore the full range and see how they could fit into your client strategies

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.