The markets’ core scenario remains one of cooling inflation, steady economic growth and falling interest rates in 2026. Faith in central banks’ ability, and willingness, to ride to the rescue in the event of any unforeseen events, such as a recession or bout of wider market volatility, remains undimmed.

Central banks could remain centre stage in the coming year, but that is just one of five themes which, in particular, could have a major say how portfolios perform in 2026 (and beyond).

“Bulls dismiss talk of an AI bubble, by pointing to the transformational potential of the technology and its scope for providing the productivity and efficiency gains that global growth craves and can benefit corporate profit margins. The absence of huge stock sales by insiders is seen as an article of their faith in both the future and the valuations of their companies.”

Bulls dismiss talk of an AI bubble, by pointing to the transformational potential of the technology and its scope for providing the productivity and efficiency gains that global growth craves and can benefit corporate profit margins. The absence of huge stock sales by insiders is seen as an article of their faith in both the future and the valuations of their companies.

Sceptics will argue the whole thing is a house of cards, as semiconductor, server and cloud services, power and water providers rely on Sam Altman and OpenAI to meet $1.4 trillion of investment commitments, with money it does not have and products and services it is yet to fully develop. The increased use of debt, or complex financing agreements, brings uncomfortable echoes of the later stages of the technology, media and telecoms bubble of 1998 to 2000.

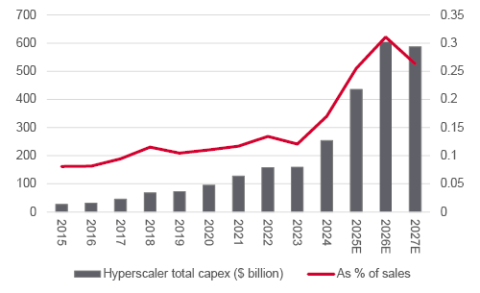

Thus far, AI hyperscalers have been rewarded by equity markets for spending. Trends in capital expenditure at the Big Five of Amazon, Alphabet, Meta, Microsoft and Oracle could be telling in 2026, especially as their spending means these previously asset-light businesses are now taking on more fixed assets than ever before, and also encroaching upon each other’s patch in earnest for the first time.

Source: Company accounts, Marketscreener, analysts’ consensus forecasts. *Alphabet, Amazon.com, Meta Platforms, Microsoft and Oracle

“Richard Bookstaber, in his magisterial book A Demon of Own Design, argues that any financial bull run initially flourishes but finally founders thanks to the trio of leverage, complexity and opacity.”

Richard Bookstaber, in his magisterial book A Demon of Own Design, argues that any financial bull run initially flourishes but finally founders thanks to the trio of leverage, complexity and opacity. It can be argued that private credit and private equity offer all three, a view supported by the arcane corporate structure at First Brands, one of two high-profile bankruptcies in the USA, along with Tricolor, which had private financing.

On the face of it, markets seem concerned, judging by how the S&P Listed Private Equity index and the share price of leading private credit investor Ares Management both peaked nearly a year ago. Both are trying to rally as 2025 ends and whether confidence recovers or ebbs further could be a useful lead indicator for 2026.

Source: LSEG Refinitiv data

“The dollar is the globe’s reserve currency but the Japanese yen’s role in global financial markets could yet prove more important than many realise.”

The dollar is the globe’s reserve currency but the Japanese yen’s role in global financial markets could yet prove more important than many realise.

Major market players have therefore shorted it, borrowed against it and used those cheap yen money to go buy risk assets around the globe. The crunch may come if the Bank of Japan and Governor Kazuo Ueda raise rates more quickly than thought, to contain inflation and fend off bond vigilantes, who are becoming twitchy about how yen weakness could lead to imported inflation, the BoJ’s swollen balance sheet and Tokyo’s sovereign debts.

Rate hikes could attract capital to Japan and reverse the yen’s decline. That could force shorters of the yen to unwind their carry trade, as losses force closure of their positions, and the sale of the assets they have bought around the globe, in a potential example of the tightly inter-linked nature of global financial markets.

Source: Bank of Japan, FRED – St. Louis Federal Reserve database, LSEG Refinitiv data

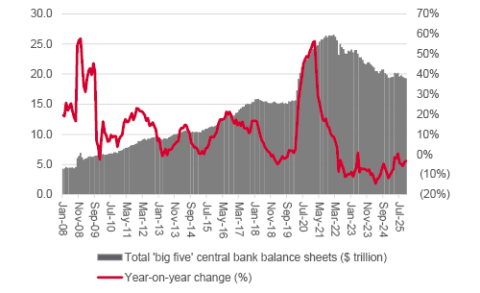

“Financial markets are expecting more interest rate cuts in the coming year, following the 130 seen so far in 2025.”

Financial markets are expecting more interest rate cuts in the coming year, following the 130 seen so far in 2025. US market-watchers are already publicly debating whether the Federal Reserve will embark upon a fresh expansion of its balance sheet in 2026, to provide liquidity at a time when ructions in private debt appear to be draining away some confidence, and cash.

Whether this is QE or not QE may be a question for another day. Such fine distinctions may be lost upon supporters of gold and silver, and other ‘hard’ assets, who have long been expecting central banks to not only scrap plans to shrink their balance sheets back to pre-crisis levels, but to turn on the taps once more. This debasement trade has done much to boost precious metal prices in 2025 and forms the investment case for them in 2026.

Source: Bank of England, Bank of Japan, European Central Bank, Swiss National Bank, US Federal Reserve and FRED – St. Louis Federal Reserve database

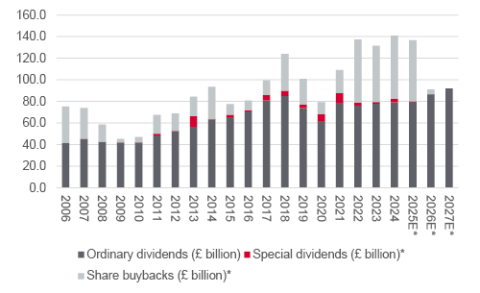

“The UK still attracts more brickbats than anything else, but the FTSE 100 is doing better than the NASDAQ and S&P 500 in sterling terms in 2025, thanks in part to how it is lining advisers’ and clients’ pockets with cash.”

The UK still attracts more brickbats than anything else, but the FTSE 100 is doing better than the NASDAQ and S&P 500 in sterling terms in 2025, thanks in part to how it is lining advisers’ and clients’ pockets with cash.

According to analysts’ consensus forecasts and company announcements, the FTSE 100 looks set to pay out some £80 billion in ordinary and special dividends in 2025, with a further £57 billion in buybacks on top. Buybacks and dividends from the rest of the market, plus another £30 billion or so from takeovers make for a total cash return from the UK market of £182 billion, or some 6.5% of the FTSE All-Share’s stock market capitalisation. That ‘cash yield’ beats the Bank of England base rate, the yield on the benchmark ten-year gilt and the prevailing rate of inflation.

There is no guarantee of a repeat in 2026, but analysts are forecasting an increase in dividend payments for 2026 and some £7 billion in buybacks are already planned by FTSE 100 constituents, so we shall see.

Source: Company accounts, Marketscreener, analysts' consensus forecasts. *As announced up to 12 December 2025.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.