It is ingrained in advisers and clients that the best way to get superior, risk-adjusted, long-term returns is to go against the crowd and seek out value. Such an approach has always needed courage and patience and 2024 has proved to be a particularly fierce test of this discipline for the pure and simple reason that what worked last year worked well again this year and it did so because the consensus macroeconomic view played out exactly as expected – inflation cooled, there was no deep economic downturn (or even a downturn of any real kind) and interest rates started to fall.

In sum, equities did well (again), led by technology and AI-related names (again), with the result that the US stock market outperformed, spearheaded by the NASDAQ (again), while Japan’s benchmark indices did better than those of Europe, which in turn generally did better than those of the UK, while emerging markets lagged (even as China put on a bit of a wiggle towards the end of the year). Holders of benchmark, ten-year government bonds lost money for the third year in four on both sides of the Atlantic, while commodity prices rose, on average, for the fourth time in five. Oil did poorly, gold did well, and bitcoin went bananas (again).

“These trends leave 2021-22 looking like a post-Covid-19 aberration and suggest the long-term trend of cheap energy, food, goods, labour and (above all) money that began in the early 1980s is reasserting itself. It is therefore worth thinking about what happened in 2024 and why, and whether these trends can continue in 2025 and beyond.”

These trends leave 2021-22 looking like a post-Covid-19 aberration and suggest the long-term trend of cheap energy, food, goods, labour and (above all) money that began in the early 1980s is reasserting itself. It is therefore worth thinking about what happened in 2024 and why, and whether these trends can continue in 2025 and beyond.

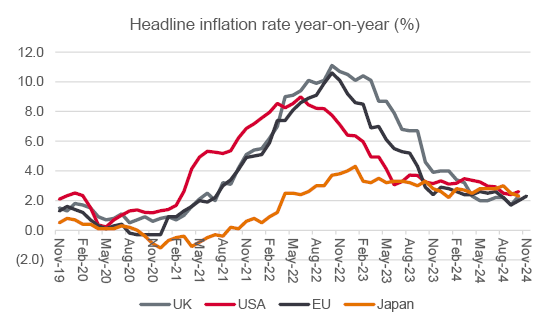

Inflation dipped back to, and even briefly below, central banks’ 2% target in the UK and EU and nearly got there in the USA, based on the official consumer price index and the US Federal Reserve’s preferred personal consumption expenditure benchmark. That gave central the room they sought to start cutting interest rates.

That said, much of the improvement in inflation came from oil and energy, as well as goods, where unblocked supply chains helped supply and the lagged effect of higher interest rates took some of the edge off demand. Services inflation remained sticky and that could yet prompt workers to demand more by way of pay increases, so perhaps central banks cannot be too gung-ho just yet.

Headline inflation rates cooled as hoped in 2024

Source: Office for National Statistics, US Bureau of Labor Statistics, European Central Bank. US and UK based on consumer price index, EU on Harmonised Index of Consumer Prices

“A global slowdown did not materialise in 2024, despite disappointing growth from China, Japan, Germany and France (four of the globe’s seven largest economies).”

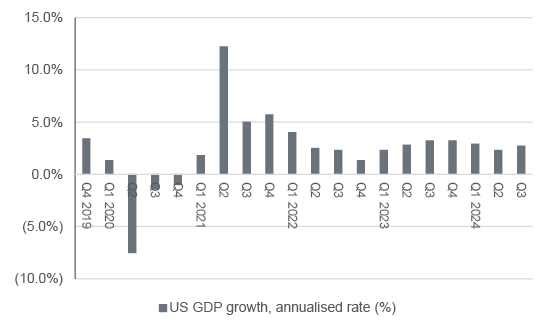

A global slowdown did not materialise in 2024, despite disappointing growth from China, Japan, Germany and France (four of the globe’s seven largest economies). India took up some of the slack, the UK emerged from 2023’s shallow downturn and the US once more led the charge. The Biden administration’s CHIPS and Inflation Reduction Acts buoyed output and American consumers kept spending, helped by rising house and stock prices. America’s latest debt ceiling breach gave no-one pause for any particular thought, even as the deficit soared, and President-Elect Trump’s plan to raise revenues through tariffs has provoked as much concern as it has positive comment. If Elon Musk succeeds in cutting US government spending, and Trump rolls back the Inflation Reduction Act, there could yet be some (unpleasant) unintended consequences.

USA powered global growth in 2024

Source: FRED – St. Louis Federal Reserve database

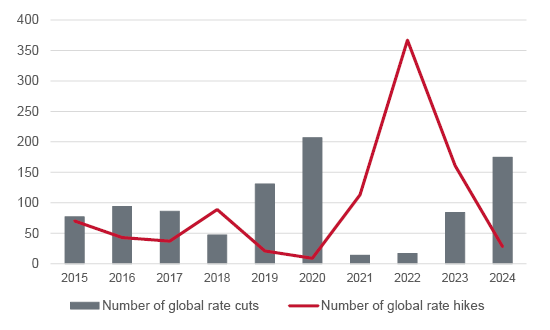

“A tally of 175 interest rate cuts worldwide in 2024, compared to just 28 rate hikes, tells a clear story.”

A tally of 175 interest rate cuts worldwide in 2024, compared to just 28 rate hikes, tells a clear story. The UK, Japan and China all added fiscal stimulus to fresh monetary impetus, and you could argue the USA did as well, given how the Federal deficit grew by another $1.8 trillion to an all-time high of $36 trillion. The question for 2025 is whether a combination of sticky inflation, steady growth and ballooning government debts (and thus rising sovereign bond yields) crimp central banks’ room for manoeuvre and force the pace of rate cuts to slow or, in a worst case, come to a halt.

Interest rate cuts gained momentum in 2024

Source: www.cbrates.com

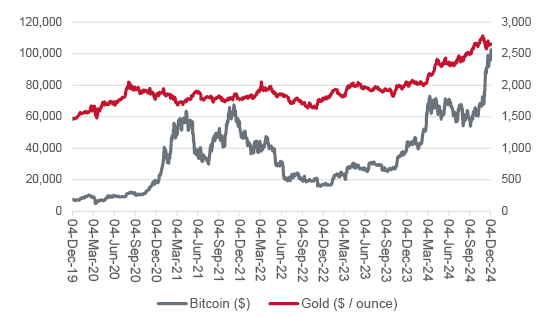

Silver hit a twelve-year high and gold and (most spectacularly) bitcoin set new all-time highs. Such demand for havens does not sit comfortably besides equities’ core scenario of cooling inflation, steady growth and lower interest rates. It may be the result of fears that central banks are playing fast and loose with inflation, or that ever-growing sovereign debts are persuading them to cut rates (and ease governments’ interest bills) whether they feel it is appropriate or not. President-Elect Trump’s enthusiasm for all things crypto, his planned deregulation drive and the departure of Gary Gensler from the Securities and Exchange Commission mean bitcoin is up 40% in barely two months, helped by what can be seen as increasingly reflexive ETF flows (the higher bitcoin goes, the more buyers appear), in a clear win for momentum over value investors.

Bitcoin has headed up, up and away

Source: LSEG Refinitiv data

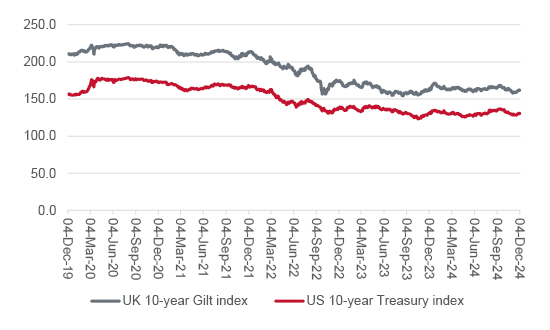

“Yields on ten-year paper rose (and prices fell) despite interest rate cuts, to suggest that bond vigilantes are becoming nervous about governments’ debt piles in the US, UK and EU and whether there is political or public appetite for the tax increases and spending cuts needed to fix them, in the absence of growth or inflation reducing those growing debt-to-GDP and interest bill-to-total spending ratios.”

Another slightly discordant note comes from the sovereign bond market, and this matters because the ten-year bond represents the local risk-free rate and thus the benchmark minimum return from any investment that is acceptable. Yields on ten-year paper rose (and prices fell) despite interest rate cuts, to suggest that bond vigilantes are becoming nervous about governments’ debt piles in the US, UK and EU and whether there is political or public appetite for the tax increases and spending cuts needed to fix them, in the absence of growth or inflation reducing those growing debt-to-GDP and interest bill-to-total spending ratios. Anyone who bought ten-year bonds in 2020, when central banks were indiscriminate buyers thanks to Covid-fighting QE schemes, has suffered, to perhaps offer a reminder that valuation always matters – in the end.

Sovereign bond yields rose (and prices fell) in 2024

Source: LSEG Refinitiv data

In two weeks’ time, we shall look at what the key macroeconomic trends may be in 2025 and how they in turn could shape the performance of advisers’ and clients’ portfolios.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.