Legendary American broadcaster Edward R. Murrow is known for many pungent epithets, but one of this column’s favourites is, “Anyone who isn’t confused really doesn’t understand the situation.” And right now, investors are entitled to feel confused because stock, bond, currency and commodity markets are giving out different signals. They cannot all be right.

“Equities seem to be pricing in a return to the ‘Goldilocks’ economy of the 2010s, where low inflation, low growth and low interest rates prevailed.”

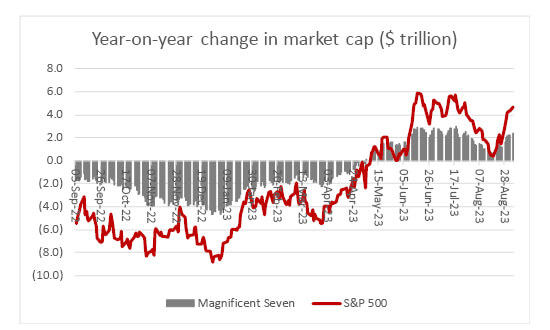

Seven big tech stocks have fired US equities higher in 2023

Source: Refinitiv data

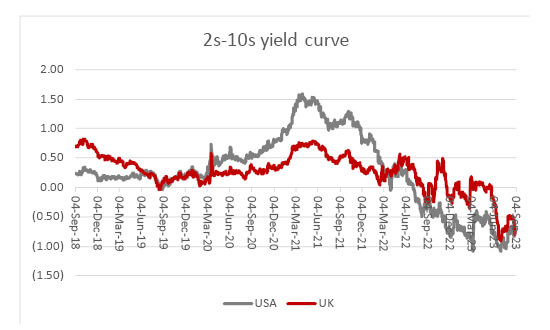

“Fixed-income markets remain convinced a recession is coming.”

Yield curves are warning of a recession

Source: Refinitiv data

A ‘Goldilocks’ scenario, an inflationary boom, a deflationary slump or a stagflationary quagmire all remain possible outcomes and not even central bankers know what is coming next, given how the US Federal Reserve, European Central Bank and the Bank of England are approaching every interest rate decision, while the Bank of Japan continues to do nothing at all.

“The really hard part is that each scenario potentially requires a different portfolio solution and asset allocation strategy, at least if history is any guide.”

The really hard part is that each scenario potentially requires a different portfolio solution and asset allocation strategy, at least if history is any guide.

The ‘Goldilocks’ scenario just feels too easy and too simplistic, especially after fifteen years of unorthodox, ultra-loose monetary policy and then the post-2020 explosion of fiscal stimulus. Equities may like it, but this column is not convinced, although this does make life much simpler for portfolio builders, because it is It is easy to make a case for any one of the other three scenarios:

If forced to guess, this column would sit in the inflation (or stagflation) camp and if a forty-year period of cheap money, cheap labour, cheap energy and cheap goods is coming to an end, then it may not be sensible to expect what worked in that period (long-duration assets like tech and Government bonds) to keep working. If the mood music changes, then value, small-caps and raw materials (and other things that central banks cannot print) may be the way forward.

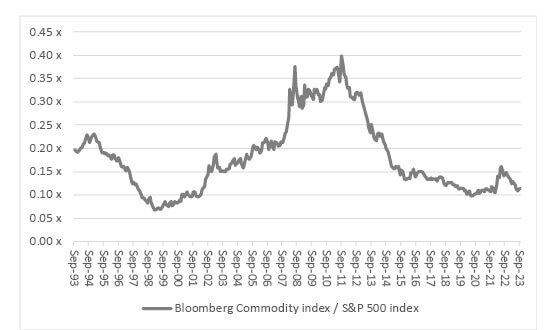

Is equities’ ten-year outperformance of commodities ending?

Source: Refinitiv data

“Equities massively outperformed in the 1990s, commodities led in the 2000s and then equities stormed back in the 2010s. The chart suggests the tide may be about to turn again.”

This column’s crystal ball is no better than anyone else’s but, in search of guidance, it will continue to look at one chart in particular. This is the relative performance of the S&P 500 against the Bloomberg Commodities Index. Equities massively outperformed in the 1990s, commodities led in the 2000s and then equities stormed back in the 2010s. The chart suggests the tide may be about to turn again. We shall see.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.