The Magnificent Seven may be one of the most famous films, or least most famous Westerns, ever made, but both the 1960 version (Yul Brynner, Steve McQueen and all) and the 2016 remake (with Denzel Washington and Chris Pratt, to name but two) draw heavily on 1954’s Seven Samurai and the work of legendary Japanese film director Akira Kurosawa.

But is not just in the world of cinema where the West can take inspiration, and learn, from Japan. What is happening in Japan’s financial markets right now could have implications for investors, not to mention central bankers and monetary policy, in London, Washington, Frankfurt and elsewhere, because the Bank of Japan (BoJ) is still locked in a titanic struggle with the Tokyo’s bond and currency markets.

“Unlike the US Federal Reserve, the European Central Bank and the Bank of England, the Bank of Japan is yet to raise interest rates and it is yet to officially try to sterilise Quantitative Easing and launch Quantitative Tightening, whereby its balance sheet would start to shrink.”

Unlike the US Federal Reserve, the European Central Bank and the Bank of England, the Bank of Japan is yet to raise interest rates and it is yet to officially try to sterilise Quantitative Easing and launch Quantitative Tightening, whereby its balance sheet would start to shrink.

Japan has yet to tighten monetary policy

Source: Bank of Japan, FRED – St. Louis Federal Reserve, Refinitiv data

The BoJ’s zero-interest-rate policy (ZIRP) dates back to 1999 and QE to 2001. Those dates should be a clue as to how hard Western central banks might find it to move away from them on a sustained basis, even if stock and bond markets right now appear to be pricing in a golden trifecta of a slowdown in inflation, a peak in interest rates and a soft landing for the global economy.

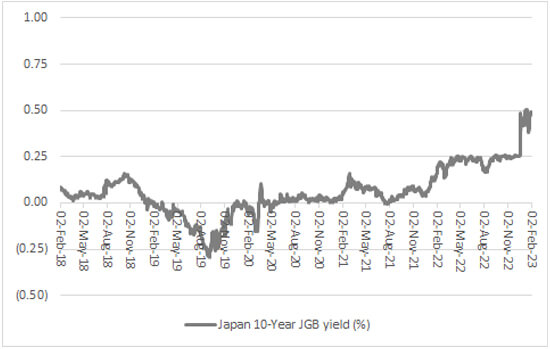

That would be nirvana indeed. But the BoJ has consistently found it hard, if not impossible, to tighten monetary policy for long and in 2016 it even launched QQE – Quantitative and Qualitative Easing – so it could bring in Yield Curve Control (YCC). Under YCC, the BoJ stated it would buy unlimited amounts of Japanese Government Bonds (JGBs) – and in effect print unlimited amounts of money – to hold the yield on the benchmark 10-year JGB below 0.25%.

After six years of that, even Japan began to see some inflation, and the sort of inflation for which Japan has strived after decades of near-deflation in the wake of the debt-fuelled equity and property bubble that finally popped as the 1980s ended and the 1990s began.

Japan is finally seeing some inflation

Source: Refinitiv data

“The yen began to tank and in late 2022 hit its lowest level against the dollar since 1998, just as the bond market began to rebel at the ongoing QQE and money printing.”

However, there was a cost. The yen began to tank and in late 2022 hit its lowest level against the dollar since 1998, just as the bond market began to rebel at the ongoing QQE and money printing.

The yen has sunk as QE has continued

Source: Refinitiv data

Something had to give and the BoJ blinked. It raised its cap on the 10-year JGB to 0.50% from 0.25% so it did not have to buy quite so many bonds and print so much money.

“The yen has rallied but the yield on the 10-year JGB flew out to 0.50% in the blink of an eye. Bond vigilantes continue to test the BoJ’s commitment to defending that new line in the sand.”

But that did not ease the pressure for long. Yes, the yen has rallied but the yield on the 10-year JGB flew out to 0.50% in the blink of an eye. Bond vigilantes continue to test the BoJ’s commitment to defending that new line in the sand.

Bond vigilantes are putting the BoJ to the test

Source: Refinitiv data

“The quandary of how best to manage the currency, the national debt, the BoJ’s balance sheet and its JGB holdings may well fall to his successor, especially as Kuroda continues to dismiss out of hand any scope for an exit from ZIRP or QE.”

The BoJ’s balance sheet already exceeds 100% of GDP so the vigilantes may not give BoJ Haruhiko Kuroda much rest, although he steps down at the end of his second, five-year term in early April. The quandary of how best to manage the currency, the national debt, the BoJ’s balance sheet and its JGB holdings may well fall to his successor, especially as Kuroda continues to dismiss out of hand any scope for an exit from ZIRP or QE, even if the fight to avoid deflation seems to be less of a worry.

Prime Minister Fumio Kishida will make the appointment and he will be aware of the economic and political stakes as policymakers look to keep bond and currency markets at bay, using any tools they have to hand.

Central bankers and PMs and presidents around the world will be watching and learning, too, and no doubt hoping the ending mirrors that of another cinematic classic from Kurosawa.

In Kagemusha, a castle siege is successfully fended off at the Battle of Nagashino with the help of new technology, in this case guns. The attackers are mown down in a hail of bullets. The shadow warrior protagonist, the kagemusha, is killed and his body eventually washed away down a river.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.