President Trump’s 1 August deadline for the imposition of ‘reciprocal tariffs’ on trading partners is now behind us. The White House can point to several trade deals, notably with the UK, Japan and EU, while negotiations continue with China, ahead of a deadline of 12 August. In the four cases mentioned, America will apply tariffs on imports at a lower rate than that threatened on ‘Liberation Day’ on 2 April and that is helping stock and bond markets, and the dollar, to rally from the spring lows, in the view that Trump will not follow through on the full tariff programme and spark a global tit-for-tat trade war that no-one is likely to win.

“The imposition of much higher levies on Brazil, Canada and Taiwan, to name but three, and threats of higher duties in pharmaceuticals, on the 1 August deadline day is prompting something of a market rethink, as this brings the worst-case scenario of 2 April back into view.”

The imposition of much higher levies on Brazil, Canada and Taiwan, to name but three, and threats of higher duties in pharmaceuticals, on the 1 August deadline day is prompting something of a market rethink, as this brings the worst-case scenario of 2 April back into view.

As discussed in this column last month, advisers and clients now have to decide whether:

Spring’s rally leaned on the first view. Any recurrence of fears about the third could lead to another shift in market mood.

Advisers and clients can perhaps track sentiment in three ways.

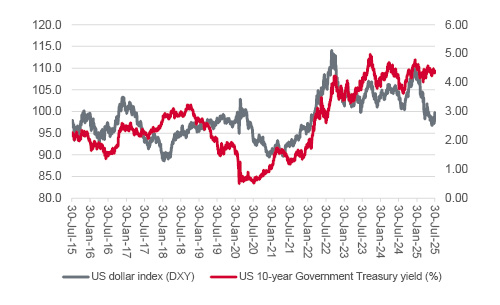

The dollar has rallied, and US Treasury yields have started to hold firm

Source: LSEG Refinitiv data.

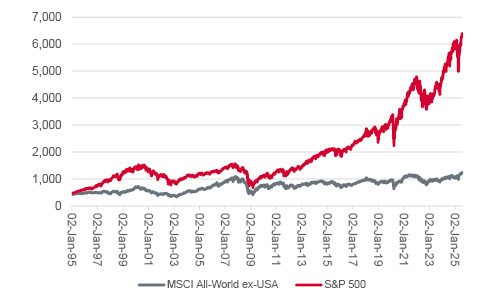

US equities have left the world trailing since 2009...

Source: LSEG Refinitiv data.

“The MSCI Emerging Markets index is making a run at its prior all-time high of 2021 and the MSCI World ex-US benchmark just might be looking to break out and reach new peaks all of its own. If both indices continue to run, then there really may be something afoot.”

This third trend need not be confined to EMs, either, if investors do decide to diversify away from the dollar and US assets more widely. The MSCI Emerging Markets index is making a run at its prior all-time high of 2021 and the MSCI World ex-US benchmark just might be looking to break out and reach new peaks all of its own. If both indices continue to run, then there really may be something afoot.

...but are non-US stock indices poised for a break-out?

Source: LSEG Refinitiv data.

Gains for those indices would not mean the US is about to collapse, just that it may be ready to underperform after a lengthy period of dominance. For the record, a classic emerging market like Turkey trades on around 11 times forward earnings for 2025, way less than the 25 times multiple applied to the S&P 500 right now, according to Standard & Poor’s research.

Granted, this is an intentionally provocative comparison, and it can be rebutted quickly, on the grounds that the biggest constituents of Istanbul’s BIST-100 are arms manufacturer Aselsan, Türkiye Garanti bank, holding company Koc, construction firm ENKA Insaat and airline Türk Hava Yollari. They are all fine companies, but the highest market capitalisation among them is $21 billion and none of them can necessarily be seen as secular growth plays, especially ones with a strong whiff of artificial intelligence, for all of the Turkish economy’s considerable long-term potential and the country’s strategic and geopolitical importance.

This is marked contrast to the US equity market where NVIDIA, Microsoft, Apple, Amazon.com, Alphabet and Meta Platforms are the six biggest stocks by market capitalisation. The other member of the Magnificent Seven, Tesla, ranks ninth.

The Magnificent Seven still dominate and drive US equities

Source: LSEG Refinitiv data.

“Between them, the Magnificent Seven represent 35% of the S&P 500’s $54 trillion stock market valuation, a smidgeon below the 36% peak reached in late 2024.”

Between them, the Magnificent Seven represent 35% of the S&P 500’s $54 trillion stock market valuation, a smidgeon below the 36% peak reached in late 2024. Again, any move away from them and rotation toward more cyclical names, for whatever reason, could signal, and play a role in, market sentiment toward US assets more widely, even if that seems hard to believe right now given the unabashed enthusiasm for AI-related narratives.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.