With the US Independence Day holiday of 4 July, it feels appropriate to revisit the US equity market, especially as the S&P 500 is now in a new bull market, at least if you use the definition of a 20% gain from the last major low. The American equity index bottomed at 3,577 and, at the time of writing, has subsequently advanced to 4,797, for a near-25% advance.

“Even a surge in the US Federal Funds rate from 0.25% to 5.25% is, so far, proving unable to stop American equities’ latest surge.”

The benchmark has achieved this despite rising bond yields, the latest debt ceiling drama and worries over a possible recession. Even a surge in the US Federal Funds rate from 0.25% to 5.25% is, so far, proving unable to stop American equities’ latest surge.

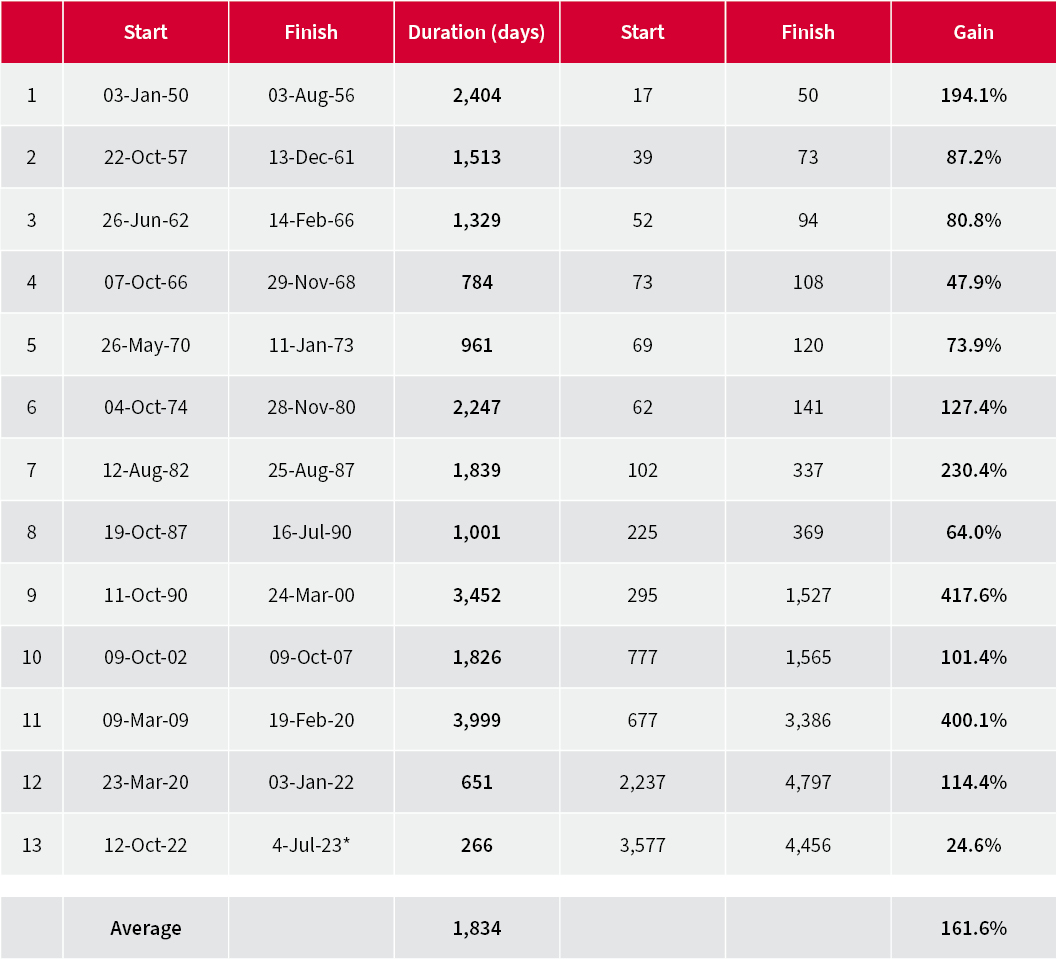

The S&P 500 is embarking upon its thirteenth ‘bull’ market since 1950

Source: Refinitiv data. *As of the time of writing, to date

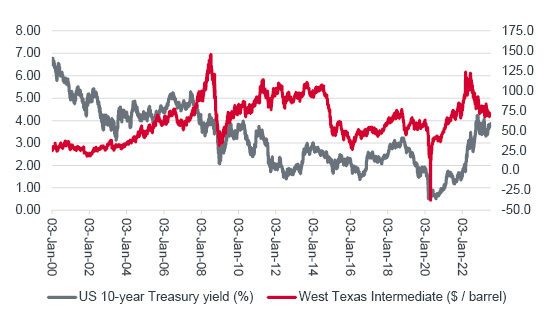

Easy on the eye as the chart for the S&P 500 may be – at least for those investors with a sizeable weighting toward US equities and for those hedge funds who are not short the index – there is another trend to which attention must be paid. That is the yield on the benchmark US 10-year Treasury, or government bond. It is fast-approaching the March high of 4.07% and while this column has no pretensions to, or qualifications for, being a chartist, or technical analyst, the wedge shape of falling highs and rising lows that is forming suggests the 10-year yield is about to break out, possibly in a violent way.

“A downward break [in the US ten-year yield] – because the Fed, the market, or both think inflation is under control – could be seen as a good thing for American stocks, not least as it would help to justify the prevailing ‘Goldilocks’ narrative.”

A downward break – because the Fed, the market, or both think inflation is under control – could be seen as a good thing for American stocks, not least as it would help to justify the prevailing ‘Goldilocks’ narrative. After spending most of 2022 pricing in a recession, US equities are returning to a favourite theme, namely that the American economy will continue to grow, but not so fast as to force severe interest rises or prevent inflation from gently receding.

US equities keep rising but the ten-year Treasury yield is on the march as well

Source: Refinitiv data

Whether the prospect of ‘no landing,’ rather than a ‘hard’ or ‘soft’ one, is credible is something that investors can only decide for themselves (even if such talk was prevalent in 1999 after a series of Fed rate hikes, only to ultimately prove inaccurate). It may be that the impact of the Inflation Reduction Act and Chips Act is still being felt in a construction and infrastructure boom that only starts to fade out in 2024, with the result that the US economy continues to defy the doubters.

One possible danger to this scenario is that the ten-year Treasury yields breaks out higher, as US growth does prove resilient, but so resilient that supply of labour, materials, goods and services struggles to meet demand, with the result that inflation stays above the Fed’s 2% target for some time to come.

“The trend in the ten-year Treasury is therefore one which advisers and clients should bear in mind, and it is one that will have implications for not just equities and bonds. Other asset classes will be watching closely as well, notably oil.”

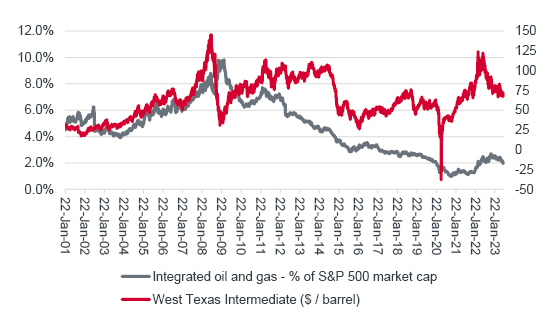

The trend in the ten-year Treasury is therefore one which advisers and clients should bear in mind, and it is one that will have implications for not just equities and bonds. Other asset classes will be watching closely as well, notably oil. While the past is no guarantee for the future, the price of crude seems to carry some correlation to the US ten-year Treasury yield. This makes sense in that oil can be a driver of inflation if prices rise and disinflation if the cost of a barrel declines, even if correlation does not necessarily mean causation.

The long-term relationship between oil and US ten-year yields is breaking down

Source: Refinitiv data

This is particularly interesting at the moment because there is an unusual degree of divergence between the price of West Texas Intermediate and the benchmark US Treasury yield. Oil is pricing in a recession it seems, Treasuries may be pricing in persistent inflation, and US equities look to be in ‘Goldilocks’ mode and looking at solid growth and cooling inflation.

They cannot all be right. US equities have done well, and oil stocks have not so perhaps if there is a surprise to come that may be the source. Although the dataset is not as long as would be ideal, since 2001 the S&P 500 Integrated Oil & Gas sector’s market capitalisation has averaged 4.6% of that index’s total price tag.

Investors are still shunning oil stocks in the USA

Source: Refinitiv data

“But if oil prices prove firmer than expected, and demand stronger than expected for longer than expected, oil stocks could yet confound the bears, even if investors who run strict environmental, social and governance (ESG) screens will be unmoved.”

Today that figure stands at just 2%. This may reflect the long-term plan to move toward greener, renewable alternatives and away from hydrocarbons, with all of the negative implications that has for demand for oil and gas, and also short-term demand worries. But if oil prices prove firmer than expected, and demand stronger than expected for longer than expected, oil stocks could yet confound the bears, even if investors who run strict environmental, social and governance (ESG) screens will be unmoved.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.