In 1970, Freda Payne’s Band of Gold topped the singles charts in the UK. While there are many interpretations of the lyrics, the Motown hit appears to reflect upon a marriage gone wrong, whereby the jilted bride is left with just thoughts of what might have been, (bad) memories and her wedding ring – the band of gold.

Anyone who held US dollars at that time may have been feeling similarly disenchanted in some ways, but relieved in others if they had held some gold of their own. Just a year later, in August 1971, America’s thirty-seventh President, Richard M. Nixon, took the greenback off the gold standard, ‘closing the window’ through which overseas governments could exchange paper dollars for the precious metal at a fixed rate of $35 an ounce.

That manoeuvre, which signalled the end of the 36-year-old Bretton Woods monetary system, enabled Nixon and the US to pay for welfare programmes and ultimately fruitless military action in Vietnam. Although economists and politicians hailed the policy as a liberation from a monetary straitjacket, investors can draw their own conclusions as to what markets ultimately thought of the launch of unfettered money creation by independent central banks.

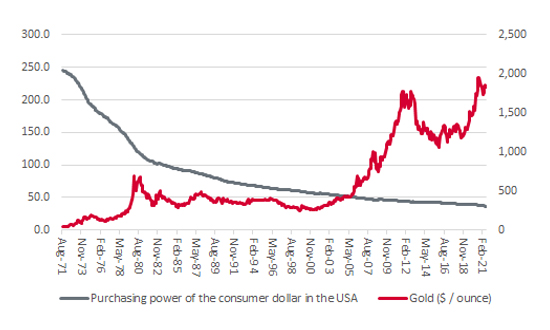

“Since Nixon’s closure of the gold window and demolition of Bretton Woods in summer 1971, the scores on the doors are clear: gold has gained 4,160% across the last five decades against the dollar. Put another way, the buck has lost 98% of its value relative to the precious metal.”

The scores on the doors are clear: gold has gained 4,160% across the last five decades against the dollar. Put another way, the buck has lost 98% of its value relative to the precious metal while 85% of its purchasing power has gone for good measure, thanks to an inexorable rise in the consumer price index (or inflation, in other words).

Gold has gained huge value relative to the dollar since 1971

Source: Refinitiv data, FRED – St. Louis Federal Reserve database

And so, exactly 50 years after the demolition of Bretton Woods, here we are again: a US Government that is running welfare programmes (and more besides, even allowing for the military withdrawal from Afghanistan) that it cannot afford and is running out of cash as it bumps up against the current Federal debt ceiling agreed by Congress of $28.4 trillion.

No wonder gold bugs are becoming more voluble.

“Even the most ardent supporters of the precious metal may have found it hard to celebrate the fiftieth (golden) anniversary with too much vigour. Gold suffered some vicious selling earlier this month, for reasons which have yet to become entirely clear.”

That said, even the most ardent supporters of the precious metal may have found it hard to celebrate the fiftieth (golden) anniversary with too much vigour. Gold suffered some vicious selling earlier this month, for reasons which have yet to become entirely clear.

Talk of a possible peak in the inflation rate in the US could be one explanation. Others pointed to what they felt was a co-ordinated hit by hedge funds in the futures markets while a gathering consensus among economists that the US Federal Reserve may be about to start tapering its quantitative easing (QE) programme could have also had an influence.

“Whatever the reason, though, the plunge did not last long, and gold has quickly recovered its ground. But for it to break fresh ground and motor beyond $2,000 an ounce on a sustainable basis for the first time, one of three things may need to happen (or even a combination of them).”

Whatever the reason, though, the plunge did not last long, and gold has quickly recovered its ground. But for it to break fresh ground and motor beyond $2,000 an ounce on a sustainable basis for the first time, one of three things may need to happen (or even a combination of them).

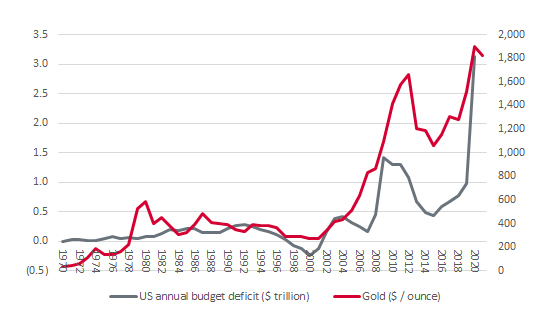

The trajectory of Government debt is one possible driver for gold…

Source: Refinitiv data, FRED – St. Louis Federal Reserve database

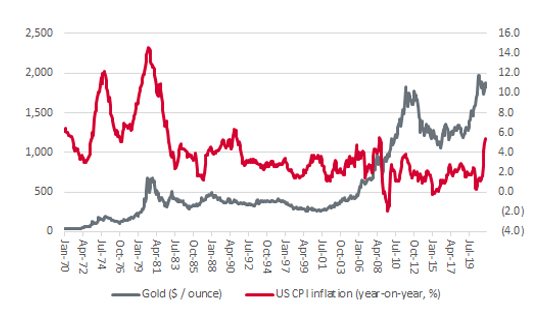

… inflation is another…

Source: Refinitiv data, FRED – St. Louis Federal Reserve database

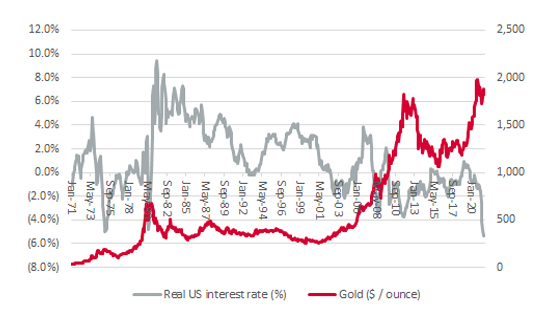

… while real interest rates could be the clincher, either way.

Source: Refinitiv data, FRED – St. Louis Federal Reserve database

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.