Interest rate cuts in the month of August in the UK, Sweden and New Zealand, to name but three, take the global total to 108 this year, according to the website www.cbrates.com. That is more than 2022 and 2023 combined, and the US Federal Reserve is now dropping very unsubtle hints that it will be joining in at the next meeting of the Federal Open Markets Committee on 18 September.

“This all seems to be in keeping with the core narrative that is doing so much to boost equity and Government bond markets alike, namely that inflation will cool, economies will enjoy a soft landing (if indeed there is any landing at all in the USA) and that central banks will therefore be able to cut the headline cost of money.”

Those rate cuts are in turn expected to stimulate demand for credit and thus economic activity, boost corporate earnings and cash flows thanks to higher demand (and lower interest bills) and persuade investors to take more risk, with asset classes such as equities, as the yield available from cash and fixed-income decline.

Such a scenario sounds very beguiling, but market history suggests that advisers and clients with substantial equity exposure might like to be a little careful about what they wish for with regard to monetary policy for three reasons, even if the FTSE All-Share and S&P 500 have, on average, benefited from cheaper money on a two-year view, once the initial rate cut has been announced:

Financial markets are pricing in a shallow rate cutting cycle, relative to historic averages

Source: Bank of England, US Federal Reserve, CME Fedwatch, LSEG Refinitiv data

The average rate cutting cycle is more than four percentage points

Source: LSEG Refinitiv data, Bank of England, US Federal Reserve. Covers period since 1962 in UK and post 1971 in USA.

“Faith in the US Federal Reserve’s ability (and willingness) to support stock markets dates back to when then-chair Alan Greenspan waded in with a pair of quick-fire interest rate cuts and a $3.6 billion bail-out plan in the wake of Russian debt default and the collapse of the Long-Term Capital Management hedge fund in 1998.”

Faith in the US Federal Reserve’s ability (and willingness) to support stock markets dates back to when then-chair Alan Greenspan waded in with a pair of quick-fire interest rate cuts and a $3.6 billion bail-out plan in the wake of Russian debt default and the collapse of the Long-Term Capital Management hedge fund in 1998. That set the scene for another leg-up in the 1990s US equity bull run. Since then, central bankers have responded with interest rate cuts, quantitative easing and other unconventional tools and interventions to the Great Financial Crisis of 2007-09, the European debt crisis of the 2010s, dislocations in the American inter-bank lending markets in 2019, the pandemic in 2020 and a US (and Swiss) banking wobble in 2023.

“Even former Reserve Bank of India governor Raghuram Rajan has opined recently in the Financial Times that central bankers should set a higher bar for interventions, so that their quest for financial and economic stability does not provide too big a safety net, encourage risk taking and promote the very instability they were seeking to avoid as a result.”

All of these actions helped financial markets, ultimately, to come through relatively unscathed, although sceptics may latch on to the words ‘ultimately’ and ‘relatively.’ Even former Reserve Bank of India governor Raghuram Rajan has opined recently in the Financial Times that central bankers should set a higher bar for interventions, so that their quest for financial and economic stability does not provide too big a safety net, encourage risk taking and promote the very instability they were seeking to avoid as a result.

Mr Rajan’s view is supported by arguments that interest rate cuts helped to stoke the tech, media and telecoms bubble in 1998-2000, in the wake of the LTCM bail-out, and that free and easy money has done much to inflate asset valuations since the introduction of Quantitative Easing (QE) and zero-interest-rate policies (ZIRP) as salves for the after-effects of the Great Financial Crisis of 2007-09. Moreover, it does seem as if recessions now happen less frequently, but come with greater severity when they do, while financial crises also feel more common.

To start with the UK, the good news is that over the thirteen rate-cut cycles since the inception of the FTSE All-Share in the early 1960s, the index has made an average gain of 16% in the two years after after the first decrease in borrowing costs. Yet the hit rate over the first three to six months is patchy and the 2001-03 and 2007-09 rate-cutting cycles started disastrously for buyers, with losses over a two-year period as recessions bit hard, earnings disappointed and equity valuations faltered.

How the FTSE All-Share has performed after the first Bank of England rate cut

“The two-year post-cut performance of the S&P 500 is similarly compelling, on average, but again the trick for advisers and clients is to safely navigate the volatility in between.”

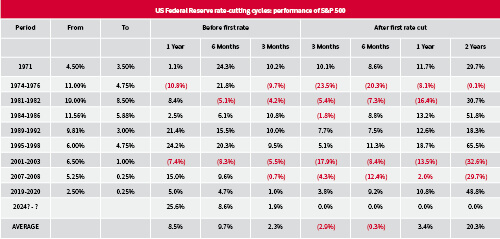

The two-year post-cut performance of the S&P 500 is similarly compelling, on average, but again the trick for advisers and clients is to safely navigate the volatility in between. The S&P 500 historically does not make much initial progress after the first cut, not least because it runs up strongly in anticipation of looser monetary policy.

How the S&P has performed after the first Fed rate cut

The scenario that markets are still discounting is lower inflation, a soft landing and a gentle reduction in rates. If any one of those three trends diverges from current expectations, then equity markets may move, potentially with some violence, as we saw briefly back in August.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.