Any readers who share Warren Buffett’s opinion that gold is an inert, useless lump can turn over the page right now. The Sage of Omaha has long since asserted that an alien invader would dismiss the purportedly precious metal as worthless were they to trip over an ingot upon their arrival from outer space. That might be going a bit far, as even the most hardened sceptic would probably be prepared to accept that gold could be worth what it costs to get it out of the ground – around $1,200 an ounce, based on the all-in sustained cost (AISC) at the world’s largest quoted gold miner, Newmont Corporation.

Gold bugs may be more interested, however, especially as gold is trying to forge and sustain a break above $2,000 an ounce and in the process reach new all-time highs. Moreover, Newmont’s decision to increase the value of its offer for fellow gold digger Newcrest Mining does catch the eye.

Whenever a major piece of M&A (merger and acquisition) activity is announced, the single most important items of information are the price paid and the valuation implied. This is because they can determine whether the buyers or potential sellers are getting the better part of the deal and also whether the shares of peers in the same industry or sector are looking cheap or not.

The gold mining industry has been busy in this respect. Barrick Gold swallowed up Randgold Resources and Newmont snapped up GoldCorp in 2019, while Agnico-Eagle and Kirkland Lake Gold merged in 2021 and Agnico-Eagle and Pan American Silver have just finished buying and divvying up Yamana Gold. Among the few remaining UK gold miners, Chaarat Gold took a look at Shanta Gold last autumn and although nothing came of that it did suggest that someone, somewhere thought there was value on offer.

Sceptics will dismiss this as an attempt to manufacture growth and momentum where little or none exists, since gold output grows only slowly and the AISC of producing gold is rising, in no small part due to surging energy and staff costs (trends which rather dent gold miners’ perceived status as a hedge against inflation).

“Gold bugs, however, will argue that the proposed Newmont-Newcrest deal is simply further evidence that gold company executives see value that the stock market is overlooking.”

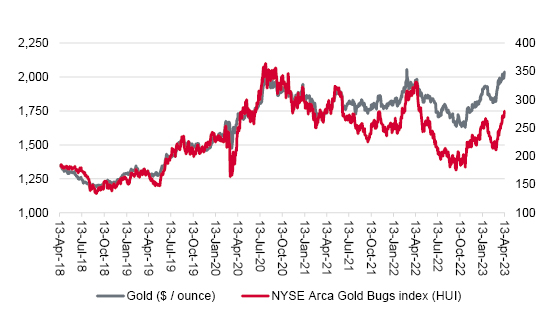

Gold bugs, however, will argue that the proposed Newmont-Newcrest deal is simply further evidence that gold company executives see value that the stock market is overlooking. The price of gold is up by 32% since the start of 2020 but the NYSE Arca Gold Bugs index, known as the HUI, is up by just 12% over the same period – and all of that gain (and more) from the index hails from the rally seen since 1 January this year.

Gold and gold miners are rallying

Source: Refinitiv data

“American gold miner Newmont is now getting busy again. It first bid for Australia’s Newcrest in February in an all-stock deal that valued the target at $17 billion. The would-be buyer has now increased its all-paper offer to $19.5 billion.”

American gold miner Newmont is now getting busy again. It first bid for Australia’s Newcrest in February in an all-stock deal that valued the target at $17 billion. The would-be buyer has now increased its all-paper offer to $19.5 billion.

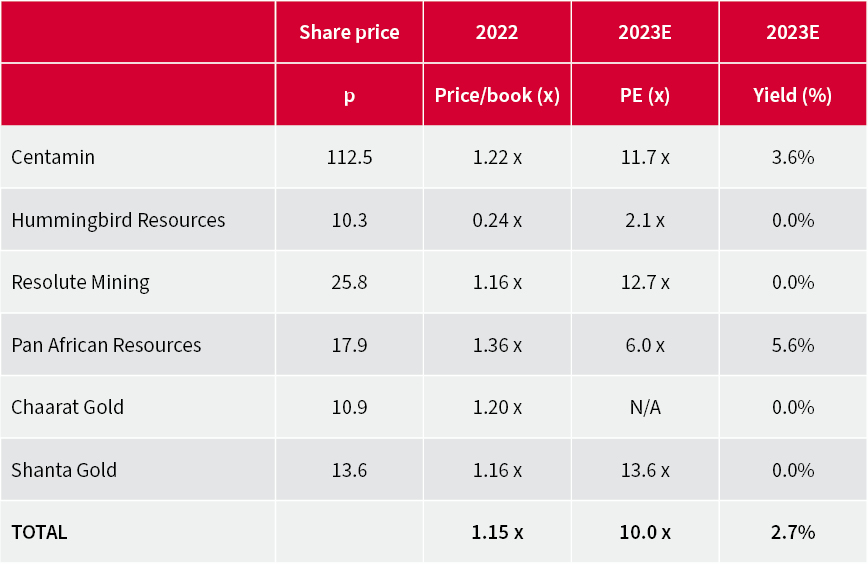

That price tag puts Newcrest on almost 1.7 times historic book, or net asset value. The major, US-listed producers trade on 1.5 times and London market’s gold diggers at 1.1 times.

Newmont bid implies 1.7x book value for Newcrest

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

UK gold diggers trade at discounts to US peers on an asset basis

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

Advisers and clients are unlikely to have the time or inclination to dig too far into such details. But in many cases, the US-listed miners and producers do look to offer greater scale (and lower all-in sustained production costs) than their UK-listed equivalents. The relative valuations do look to at least partly reflect that, and also the differing jurisdictions in which the miners operate. It is also possible to argue that junior miners can offer greater leverage into any upside in gold prices.

“Even though the prevailing rate of inflation is slowing, at least in the USA, gold is on the move all the same.”

Even though the prevailing rate of inflation is slowing, at least in the USA, gold is on the move all the same.

Perhaps oil’s fresh gains, in the wake of OPEC’s unexpected production cut of early April, is stoking fears of a 1970s-style second wave of inflation (the first followed the 1973 Yom Kippur war and the second the deposition of the Shah of Iran in 1979, both of which caused crude prices to spike).

Perhaps gold is gearing up for interest rate cuts as wrecked government finances and bloated debts limit how far central banks can tighten policy without doing serious damage, either to the economy, financial markets or both. Perhaps it is no more than a flash in the pan, if you will pardon the expression, but it will be interesting to see if gold mining executives are ahead of the game and being shrewd with their latest round of consolidation or not.

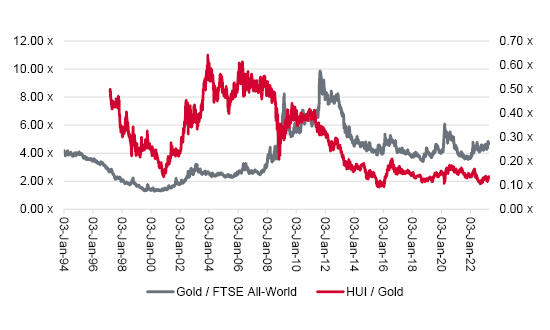

One thing is certain. Gold is trading toward the lower end of its range relative to global equities (as benchmarked by the FTSE All-World since its inception in 1994) and gold miners are trading at near-historic lows relative to the metal’s price (as benchmarked by the HUI and its inception in 1997).

Gold miners are trading near historic lows relative to gold

Source: Refinitiv data

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.