One of the most encouraging features of 2026, from an equity market point of view, remains positive earnings momentum. On both sides of the Atlantic, positive earnings surprises from companies continue to outweigh negative ones, and aggregate profit forecasts for the major indices continue to rise, not fall.

In an era where algorithm-driven funds dominate so much of the near-term trading flow, and passive funds create an ever-greater degree of reflexivity, thanks to the cycle of more buying – higher share prices – higher index weightings and then more buying and so on (and on), this matters more than ever.

It also means that any easing of that upgrade momentum or, worse, a reversal that is so abrupt it leads to downgrades, could have serious consequences. The algo-led funds would dispassionately respond with selling, and the passive funds could, presumably, be at risk of creating a reflexive self-feeding cycle that leans to the downside every bit as vigorously as it currently does to the upside.

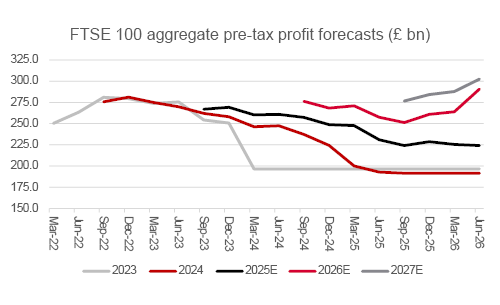

For all of the brickbats thrown at the FTSE 100, and the prevailing political and economic uncertainty, the good news for clients and advisers with exposure to UK equities on the earnings front is three-fold.

Source: Company accounts, Marketscreener, consensus analysts' forecasts

Source: Company accounts, Marketscreener, consensus analysts' forecasts

The net result is the FTSE 100 trades on barely 13 times forward earnings for 2026 and 12 times for 2027. These are not unduly low multiples relative to the index’s own history but nor are they expensive either, which may offer some downside support should anything unexpectedly go wrong.

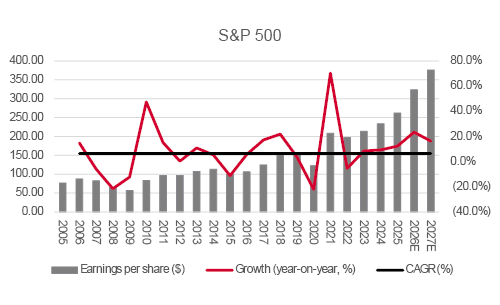

The outlook also looks bright in the USA, after a bumper first-quarter reporting season and upgrades galore for the second quarter at the same time.

Source: Company accounts, Marketscreener, consensus analysts' forecasts

However, there are two key differences between the UK and USA.

It may well be different this time, but the absence of any acceleration in American companies’ long-term earnings growth seems to back up the assertion of the American Nobel Laureate economist Robert Solow that, “You can see the computer age everywhere but in the productivity statistics.” Should the so-called Solow Paradox hold true, then the combination of lofty valuations and earnings disappointment could be a recipe for greater volatility in US equities, at the very least, even if such a scenario feels unlikely as we prepare for the second-quarter results season from mid-July onwards.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.