Winston Churchill was Chancellor of the Exchequer from 1924 to 1929, and he presented five Budgets to Parliament during his term in office. He targeted pension reform, and the protection of wages from inflation and growth above all else, in uncanny echoes of the current Chancellor’s programme. He also endured a torrid time thanks to the General Strike and his legacy was tarnished by the Bank of England’s decision with withdraw from the Gold Standard in 1931, just six years after Churchill oversaw the UK’s return to it. As a result, the future Prime Minister later noted “Everybody said that I was the worst Chancellor of the Exchequer that ever was. And now I’m inclined to agree with them. So now the world’s unanimous.”

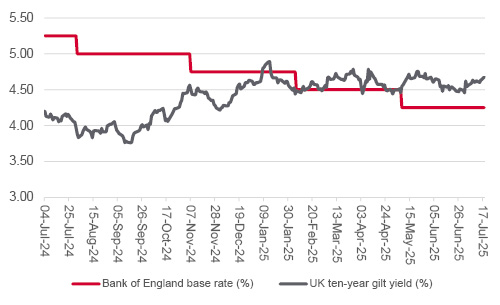

It is too early to judge whether Rachel Reeves can succeed in her own goals of stoking growth and meeting her own fiscal rules on Government borrowing, but the strain already seems to be telling, judging by her tearful appears in the House of Commons amid a backbench rebellion over welfare reforms. The UK Government bond market does not seem convinced, either, given how the yield on the benchmark ten-year gilt is higher than it was at the time of Labour’s General Election victory in July 2024, even though the Bank of England base rate is down by a full percentage point over the same period.

Bond vigilantes continue to stalk the Chancellor of the Exchequer

Source: LSEG Refinitiv data.

Advisers and clients will ultimately look to their portfolios to gauge the effect of Chancellor Reeves’ policies, and, in this respect, she is off to a decent start, despite President Trump’s tariffs, war in the Middle East and turgid UK economic growth figures. The Chancellor’s ‘Leeds Reforms’ package generally drew praise, albeit of the lukewarm variety, and the FTSE All-Share is up by nearly 9% since Labour took office last summer, a gain that has outpaced inflation.

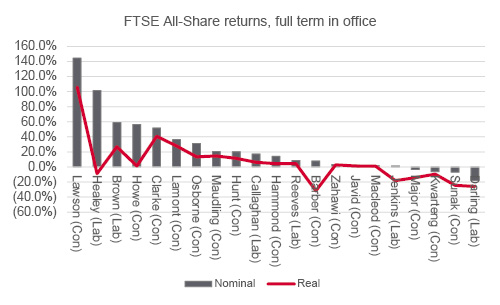

Rachel Reeves is the twenty-first Chancellor of the Exchequer since the inception of the FTSE All-Share index in 1962 and the sixth member of the Labour Party to hold the post during this period. She has already outlasted four of her predecessors, all of whom were Conservatives – the ill-fated Ian MacLeod, Kwasi Kwarteng, Nadhim Zahawi and Sajid Javid.

“Stability is always welcomed, and the Chancellor’s first year in office represents a steady one for equity investors, despite some signs of unrest in the bond market and on the backbenches.”

Stability is always welcomed, and the Chancellor’s first year in office represents a steady one for equity investors, despite some signs of unrest in the bond market and on the backbenches.

Chancellor Reeves’ first year was a steady one for UK equity investors

Source: LSEG Refinitiv data, www.gov.uk. *To 4 July. 8.7% in nominal terms and 4.3% in real terms as of 21 July and time of writing. ** Adjusted for RPI as CPI only introduced in 1989 in current format.

Cooler inflation is helping here, both in nominal and real terms, and the rate of change in prices could yet define Reeves’ term as Chancellor, especially if external events take a hand.

“The gap between nominal and real, inflation-adjusted returns from the FTSE All-Share index under some Chancellors is truly glaring, and this is company that the current incumbent of 11 Downing Street may not wish to keep.”

The gap between nominal and real, inflation-adjusted returns from the FTSE All-Share index under some Chancellors is truly glaring, and this is company that the current incumbent of 11 Downing Street may not wish to keep.

Inflation had a withering effect upon advisers’ and clients’ returns from the stock market under Denis Healey’s Labour Chancellorship in the mid-to-late 1970s, even if his supporters would argue his record was tarnished by the need to tackle the mess left behind by the crack-up Barber boom and oil price spike of the early seventies. Inflation also chewed up the nominal gains made by the FTSE All-Share under the Tory Chancellors Sir Geoffrey Howe (1979-83) and the aforementioned Tony Barber (1970-74).

Investors – and Chancellors – must always beware inflation

Source: Refinitiv data, www.gov.uk. Adjusts nominal return by change in the retail price index (RPI) as CPI data only goes back to January 1989 in current format.

Not all of the inflation that tore through the British economy in 1973-74 could be laid at the door of Mr Barber’s policies, as the 1973 oil price shock had a huge amount to do with it, and this highlights the importance of factors which are beyond the control of any Chancellor, no matter how diligent or skilled.

Alastair Darling could hardly have expected to inherit the Great Financial Crisis which prompted a deep recession and a wicked bear stock market. Norman Lamont inherited British membership of the Exchange Rate Mechanism, fought to defend the pound and a policy in which he did not believe and oversaw a devaluation of sterling which actually helped the FTSE All-Share to rally. Mr Sunak had to contend with COVID-19 and the worst recession for three centuries, so perhaps he got the worst hand of all.

Even so, advisers and clients, looking at the world through the narrow perspective of their portfolios, will be wanting Rachel Reeves to think back to Barber and Healey. The Chancellor’s desire for growth is totally understandable, especially as rapid nominal growth could help to shrink the debt-to-GDP ratio, if borrowing and base rates are kept under control.

“Failure to rein in spending could raise fears of fiscal profligacy and – in a worst case – a situation where suppressed interest rates and even money printing come into play as tools to make the aggregate debt manageable.”

But that is a big ‘if,’ should the backbench rebellion on welfare reforms be any sort of guide. Failure to rein in spending could raise fears of fiscal profligacy and – in a worst case – a situation where suppressed interest rates and even money printing come into play as tools to make the aggregate debt manageable. Further increases in ten-year gilt yield, and perhaps the gold price, may give advisers and clients a valuable steer as to the likelihood of such a scenario.

Past performance is not a guide to future performance and some investments need to be held for the long term.

Russ Mould assesses Rachel Reeves’ first year as Chancellor and what it could mean for markets and your clients.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.