The most violent price reaction to last month’s Budget was seen in the usually calmer environment of the bond market.

The yield on the benchmark 10-year Government bond, or Gilt, plunged in one trading session from 1.11% to 0.985%. That equated to a 1.3% one-day gain in the paper’s price (since bond yields move inversely to price, just as is the case with shares) as the Budget document itself revealed a big drop in the amount of Gilts that the Bank of England intended to sell for fiscal 2021–22, in response to downward revisions to estimates for Government borrowing.

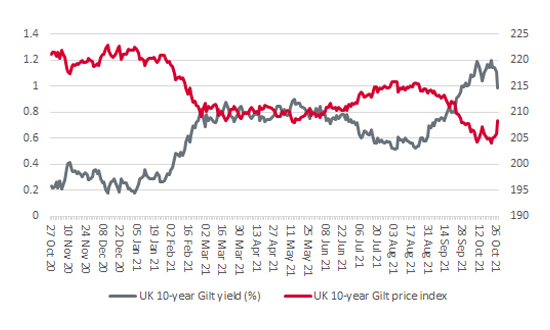

Budget prompted a rally in Gilts

Source: Refinitiv data

But that was the first bit of good news holders of UK Government debt had had for a while. As inflation has picked up pace, so bond yields have surged and prices tumbled. From its year low of 0.18% on 4 January, the benchmark 10-year Gilt yield rose to a peak of 1.20% on 21 October. That equated to an 8% drop in the price of the paper – so anyone who bought at the yield low (and price peak) lost the equivalent of 44.4 years’ worth of interest.

“The surge in 10-year Gilt yields, and accompanying drop in prices, raises the issue of whether UK Government bonds are indeed a ‘safe’ investment or not.”

This raises the issue of whether Government bonds are ‘safe’ or not. The idea is that they are. The adviser or client buys the bond at issue, receives the interest payments (or coupons) over the lifetime of the bond and then gets back their initial investment (or principal) upon maturity of the loan.

However, there are risks.

The coupon is always fixed and is based upon the issue price of the paper (usually 100). The yield will change according to the price, just as it would for a share.

As coupons get lower, or yields become thinner, the buffer against any potential capital loss in the event interest rates rise gets progressively smaller. This is where duration comes into play.

Note how that one percentage point rise in the UK 10-year Gilt yield between January and October translated into an 8% price decline.

“The issue, therefore, is not whether Government bonds are risky or not, but whether the rewards on offer, in the form of the coupon or the running yield, compensate the adviser or client for the risks involved.”

The issue, therefore, is not whether Government bonds are risky or not, but whether the rewards on offer, in the form of the coupon or the running yield, compensate the adviser or client for the risks involved.

If inflation becomes entrenched and stays elevated, the answer may well be ‘no’. If an investor believes the storm will blow over and deflationary forces will reassert themselves, then the answer may be ‘yes,’ especially after the recent sell-off.

Advisers and clients can also build a portfolio of bonds to help manage the risks.

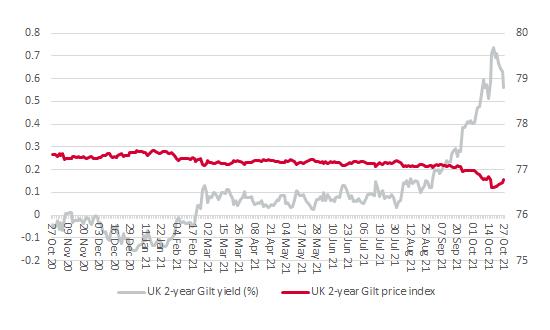

2-year Gilts have lost much less ground than the 10-year paper in 2021

Source: Refinitiv data

Advisers and clients also use a range of bond funds to mitigate the dangers. They can also select flexible bond funds that can put money to work across a wide range of fixed-income asset classes and not just one and therefore use its mandate to tackle – and even benefit from – duration.

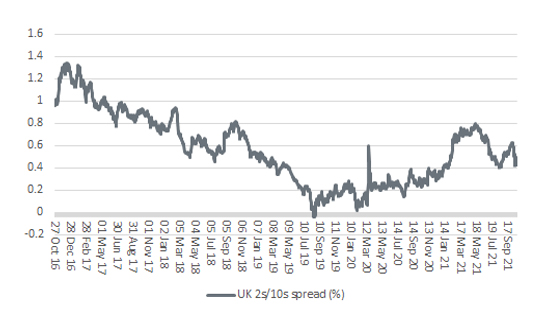

The UK 2/10s yield curve is flattening again

Source: Refinitiv data

“One tool that advisers and clients can use to measure whether inflation or deflation is coming is the yield curve. This can be measured in the differential between the yield on the 2- and 10-year Gilts.”

One tool that investors can use to measure whether inflation or deflation is coming is the spread between the 2- and 10-year Gilt. If the market thinks a recovery and inflation are coming (and that central banks will actually raise interest rates), the spread may widen, and the yield curve steepen, as rate rises are priced in. If it thinks a downturn or deflation are coming, then it may flatten as rate cuts are priced in.

Right now, the yield curve is flattening, even as inflation rises. Central bank manipulation of bond markets via quantitative easing could mean we are getting a false signal. But it could mean the Gilt market is warning of the middle ground, the worst outcome of all – stagflation.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.