It will be of little or no consolation to investors, but the UK is not the only country whose economic foundations are coming into question. The Bank of England has had to intervene in the gilt market, ostensibly to support the value of defined benefit pensions and more generally to bring order to the Government bond market, while China has stepped in to support its currency in the foreign exchange markets and so has Japan.

“Moves to return monetary policy to anything like ‘normal’ have barely started and currency and bond markets have already started to buckle.”

Moves to return monetary policy to anything like ‘normal’ have barely started and currency and bond markets have already started to buckle. This suggests that at some stage central banks will have to recant and return to cutting rates, relaunching QE or both, as the Bank of England is already doing, albeit under a different guise.

The UK does have specific issues of its own to address, not least as it has two particularly bad habits.

“The cavalier way in which the plan was presented, the manner in which the Bank of England is looking to tighten policy as the Government loosens it and the ongoing uncertainty as to what happens when this support package expires and oil and gas prices are still elevated, in effect combined to break the UK gilt market.”

These twin deficits leave the UK reliant upon others to fund those bad habits and this may be why the mini-Budget may represent an unlikely tipping point. Looking to push through £45 billion in (apparently) unfunded tax cuts does not look like a big deal when compared to a national debt that is already £2.4 trillion. Even the suggested £150 billion price tag for household and business energy subsidies looks small in that context. But the cavalier way in which the plan was presented, the manner in which the Bank of England is looking to tighten policy as the Government loosens it and the ongoing uncertainty as to what happens when this support package expires and oil and gas prices are still elevated, in effect combined to break the UK gilt market. Buyers of Government debt – in effect, lenders of money to the UK – decided they were getting far too little yield by way of compensation for the risks they were taking. That is why gilt yields shot higher and the Bank of England had to step in.

Three major policy interventions in a week does not feel like a good sign, especially as Japan is still keeping monetary policy ultra-loose, as it leaves its headline interest rate unchanged at minus 0.1%, while China is responsible for two of the 12 interest rate cuts logged worldwide by the website www.cbrates.com this year (compared to 271 rate hikes).

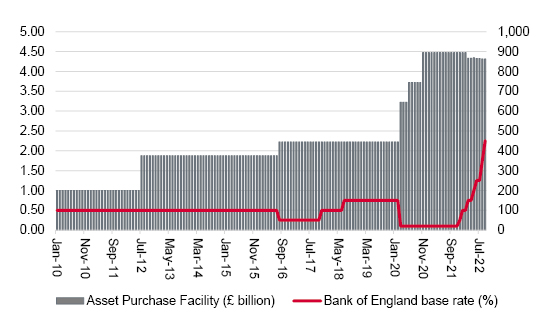

All three are struggling to juggle high debt with low rates and a firm currency. Something must give, and chaos is breaking out in the UK even when interest rates are 2.25% and the Bank of England can point to a mere £32 billion, or 3.5%, reduction in its £895 billion Quantitative Easing (QE) scheme.

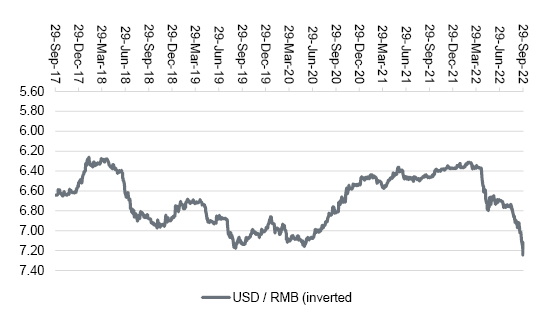

China is looking nervously at the falling value of the yuan…

Source: Refinitiv data

…as Japan intervenes to support the yen.

Source: Refinitiv data

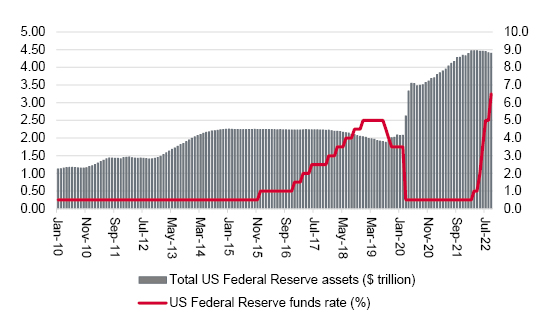

Most disconcertingly of all, the US Federal Reserve is only just embarking upon Quantitative Tightening and seems determined to press ahead with further interest rate rises of its own. The Fed Funds rate is only at 3.25% and the Fed’s total assets stand at $8.9 trillion, only a fraction down from their all-time high.

Bank of England has barely started with QT…

Source: Bank of England, Refinitiv data

…and so has the Fed, but markets are rocking anyway

Source: US Federal Reserve, FRED – St. Louis Federal Reserve database, Refinitiv data

Three nations are therefore failing, it seems, to maintain lofty debts alongside low borrowing costs and a firm currency.

Eighteenth-century economist Adam Smith would not be surprised. In The Wealth of Nations Smith wrote, 'History shows that once an enormous debt has been incurred by a nation, there are only two ways to solve it: one is to simply declare bankruptcy and repudiate the debt. The other is to inflate the currency and thus to destroy the wealth of the ordinary citizen.'

You can argue that neglects both a third option, which is to get the economy growing so the debt can be paid back (and Liz Truss and Kwasi Kwarteng will argue this is their plan), and a fourth, which is to start a war, but regrettably Smith looks to be spot on.

At one end of the spectrum, Suriname, Sri Lanka and Lebanon have already defaulted. Zambia, Ghana and Egypt look to be in trouble.

“Central banks may be faced with a choice between letting [inflation] run and sacrificing their currencies on one hand and tightening policy and watching debt-laden economies slide into a recession for which they are ill prepared on the other.”

At the other end we have the US, EU and UK where inflation is galloping along. Central banks may be faced with a choice between letting it run and sacrificing their currencies on one hand and tightening policy and watching debt-laden economies slide into a recession for which they are ill prepared on the other. The Bank of England’s lurch back to QE (albeit in a different guise) may well be a pointer for the path they are most likely to take.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.