China’s New Year Holiday festival is over, and the Year of the Snake is now underway. People with a much keener interest in, and better understanding of, the Chinese zodiac tell this column that the snake signifies intelligence, mystery and renewal. Make of that what you will, but President Xi Jinping and the Communist Party authorities are going to need plenty of the first named if they are to resolve the second and prompt the third when it comes to China’s economy and how to turn it around.

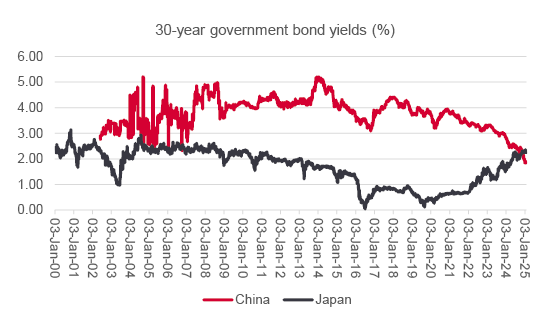

“Fixed-income markets sense a deep-seated malaise, given how the 30-year government bond yield in China now stands below that of Japan.”

A real estate bust, coupled with the need to move away from debt-funded infrastructure spending and reduce reliance upon exports (in the face of further rounds of tariffs from the USA and the West), means China’s growth is slowing, especially as domestic consumption seems slow to develop and take up the slack. Fixed-income markets sense a deep-seated malaise, given how the 30-year government bond yield in China now stands below that of Japan – a sufferer until recently of a 30-year-plus debt deflation, itself the result of an epic, debt-fuelled speculative episode in equities and property in the mid-to-late 1980s. The yields on 10-year paper are close to converging as well.

Fixed-income markets fear deflation in China

Source: LSEG Refinitiv data, UBS.

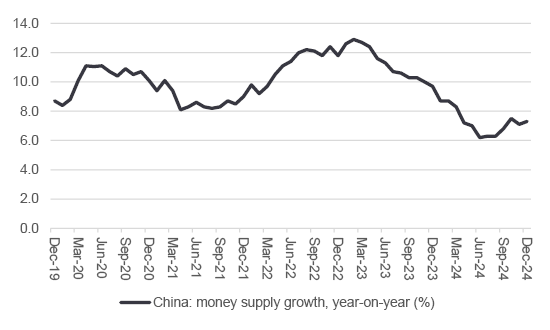

Beijing is alert to the danger. The authorities have already sanctioned interest rate cuts, lower capital requirements for banks to try and boost lending and incentives to stimulate residential property demand. Money supply growth is picking up a little as a result, but December’s 7% year-on-year increase is barely sufficient to sustain China 5% annual GDP growth target.

Chinese money supply growth remains sluggish

Source: LSEG Refinitiv data, UBS.

“Beijing has a delicate economic balancing act, as it seeks to dodge a downward snake and climb an upward ladder. It is not on its own in this respect and, while it may seem old-fashioned, money supply could yet prove a telling indicator for macroeconomic trends elsewhere – including here in the UK.”

More may therefore be required, although China’s currency could come under further pressure if monetary policy eases quickly and bond yields continue to sink. Beijing has a delicate economic balancing act, as it seeks to dodge a downward snake and climb an upward ladder. It is not on its own in this respect and, while it may seem old-fashioned, money supply could yet prove a telling indicator for macroeconomic trends elsewhere – including here in the UK.

In the 1980s, the economist Professor Alan Walters was a huge influence on Prime Minister Margaret Thatcher. A monetarist, he advocated the theories of Milton Friedman, who argued that inflation is “always and everywhere a monetary phenomenon.” In other words, changes in the supply of money would affect its value, just as it would any other product.

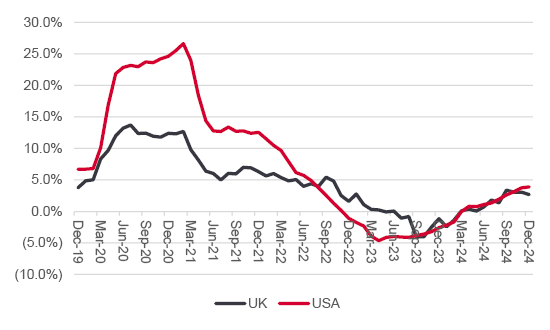

Wind on forty years and this no longer seems to be a fashionable view, but a look at the money supply growth chart for China may be one explanation as to why its annual rate of inflation is all but zero. A surge in money supply in the USA and UK in the early part of this decade, thanks to the deployment of furlough schemes, welfare cheques, interest rate cuts and quantitative easing as a means of fighting the economic effects of COVID-19, was a likely contributor to the subsequent surge in inflation on both sides of the Atlantic.

US and UK money supply growth has eased …

Source: LSEG Refinitiv data, UBS.

The US Federal Reserve and Bank of England then switched policy. They raised interest rates and stopped buying treasuries and gilts and started to sell them, with the result that yields have gone higher and the money supply taps have been tightened, if not quite cut off. Higher rates and Quantitative Tightening may have helped to cool inflation, at least if Friedman’s and Walters’ theories were correct.

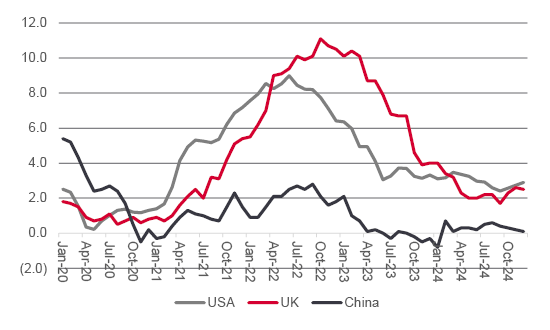

… to the potential benefit of inflation …

Source: LSEG Refinitiv data, Office for National Statistics, US Bureau of Labor Statistics

… as central banks have raised rates and shrunk their balance sheets

Source: Bank of England, FRED – St. Louis Federal Reserve database

“The Monetary Policy Committee was slow to act as inflation rose, and is equally likely to be slow to react as it cools, in a perfectly human attempt to counterbalance the prior error, even in the knowledge that monetary policy works with an 18-to-24-month lag.”

This all matters as China debates how to drag itself out of the mire, President Trump demands that the US Federal Reserve cuts interest rates and the Bank of England debates how far and how fast it should reduce the headline cost of borrowing in the UK. The Monetary Policy Committee was slow to act as inflation rose, and is equally likely to be slow to react as it cools, in a perfectly human attempt to counterbalance the prior error, even in the knowledge that monetary policy works with an 18-to-24-month lag.

Financial markets currently expect two, one-quarter-rate points from the Bank of England this year. Go too slow and inflation could stay above target, too fast and the economy could tip into recession. The latter would need either government spending (when the public finances are already shot) or more QE (when inflation is political poison). Thankfully, the lowly valuation attached to UK equities means investors are not necessarily relying on a positive outcome either way.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.