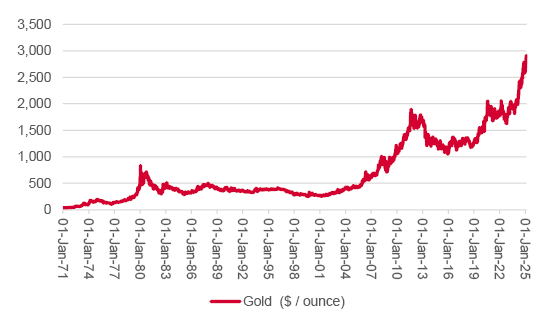

This year’s record highs in the US, UK and German stock markets continue to make headlines, but another, much more unsung asset is also breaking new ground and that is gold, which is trading above $2,900 an ounce for the first time this week.

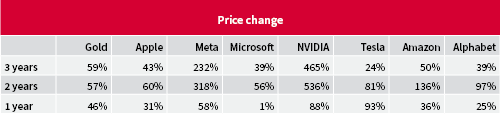

“Gold’s 46% surge in the past year has even outpaced four of the so-called Magnificent Seven, despite markets’ ongoing fascination with technology stocks and all things AI-related, and apparent disinterest in the precious metal.”

Gold’s 46% surge in the past year has even outpaced four of the so-called Magnificent Seven, despite markets’ ongoing fascination with technology stocks and all things AI-related, and apparent disinterest in the precious metal.

The $3,000 mark beckons. On past form, the metal may try and fail to pass that psychological threshold on more than one occasion before kicking on (assuming it makes the breakthrough at all) and this may give advisers and clients chance to think about why gold stands where it does and what needs to happen for its trajectory to continue – or change.

Gold has outperformed the Magnificent Seven

Source: LSEG Refinitiv data, UBS.

It still feels unfashionable to focus on gold, and it is easy to dismiss the case for including the precious metal in even the most balanced of portfolios.

As Warren Buffett succinctly put it in a speech, he gave at Harvard in 1998, “Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.”

“Yet, unusually, the market is shrugging off the Sage of Omaha’s words of wisdom and embracing gold instead in what seems to be the precious metal’s third major bull market since 1970.”

Yet, unusually, the market is shrugging off the Sage of Omaha’s words of wisdom and embracing gold instead in what seems to be the precious metal’s third major bull market since 1970.

Gold is enjoying its third bull run since 1970

Source: LSEG Refinitiv data.

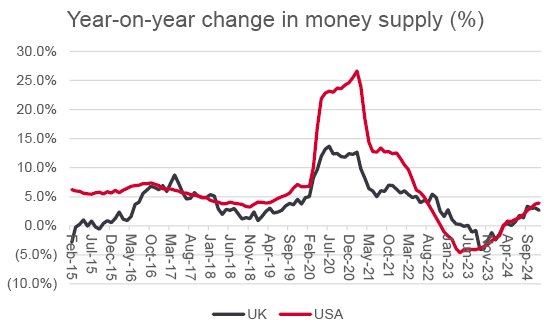

Galloping money supply may have boosted gold this time around

Source: LSEG Refinitiv data, FRED – St. Louis Federal Reserve database

Which of the themes of inflation (or stagflation), money supply growth, Government deficits or central banks being behind the policy curve is helping to drive gold higher this time is something that only advisers and clients can decide for themselves, but there do seem to be some uncanny parallels.

“A further angle may be central bank buying. According to the World Gold Council, central banks added 1,045 tonnes to their reserves in 2024.”

A further angle may be central bank buying. According to the World Gold Council, central banks added 1,045 tonnes to their reserves in 2024. Some have suggested this is a sign that some countries are looking to diversify away from the dollar and reduce their exposure, given how America has sought to use currency and trade sanctions against Russia and the latter against not only China, but would-be geopolitical allies such as Canada and Mexico.

Either way, that was the third year in a row when they gobbled up more than 1,000 tonnes of the precious metal and stories about how gold vaults have struggled to meet demand have begun to multiply.

“Intriguingly, gold mining equities are not embracing the mood. The New York Stock Exchange ARCA Gold Bugs index is no higher now than it was in spring 2006, when the gold price was $550 an ounce, not more than $2,900.”

Intriguingly, gold mining equities are not embracing the mood. The New York Stock Exchange ARCA Gold Bugs index is no higher now than it was in spring 2006, when the gold price was $550 an ounce, not more than $2,900. If – and it remains an ‘if’ – gold does keep going, perhaps miners will start to remind investors not to forget about them, given that statement from Barrick Gold last week (12 Feb) that a 4% change in the gold price, up or down, equates to a $450 million swing in earnings before interest, taxes, depreciation and amortisation (EBITDA), or 9% of the miner’s profits, based on that metric.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.