With a gain of more than 200% in this decade to date, gold is proving its worth as a portfolio diversifier for advisers and clients. That return beats global equities easily and of the major asset classes only the now-flagging Bitcoin and still-shiny silver can point to a better capital return. Even more amazingly, gold can point to a better capital return than the S&P 500 over the past twenty years (though dividends and buybacks from equities close up the gap to almost nothing).

The question now is whether this year’s gyrations in the precious metal markets are a sign of a top, or just the commodities taking a breather after a storming run.

Sceptics will remain firm in their view that the investment case against gold and precious metals is clear cut. They have little industrial use, certainly in the case of gold, generate no cash and thus rely on the greater fool theory for upside, as holders need new buyers to follow in and buy off them for the price to rise.

There also remains the risk that the recognised exchanges tinker with the rules if they feel matters are getting out of hand, as COMEX has just done in the USA by raising its margin requirements for traders, or that government gets involved, as the Roosevelt administration did with Executive Order 6102 in 1933 that effectively forbade private ownership of any scale.

Bulls will counter by pointing to ongoing geopolitical risk, a weak dollar and galloping sovereign debts, especially in the West, where the burden is now so great that inflation and monetary debasement may be the only way to render manageable those borrowings and the associated interest bill. There is, after all, little or no political or public appetite for the sort of austerity that would be required to rein in debt growth, let alone bring about a reduction in absolute terms. The prospect of more central bank money printing, in the form of Quantitative Easing, at the first sign of any economic or financial market trouble is a further consideration for those who still pound the table for precious metals.

Advisers and clients will have their own views on the arguments for and against precious metal exposure, and the policies of incoming US Federal Reserve chair Kevin Warsh could well have a say, too. Mr Warsh’s public statements suggest he is in favour of rapid interest rate cuts (which could weaken the dollar and play to the bull case) but also that he believes the US central bank’s balance sheet is too bloated and that Quantitative Tightening should be used to shrink it (and thus assert the sort of monetary discipline that could weaken appetite for gold).

At this stage, valuation would be used to further frame the debate, but this is more difficult in this instance, because gold and the precious metals generate no cash, an issue which comes back to why master investor Warren Buffett had no interest in them at all.

In the absence of multiples of earnings or a full-blown discounted cash flow (DCF) model, an alternative approach is needed. This can focus on the affordability of gold for would-be buyers, or a study of what it helps holders to buy, to provide a framework of relative, rather than absolute, valuation.

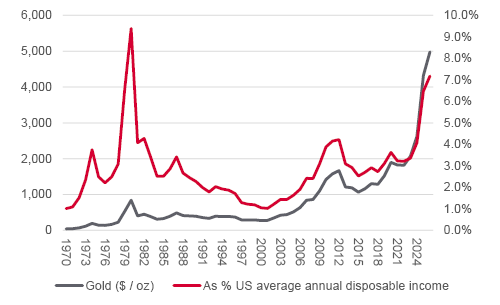

One approach is to look at how the gold price compares to annual disposable income. When gold peaked at $835 an ounce in January 1980, it reached 9.4% of the annual US household’s available annual discretionary spending. Gold currently stands at 7.2% of that figure, and a return to the former high points to a gold price of some $6,500 an ounce, or a third above current levels. Asset and wage inflation (or deflation) could shape this calculation going forward.

Source: Jefferies, FRED – St. Louis Federal Reserve, LSEG Refinitiv data.

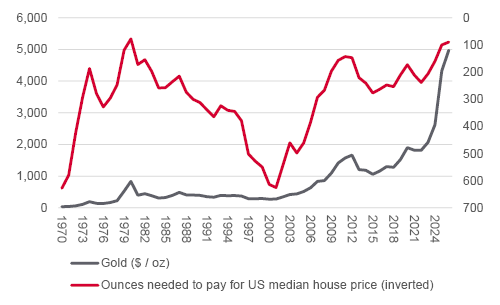

A different technique is to look at gold’s purchasing power, relative to the most important buy anyone makes – a house. A would-be buyer of the average US dwelling would currently need just 90 ounces of gold to cover the cost. This compares to the figure of 78 reached when gold peaked in January 1980. A repeat of that would take gold up by a sixth to around $5,750, again before adjusting for any future increases (or decreases) in US house prices.

Source: Palm Valley Capital, FRED – St. Louis Federal Reserve, LSEG Refinitiv data.

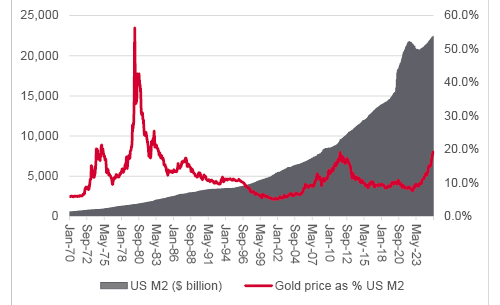

One final test is to look at the value of gold relative to US money supply. This perspective rests on the debasement trade, whereby bulls of gold assert that governments will print or rely on inflation to make their debts, and spending programmes, affordable, rather than turn to austerity or higher taxes.

Source: Myrmikan Research, FRED – St. Louis Federal Reserve, LSEG Refinitiv data.

Here the conclusion is that gold is way below past peaks relative to the M2 measure of money supply in the US. A return to the 1980 high would take gold above $12,600 an ounce, although it is worth bearing in mind, in this case and the other two, that gold did not hold that zenith for long at all forty-six years ago.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.