The press coverage garnered by Scion Asset Management’s Michael Burry, the man who did so much to protect his clients from the damage caused by the Great Financial Crisis and inspired the book and the film The Big Short, for just a few tens of millions of dollars’ worth of put options on AI darlings NVIDIA and Palantir is interesting. The rebuttals from both companies’ chief executives were speedy, but so were wobbles in their share prices, as some investors looked on nervously at both the profits they have accrued in the stocks, and the spending plans of the biggest AI players. For some, previously copious free cash flow is drying up, for others the funding sources remain unclear, if not downright opaque.

All of this brings into relief once more the lop-sided nature of the US equity market. Technology and AI-related stocks dominate, often in unexpected ways. Meanwhile, marked underperformance from sectors such as industrials, financials and real estate suggests America’s economic outlook may not be as robust as it seems. Yet these sectors’ faltering returns could mean they are worthy of further research, just as many of these sectors were when COVID-19 and lockdowns were doing their worst.

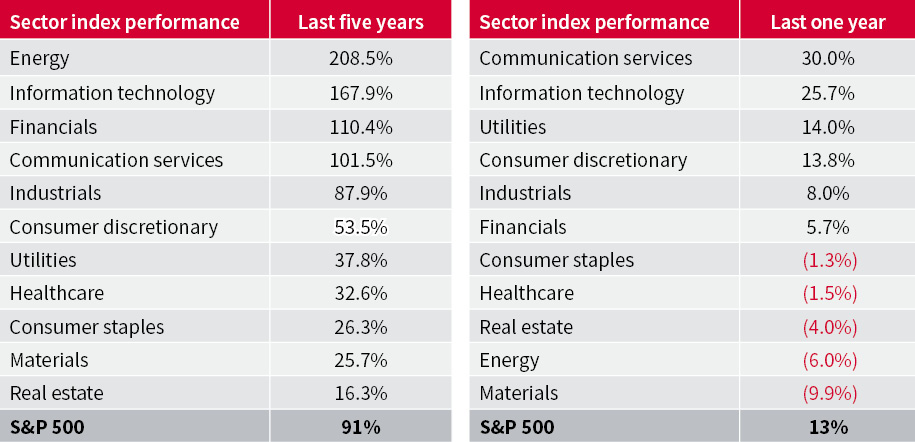

Take a five-year view, and go back to ‘Pfizer Monday,’ and the S&P 500 looks reasonably balanced with energy and financial stocks among the vanguard, alongside information technology and communication services and industrials. This mix flags not only American dominance in tech and AI, but also the strong nature of the economic rebound post-COVID, not to mention the value that can be accrued by buying sectors when their fortunes are at their lowest ebb and valuations are washed out (as was the case with energy and financials back in 2020).

But a one-year view leaves the US equity market’s foundations looking more reliant on a narrower leadership group.

The presence of communication services is a bit deceptive, as this usually defensive sector’s three largest stocks are Alphabet, Meta Platforms and NVIDIA. Information technology, dominated by NVIDIA, Apple and Microsoft speaks for itself. However, two of the three biggest consumer discretionary names are Amazon.com and Tesla and the utilities are doing well as investors ponder who will provide the energy that powers and cools the data centres and servers needed for the computing and inference capabilities of the large language models that underpin AI.

AI and technology-related sectors dominate in the USA, sometimes in deceptive ways

Source: LSEG Refinitiv data

Again, the contrastingly poor showing from cyclical sectors jumps out, as do the turgid returns from the energy and materials sectors in the past twelve months. Weak oil and gas prices are not helping the former, while the latter may well be worried about tariffs and global trade.

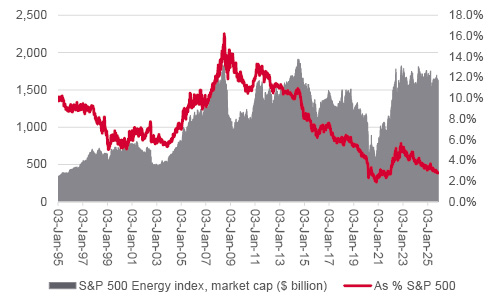

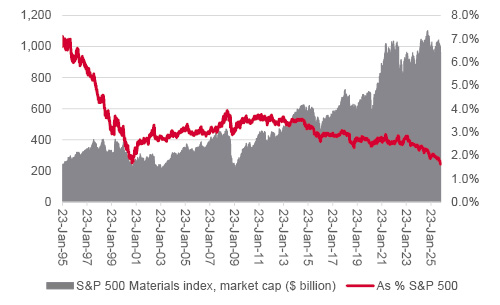

The net result of these trends is that the ‘Magnificent Seven’ of Alphabet, Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla now represent nearly 40% of the S&P 500’s stock market capitalisation between them. At the other end of the scale, the energy sector is now worth just 2.8% of the headline index and materials just 1.6%, even if the importance of energy and resource independence seems clearer than ever in light of the war in Ukraine, fragile peace in the Middle East and ongoing tensions over the supply of critical minerals with China, to name but one.

Weak oil and gas prices mean the energy sector is again unloved…

Source: LSEG Refinitiv data

…while materials’ index weighting is down to a record low

Source: LSEG Refinitiv data

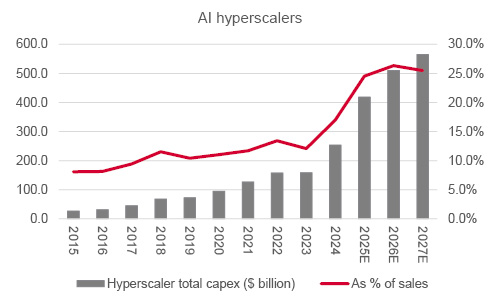

Granted, the materials sector is not a pure play on mining and metals, as steels, chemicals and other cyclical industries feature (many of them the ones that President Trump’s tariff plans are trying to prop up and save). But the lack of interest in both sectors is startling, especially when their spending discipline and frugality contrasts so markedly with the tidal wave of spending unleashed by those who are scrambling to cement a leading position in AI. Such is the scale of their outlay, that investors are becoming more nervous about funding and the returns that may be accrued, with some even wondering whether, on the horizon, lurks a spending bust to match that witnessed when the technology, media and telecoms bubble collapsed in the early 2000s.

The hyperscalers continue to pour money into AI

Source: Company accounts, Marketscreener, analysts’ consensus forecasts for Alphabet, Amazon.com, Meta Platforms, Microsoft and Oracle

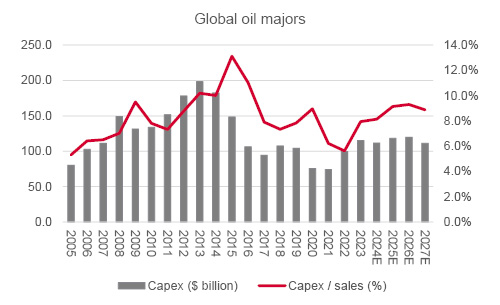

Big oil is exercising considerable restraint when it comes to capital investment, and that spending includes renewables and not just oil and gas fields. It seems logical to assume that supply of hydrocarbons will only grow slowly, and that it will take time to bring on new fields, even if demand for energy worldwide continues to grow.

Big oil is showing much greater spending restraint…

Source: Company accounts, Marketscreener, consensus analysts' forecasts for BP, Chevron, ConocoPhillips, ENI, ExxonMobil, Shell and TotalEnergies

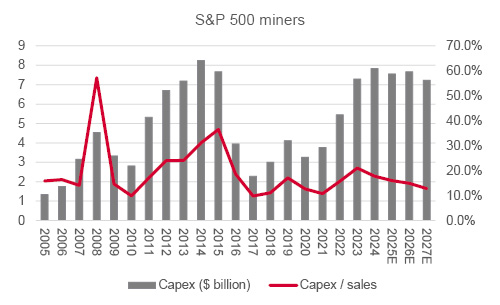

The same could be said for metals. Mines cannot be developed at the flick of a switch. The spending boom for the early 2000s sowed the seeds for the commodity price weakness of the 2010s but there has now been a decade of restraint.

…as are US miners…

Source: Company accounts, Marketscreener, consensus analysts' forecasts for Freeport-McMoRan and Newmont

This lack of supply could prove telling, if demand picks up, thanks to wider economic growth, the electrification trend or even just demand from advisers and clients who may feel they trust ‘hard’ assets more than paper promises, such as cash and bonds, especially if inflation rips higher or Western governments continue to rack up fresh borrowing.

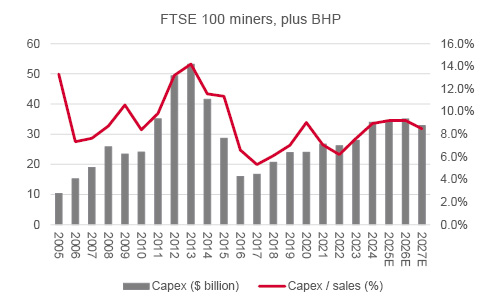

…and other leading metal and mineral producers

Source: Company accounts, Marketscreener, consensus analysts' forecasts for Anglo American, Antofagasta, Endeavour Mining, Fresnillo, Glencore, Rio Tinto and BHP.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.