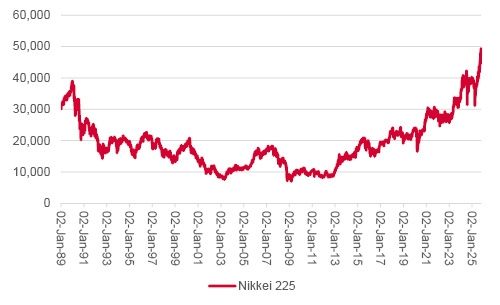

Japan’s Nikkei 225 stock index is approaching an all-time high following the appointment of Sanae Takaichi as leader of the Liberal Democratic Party and Prime Minister (PM) and her selection, in turn, of Finance Minister, Satsuki Katayama. The 50,000 mark is tantalisingly within reach.

“The top two posts in Japanese politics will be held by women for the first time, but markets seem even more interested in comparisons between Takaichi and Shinzō Abe. This is because of the similarities between their policy proposals and political preferences.”

The top two posts in Japanese politics will be held by women for the first time, but markets seem even more interested in comparisons between Takaichi and Shinzō Abe. This is because of the similarities between their policy proposals and political preferences. Abe’s reform programme, dubbed ‘Abenomics’, is widely credited with dragging the Japanese economy out of a twenty-year deflationary funk and boosting the Nikkei at the same time, so it is easy to understand why equity investors may be getting excited.

Japan’s Nikkei 225 is approaching an all-time high

Source: LSEG Refinitiv data

Abe’s failed first stab as Prime Minister in 2006-07 quickly became a distant memory after he swept back into power in December 2012 and immediately announced his so-called ‘Three Arrows’ programme, which targeted:

The goals were to get Japan's economy back on a consistent growth path, after the quarter-century of stagnation that followed the bursting of the 1980s’ debt-fuelled property and equity bubble, and drive inflation toward the Bank of Japan’s 2% target.

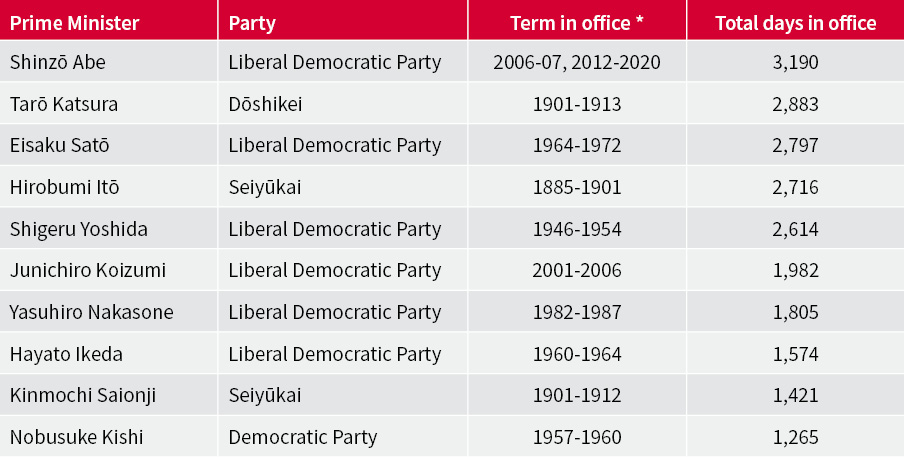

Abe largely succeeded, with the result that he became Japan’s longest-serving Prime Minister, as he added General Election victories in 2014 and 2017 to that of 2012. The Nikkei also took flight as it surged from just under 10,000 when Abe took office to more than 22,000 by the time he stepped down owing to illness in summer 2020.

Abe became Japan’s longest-serving Prime Minister...

Source: www.japan.kaneti.go.jp. *Dates span all periods in office which may not have been consecutive*

...and the most successful one for investors in Japanese equities

Source: www.japan.kaneti.go.jp. *Capital gain, local currency terms. **LDP = Liberal Democratic Party. DPJ = Democratic Party of Japan. JSP = Japan Socialist Party. JRP = Japan Renewal Party. JNP = Japan New Party.

“Kataichi won control of the LDP and then the role of Prime Minister, following the resignation of her predecessor Shigeru Ishiba, by calling for more fiscal stimulus, loose monetary policy from the Bank of Japan and the wider restart of Japan’s fleet of nuclear power plants, where only a handful of 54 reactors are operating some fourteen years after the accident at Fukushima.”

Kataichi won control of the LDP and then the role of Prime Minister, following the resignation of her predecessor Shigeru Ishiba, by calling for more fiscal stimulus, loose monetary policy from the Bank of Japan and the wider restart of Japan’s fleet of nuclear power plants, where only a handful of 54 reactors are operating some fourteen years after the accident at Fukushima. In a further nod to Abe and his programme, the PM is focusing upon national security, as well as energy security, since she also wishes to change Article Nine of the (pacifist) Japanese constitution, whereby Japan can strengthen its military capability. Kataichi is already proposing an increase in defence spending to 2% of GDP.

“However, there are some key differences between now and the situation that Abe inherited, even if the desired direction of travel is the same.”

However, there are some key differences between now and the situation that Abe inherited, even if the desired direction of travel is the same.

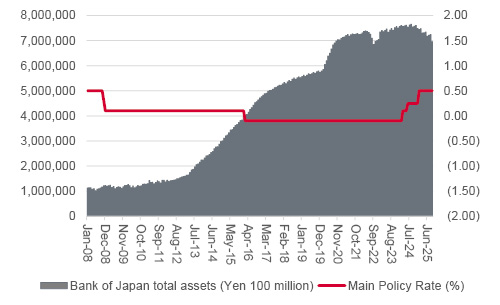

The Bank of Japan is slowly tightening monetary policy in response to inflation

Bank of Japan, FRED – St. Louis Federal Reserve, LSEG Refinitiv data

“There is one final key difference: the Nikkei is now nearly five times higher than when Abe returned to office nearly thirteen years ago. Japanese equities are not as cheap as they were.”

There is one final key difference: the Nikkei is now nearly five times higher than when Abe returned to office nearly thirteen years ago. Japanese equities are not as cheap as they were. However, the Nikkei still stands on 1.6 times book value, compared to the 2.4 times peak reached in the late 1980s, and the early 2000s trough of just 0.8 times, so bulls of the market may argue there is still upside potential, especially given the improvements in Japanese corporate governance, shareholder relations and returns on equity seen over the past decade.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.