At the time of writing, no date is set for the second Budget of this Labour Government, but investors – or at least bond market vigilantes – seem to be getting edgy, at least if the yields on UK sovereign bonds, or gilts, are a reliable yardstick (and they usually are).

Gilt yields are starting to crawl higher, and thus prices are going lower. At 4.73% at the time of writing, the yield on the benchmark ten-year gilt is within touching distance of the 4.84% sixteen-year high reached back in January. At 5.60%, the 30-year instrument’s yield is nearing a mark not seen since 1998.

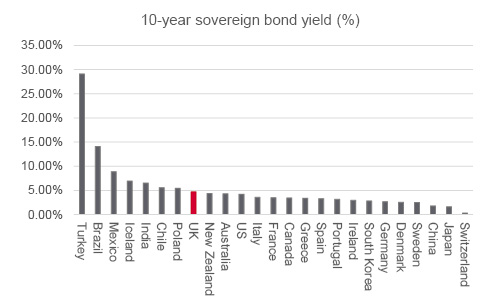

“The result is that it is costing the UK Government more to issue ten-year debt than any of Portugal, Ireland, Italy, Greece and Spain, the so-called PIIGS whose sovereign borrowings caused such angst in the early 2010s.”

The result is that it is costing the UK Government more to issue ten-year debt than any of Portugal, Ireland, Italy, Greece and Spain, the so-called PIIGS whose sovereign borrowings caused such angst in the early 2010s.

The UK ten-year gilt yield is high by global standards...

Source: LSEG Refinitiv data.

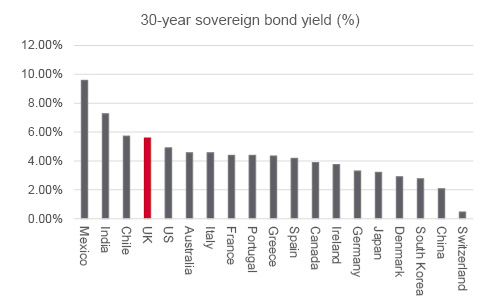

The same applies to 30-year paper. None of this, alas, looks like a vote of confidence in the UK’s economic outlook or Labour’s ability to stick to its carefully laid-out fiscal rules, at least without some politically unpalatable tax increases, spending cuts, or both.

...and the thirty-year yield exceeds that demanded of any of the debt-stricken PIIGS of the 2010s

Source: LSEG Refinitiv data.

Back in 1998, Tony Blair was Prime Minister and Gordon Brown Chancellor of the Exchequer. Inflation was subdued, at below 2% based on the consumer price index, but annual GDP growth that year was 3.4%, a far superior rate of growth to that of 2025. The Bank of England base rate therefore exceeded 7% all the way through to November 1998, when rapid cuts were deployed by the then Governor Eddie George, as part of a globally co-ordinated response to the Asian debt crisis and subsequently LTCM hedge fund failure.

“Healthy GDP growth, ‘Cool Britannia’ feelgood and financial market volatility were thus the order of the day 26 years ago. This time around, however, inflation, tariffs and Government debt seem to be the key issues that are niggling bond vigilantes.”

Healthy GDP growth, ‘Cool Britannia’ feelgood and financial market volatility were thus the order of the day 26 years ago. This time around, however, inflation, tariffs and Government debt seem to be the key issues that are niggling bond vigilantes.

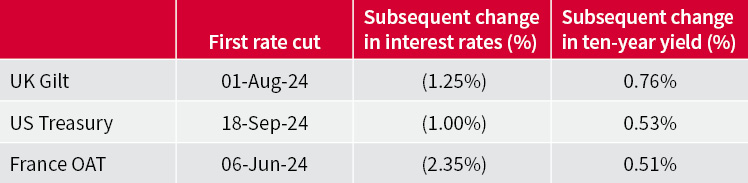

Interest rate cuts from the Bank of England have made no difference, either. Benchmark gilt yields have gone up in the UK since the first reduction in headline borrowing costs of this cycle sanctioned by Governor Bailey and the Monetary Policy Committee a year ago.

“Nor will the Labour Government, Treasury or Bank of England take comfort from how France is in the same situation, especially as efforts in Paris to impose any kind of fiscal order have led to public unrest, while coming to naught. Next week’s vote of confidence in the current Prime Minister, François Bayrou, may only heighten worries about France’s ability to manage its borrowing.”

It will be scant consolation that the UK is keeping company here with America, where the Trump administration continues to run policies designed to stoke growth, generate tax revenue from tariffs and keep interest rates low, in an attempt to manage a galloping Federal debt and interest bill. Nor will the Labour Government, Treasury or Bank of England take comfort from how France is in the same situation, especially as efforts in Paris to impose any kind of fiscal order have led to public unrest, while coming to naught. Next week’s vote of confidence in the current Prime Minister, François Bayrou, may only heighten worries about France’s ability to manage its borrowing.

French, American and British sovereign yields have risen even as central banks have cut interest rates

Source: LSEG Refinitiv data.

Over the last month, the UK two-year gilt yield is up by seven basis points (0.07%), the ten-year by fifteen (0.15%) and then thirty-year by twenty-three (0.23%).

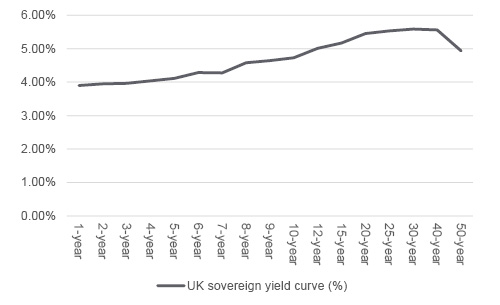

As a result, the yield curve shows something a little more akin to a ‘normal’ yield curve, where lenders (or bond buyers) demand a higher return from longer-dated paper to compensate themselves for the increased scope for something to go wrong during the additional life time of the gilts, such as changes in interest rates, higher inflation or, at worst, a default by the issuer (or borrower).

The UK sovereign bond yield curve is starting to steepen

Source: LSEG Refinitiv data.

“This also means the UK is offering a so-called ‘bear steepener,’ when both short- and long-term yields are rising but long-term ones are rising faster to widen the gap between the two.”

This also means the UK is offering a so-called ‘bear steepener,’ when both short- and long-term yields are rising but long-term ones are rising faster to widen the gap between the two.

Such a trend can be bad news for bonds in particular, as prices fall when yields rise, and it can be a sign inflation is on the rise. It could be a challenge for share prices, too, as it combines higher discount rates (that lower the theoretical value of the long-term cash flows of long duration sectors like tech and biotech) with tighter monetary policy that hits the earnings power of short-duration, cyclical industries. This means it is not just bond vigilantes, but advisers and clients with UK equity exposure as well, who will have keep tabs on the rumour mill regarding possible policy interventions from Chancellor Rachel Reeves ahead of the Budget as she looks for a way to keep financial markets, her own backbenchers and voters happy, while sticking to her own ‘fiscal rules’ and the Government’s growth agenda.

Past performance is not a guide to future performance and some investments need to be held for the long term.

Russ Mould assesses Rachel Reeves’ first year as Chancellor and what it could mean for markets and your clients.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.