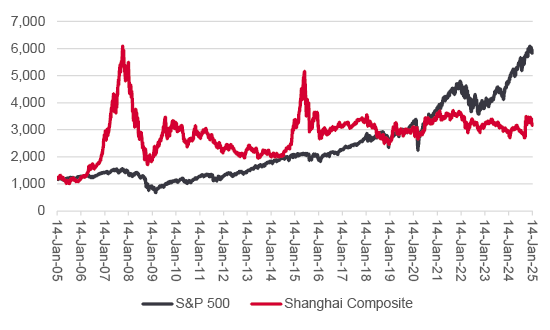

The USA and China are at loggerheads, philosophically, politically and economically – though thankfully not in military terms – and the contrast between how the two are perceived by financial markets could hardly be greater. Stock markets offer part of the story, as America’s headline indices sit at or near to all-time highs, while the Shanghai Composite equity benchmark languishes where it did back in spring 2007.

US equity markets continue to surge as China swoons again

Source: LSEG Refinitiv data.

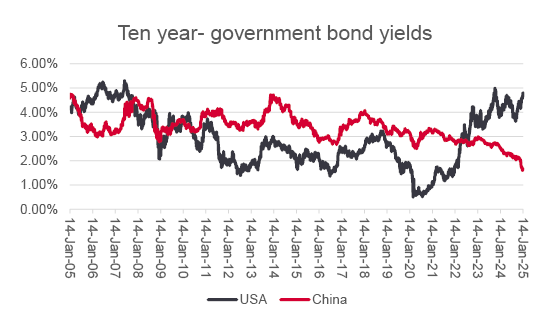

Even more telling are the different trajectories of the countries’ respective government bond markets. The yield on the ten-year Chinese sovereign bond has collapsed to what looks like an all-time low of 1.60%, while the US equivalent is pushing toward twenty-year highs.

Sovereign bond yields are plunging in China and rising in the USA

Source: LSEG Refinitiv data.

“At first glance, the trends in fixed-income markets may also reflect the mood of American optimism, as markets embrace President-Elect Trump’s agenda of tax cuts and deregulation and anticipate faster economic growth (albeit perhaps at the cost of hotter inflation) and fret about China’s economic trajectory in the wake of an epic real estate bust.”

At first glance, the trends in fixed-income markets may also reflect the mood of American optimism, as markets embrace President-Elect Trump’s agenda of tax cuts and deregulation and anticipate faster economic growth (albeit perhaps at the cost of hotter inflation) and fret about China’s economic trajectory in the wake of an epic real estate bust.

It may be that bond markets are pricing in a slowdown in interest rate cuts from the US Federal Reserve and a shift to looser monetary policy from the People’s Bank of China, which traditionally steers bank lending rather than adjusts the price of money as its main tool of control.

But there may be another trend at work, at least in the USA, which advisers and clients might like to ponder, especially as the S&P 500 now represents almost two-thirds of the market capitalisation of the FTSE All-World, a level that exceeds the prior high achieved at the peak of the technology, media and telecoms (TMT) bubble in 2000.

US equities stand at a record high as a percentage of global market

Source: LSEG Refinitiv data.

“It can also be argued that there are parallels between President-Elect Trump’s agenda and the supply-side policies implemented by Ronald Reagan to great effect in the early 1980s, which did so much to revive America’s economy and financial markets alike.”

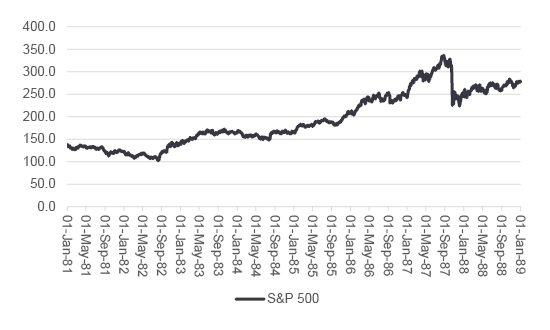

It is easy to understand why there is such enthusiasm for US assets, not least as mood tends to be led by price, given the temptation is to assume that what has worked for a long time will keep on working. It can also be argued that there are parallels between President-Elect Trump’s agenda and the supply-side policies implemented by Ronald Reagan to great effect in the early 1980s, which did so much to revive America’s economy and financial markets alike.

US equities stumbled before Reagan’s reforms really took hold

Source: LSEG Refinitiv data.

“However, there are some differences which do not sit entirely comfortably with such a beguiling narrative.”

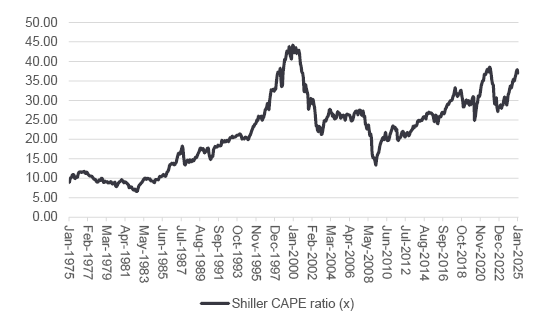

However, there are some differences which do not sit entirely comfortably with such a beguiling narrative. First, the US economy double dipped as Reagan’s first administration applied what it saw as the necessary reforms. Second, the S&P 500 was much less highly valued than now, using Professor Robert Shiller’s cyclically adjusted price earnings (CAPE) ratio as a guide. Finally, the US Federal deficit was barely 30% of GDP in 1981, compared to 120% now, to leave Reagan with so much more room for fiscal manoeuvre.

US equities were much cheaper when Reagan began his reforms

Source: https://shillerdata.com/

Finally, expectations were just so much lower. Indeed, America still viewed itself as under threat from a new rising economic power throughout the 1980s – only back then Japan was seen as the threat. Such fears were heightened by Sony’s purchase of music company CBS in 1988 and movie studio Columbia in 1989 and then encapsulated in Michael Crichton’s 1992 novel Rising Sun, by which time, ironically, the debt-fuelled Japanese property and debt bubble had well and truly popped, given how the Nikkei-225 stock index peaked on 31 December 1989.

The tale of woe represented by China’s sovereign bond and equity markets may not suggest America has much to worry about, but the warning offered by the Japanese experience may yet also have a bearing, unlikely as that may seem right now, especially as China has tripped up twice in the last twenty years thanks to speculative boom-and-bust cycles in equities and then property.

“In the cases of both Japan and then China, debt had a huge role to play, so it may yet prove significant that America’s government, corporations and consumers have continued to pile up their borrowings.”

In the cases of both Japan and then China, debt had a huge role to play, so it may yet prove significant that America’s government, corporations and consumers have continued to pile up their borrowings. The surge in ten-year US Treasury yields may reflect Trump’s apparent desire to let the American economy run hot (and strong nominal growth could indeed help to salt down the debt-to-GDP ratio).

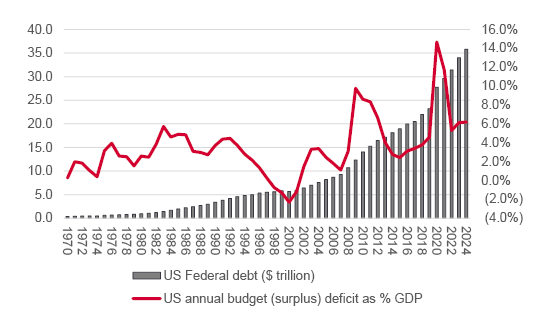

US annual budget deficit is unusually high for a non-recession year

Source:FRED – St. Louis Federal Reserve database.

But it may simply reflect how the total federal deficit is $36 trillion and rising, the annual deficit is running at 6% of GDP when the economy is growing and the stock market booming (to the benefit of the tax take) and the interest bill exceeds $1 trillion a year – with the result that supply of Treasuries could be about to rise, and fast. Bond vigilantes could therefore still have a say before a lid is put on benchmark US sovereign bond yields, especially if they demand the sort of hair-shirt policies enacted by Reagan, which brought long-term gain, but short-term pain.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.