As fund management legend and founder of Vanguard John Bogle once noted, “The stock market is a giant distraction from the business of investing. In the long run, investing is about the returns earned by businesses, not the stock market.” In other words, sentiment may drive prices in the near term but in the end, it is profits and cash flows that drive valuation.

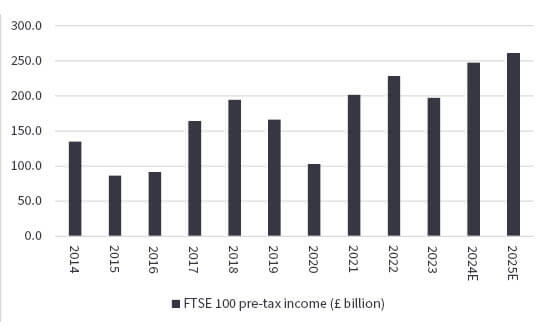

From the point of view of those advisers and clients with exposure to the UK equity market, the bad news is that aggregate consensus forecasts for the members of the FTSE 100 index fell by 4% in the first six months of this year, to £247 billion from £258 billion.

The good news is that £247 billion figure is still a record high, and it therefore helps to justify why the index is trading close to an all-time peak. (Further progress, to £261 billion, is expected by analysts for 2025). And the 2024 number is enough to put the UK stock market on barely 12 to 13 times forward earnings for this year, when Europe is on 13 times, Japan 16 times and the USA a meaty 23 times, according to consensus analysts’ forecasts.

“The UK therefore (still) looks cheap. Advisers and clients now have to decide whether the earnings forecasts are any good, what momentum is like, and what are the biggest swing factors (to the upside and downside), as the answers to those questions may help them determine whether the UK equity market is cheap and undervalued or cheap because it simply deserves to be so.”

The UK therefore (still) looks cheap. Advisers and clients now have to decide whether the earnings forecasts are any good, what momentum is like, and what are the biggest swing factors (to the upside and downside), as the answers to those questions may help them determine whether the UK equity market is cheap and undervalued or cheap because it simply deserves to be so.

FTSE 100 aggregate profits are expected to hit a record high in 2024

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

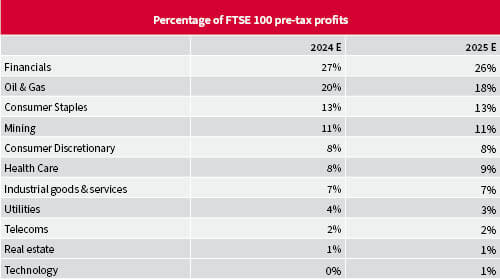

The easiest way to knock the FTSE 100, especially relative to the USA, is to point out its lack of exposure to secular growth sectors such as technology. The UK’s premier index is instead heavily weighted toward financials, oils, consumer staples and miners. Three of those are cyclical and hard to forecast, while one rather plods by comparison with technology. Applying these criteria, the UK does deserve a discount to America. That said, an era of higher inflation, higher nominal GDP growth and higher interest rates may be a better environment for cyclicals and financials than the low inflation, low growth, low rates sludge of the 2010s which put a much greater premium on secular growth and long-duration assets.

Financials, oils, miners and consumer staples dominate FTSE 100 earnings

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

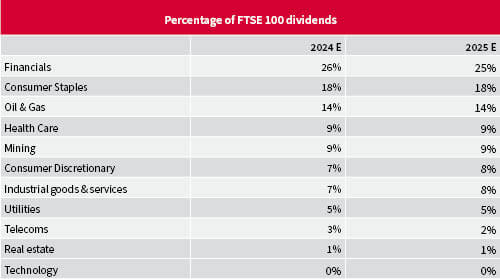

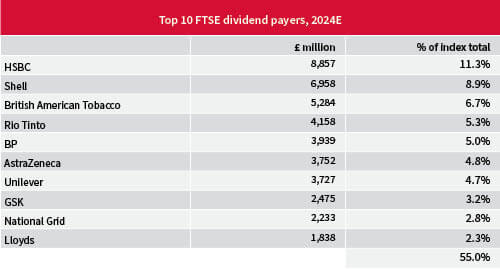

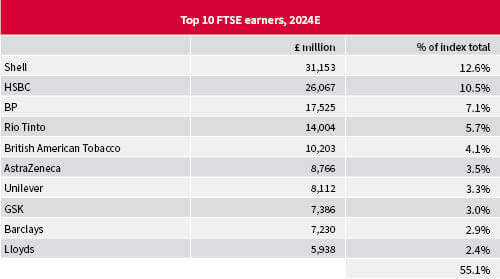

This also raises the issue of concentration risk, as ten firms represent 55% of forecast FTSE 100 pre-tax income in 2024, and ten firms represent 55% of forecast dividends. There is some overlap between the names, but advisers and clients who wish to have exposure to the UK in the equity portion of their portfolios need to be comfortable with these stocks in particular, from the point of view of fundamentals, valuation and, perhaps, an ethical, social and governance (ESG) perspective, given the preponderance of miners, tobacco producers and oils.

Just ten firms represent more than half of the FTSE 100’s forecast profit and dividends

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

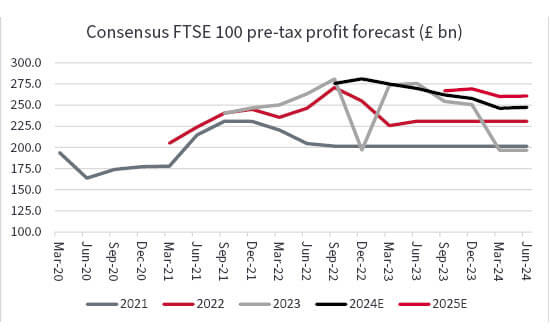

The small drift lower in FTSE 100 aggregate pre-tax income forecasts may not encourage everyone, either, although the USA has seen a similar degree of downgrades to consensus estimates for 2024.

FTSE 100 profit forecasts have drifted slightly lower in 2024

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

“The UK may offer more political stability than previously, after Labour’s General Election win, and that may be a nice contrast to parts of Europe or even the USA, where a fractious Presidential campaign is just hitting top gear and another disputed result is a possibility.”

Moreover, the FTSE 100 has managed a 6% capital gain despite those (modest) earnings downgrades, so that is the equivalent of a 10% re-rating already, to suggest someone, somewhere is warming to UK equities. The UK may offer more political stability than previously, after Labour’s General Election win, and that may be a nice contrast to parts of Europe or even the USA, where a fractious Presidential campaign is just hitting top gear and another disputed result is a possibility. It can also be argued that interest rate cuts may be coming, and the UK may be emerging from a slowdown just as the US enters one, while cash returns remain a potential source of support.

“Add in £10.8 billion of forecast dividends from the FTSE 250 and £38.2 billion of live or completed takeover offers and the FTSE 350 is offering £169.1 billion in total cash returns (dividends plus buybacks plus takeovers) on its £2.5 trillion market capitalisation for a ‘cash yield’ of 6.8%.”

FTSE 100 firms are expected to pay £78.6 billion in ordinary dividends in 2024, with £3 billion in special dividends from HSBC on top, and they are running share buybacks worth £38.5 billion. Add in £10.8 billion of forecast dividends from the FTSE 250 and £38.2 billion of live or completed takeover offers and the FTSE 350 is offering £169.1 billion in total cash returns (dividends plus buybacks plus takeovers) on its £2.5 trillion market capitalisation for a ‘cash yield’ of 6.8%.

That figure compares very favourably to the 5.25% Bank of England base rate, the ten-year gilt yield of 4.09% and the prevailing rate of inflation which is down to 2.0%, based on the consumer price index.

None of this is to say the UK is going to go up like a rocket. But its lowly valuation means it still feels unloved and unloved can mean undervalued. As the old market saying goes, you can have cheap stocks and good news – just not both at the same time.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.