Everyone seems to be talking down the UK’s economic prospects, but no-one has told Virgin Money UK. The bank is increasing cash returns to shareholders as net interest margins rise, loan losses remain modest and cost control is good,” says AJ Bell investment director Russ Mould. “The FTSE 250 firm does expect increased sour loan provisions in its new fiscal year to September 2023, but analysts have already pencilled in a big drop in profits and the shares trade at a huge discount to net asset value, so this is hardly a shock either and that may be why the shares are rising sharply.

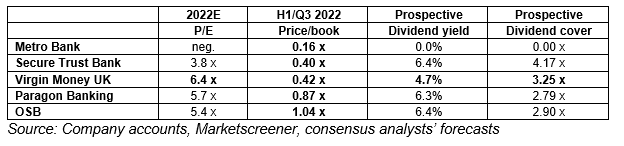

Virgin Money UK’s share price is 160p, but the firm’s latest net asset, or book, value per share figure is 383p, so investors are effectively buying £1 of assets per share for 42p.

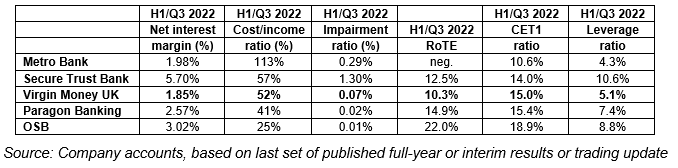

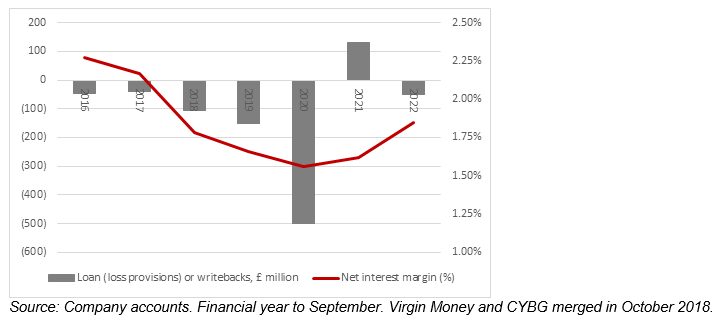

That could look like an opportunity, given how loan losses remain low (at just 0.07% of loans outstanding), return on equity is still in double figures and the net interest margin has improved to 1.85%, as interest rates and bond yields rise.

The bank does acknowledge that provisions for bad loans will increase in the year to September 2023, to around 0.30% to 0.35% of the loan book. Provisions for cost cuts will also burden the profit and loss account in the new financial year (even if they are designed to bring long-term gains) but a further modest improvement in net interest margins should help support earnings and keep return on equity in the low double-digit percentage range, if management’s guidance proves accurate.

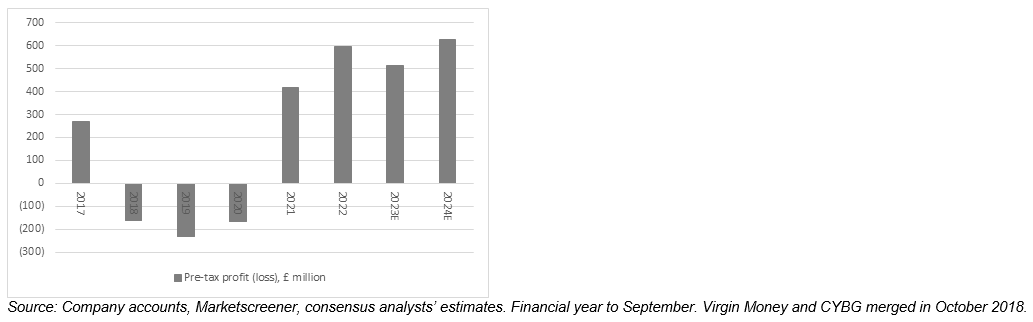

The expectation that loan loss provisions will start to normalise reflects the gloomy outlook for the UK economy, as well as the mortgage market, and consensus forecasts are factoring in a double-digit percentage drop in earnings in fiscal 2023.

That anticipated profits slide explains why the shares have been so weak for much of 2022, although they have now started to rally, partly because the valuation starting point is lowly and partly because of the prospect of further cash returns.

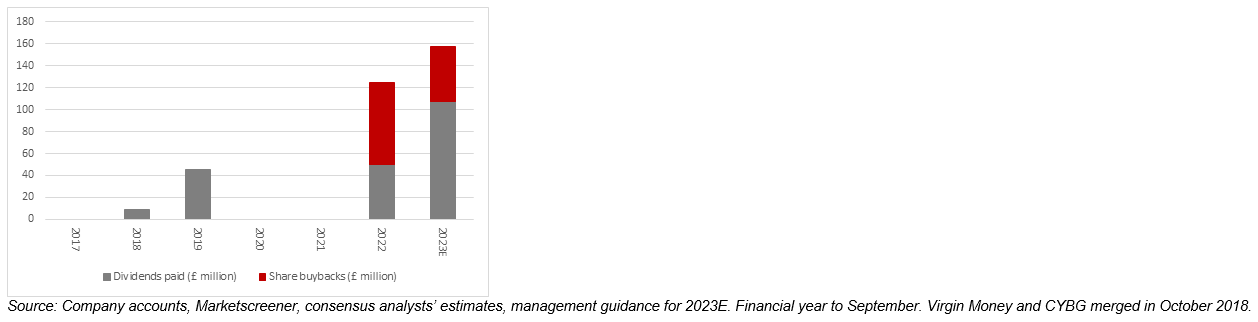

A 30% pay-out based on consensus analysts forecasts implies a drop in the full-year dividend to 7.7p from 10p a share in 2023, but that equates to a 4.7% forward dividend yield with cover of more than three times. Moreover, Virgin Media is now adding share buybacks to the mix, with the goal of a £50 million programme to follow the £75 million one of fiscal 2022.

Add together the dividend per share implied by the plan to pay out 30% of 2023’s net profit in dividends and top that up with £50 million in buybacks and Virgin Money UK could return some 7% of its market cap in cash to shareholders in just one year.

No wonder the shares are up so strongly, especially after a lengthy spell in the doldrums – they still trade at barely half their 2018 peak – as buying back stock at a discount to net asset value is just about the surest way to create the shareholder value that there is.

Fellow challenger banks OSB and Paragon are also running buyback programmes to supplement dividend payments, while all of the Big Five FTSE 100 lenders have declared buyback schemes in 2022. Based on their latest pronouncements, Barclays, HSBC, Lloyds, NatWest and Standard Chartered are due to buy back more than £7 billion of stock this year.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.