Equity markets are buoyant, fixed income markets seem more nervous – judging by how yields are rising (at least for government issue in the developed West) – and commodity prices continue to march to their own beat, as gold and silver surge, industrial metals largely flatline, and oil and gas remain subdued.

“The (relative) calm that pervades hydrocarbon prices is in many ways surprising, given the ongoing war in Ukraine, Russia’s role as a top-three supplier worldwide, and heightened tensions in the Middle East.”

The (relative) calm that pervades hydrocarbon prices is in many ways surprising, given the ongoing war in Ukraine, Russia’s role as a top-three supplier worldwide, and heightened tensions in the Middle East.

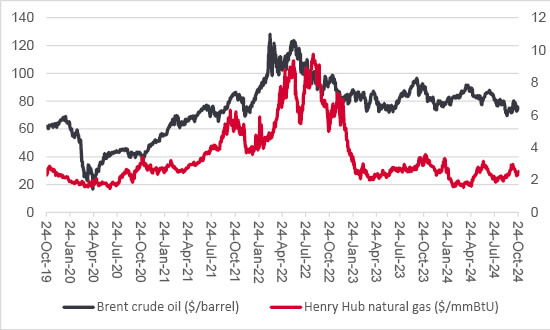

Oil and gas prices trade a long way from recent peaks

Source: LSEG Refinitiv data

There are clearly far more important, humanitarian issues at stake in both conflicts, but, from the narrow perspective of financial markets, investors must pay attention too, especially because of oil and gas. Equity markets’ preferred scenario of cooling inflation, a soft landing for Western economies and lower interest rates from central bank is playing out to perfection, with the result that indices such as the S&P 500 and NASDAQ Composite in the US, DAX and MIB-30 in Europe, and even the benighted FTSE 100 trade at or very close to multi-year or even all-time highs.

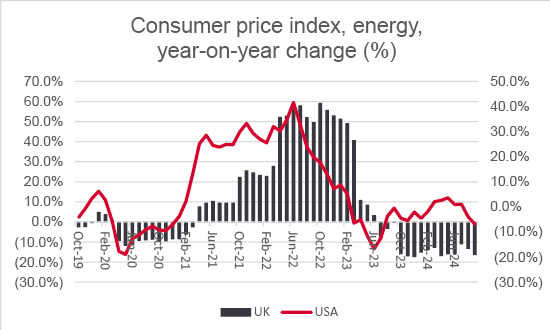

Weakness in energy prices is a key part of this, as it is feeding into lower inflation. Any resurgence in hydrocarbon prices could therefore lead to an upset, and it should be worth assessing the key sensitivities here as part of any risk management process.

Energy components of consumer price indices are helping to cool headline inflation rates

Source: LSEG Refinitiv data

“Near-term sentiment toward oil and gas prices remains broadly negative for three reasons.”

Near-term sentiment toward oil and gas prices remains broadly negative for three reasons.

Overlaying of all of this remains the long-term issue of the global transition toward more renewable sources of energy and away from hydrocarbons which should, in theory, dampen demand for oil in particular.

“Central bankers, politicians and consumers will doubtless all be hoping the IEA’s prognosis about oil demand and supply proves correct and energy prices remain contained, as may environmental campaigners.”

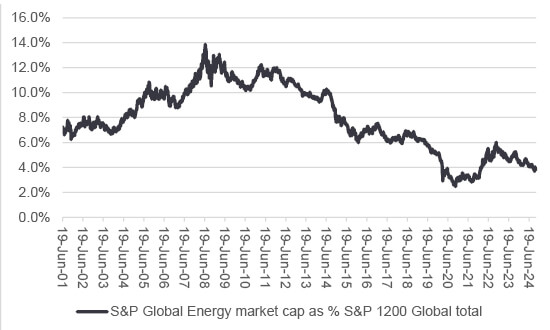

Central bankers, politicians and consumers will doubtless all be hoping the IEA’s prognosis about oil demand and supply proves correct and energy prices remain contained, as may environmental campaigners. Only oil company executives and shareholders may be less pleased, and in the case of the latter they will note the S&P Global 1200 Energy sector is back down to just 3.8% of total S&P Global 1200’s market capitalisation. Indeed, the S&P Global 1200 Energy sector’s entire market cap of $2.7 trillion is less than that of Apple, NVIDIA or Microsoft.

Energy and oil stocks are out of favour once more

Source: LSEG Refinitiv data

“However, it could be unwise to write off oil just yet, also for three reasons.”

However, it could be unwise to write off oil just yet, also for three reasons.

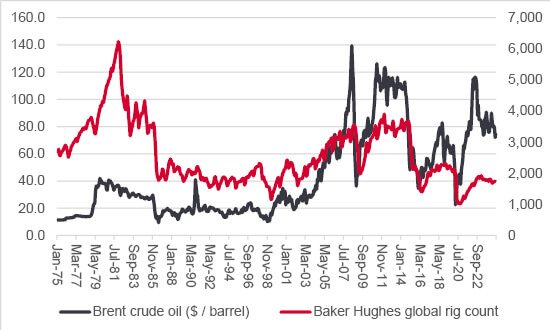

Global drilling activity remains depressed

Source: Baker Hughes, LSEG Refinitiv data

“The OVX index, which measures anticipated oil market volatility, just as the VIX index does for stock markets, trades at 47, well above its historic average of 37. That suggests oil traders remain on a state of high alert, even if equity prices are not putting much, if anything, of a geopolitical premium on hydrocarbon prices.”

The OVX index, which measures anticipated oil market volatility, just as the VIX index does for stock markets, trades at 47, well above its historic average of 37. That suggests oil traders remain on a state of high alert, even if equity prices are not putting much, if anything, of a geopolitical premium on hydrocarbon prices.

OVX index stands above historic averages

Source: CBOE, LSEG Refinitiv data

It is to be hoped that such complacency does not lead to shocks further down the road.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.