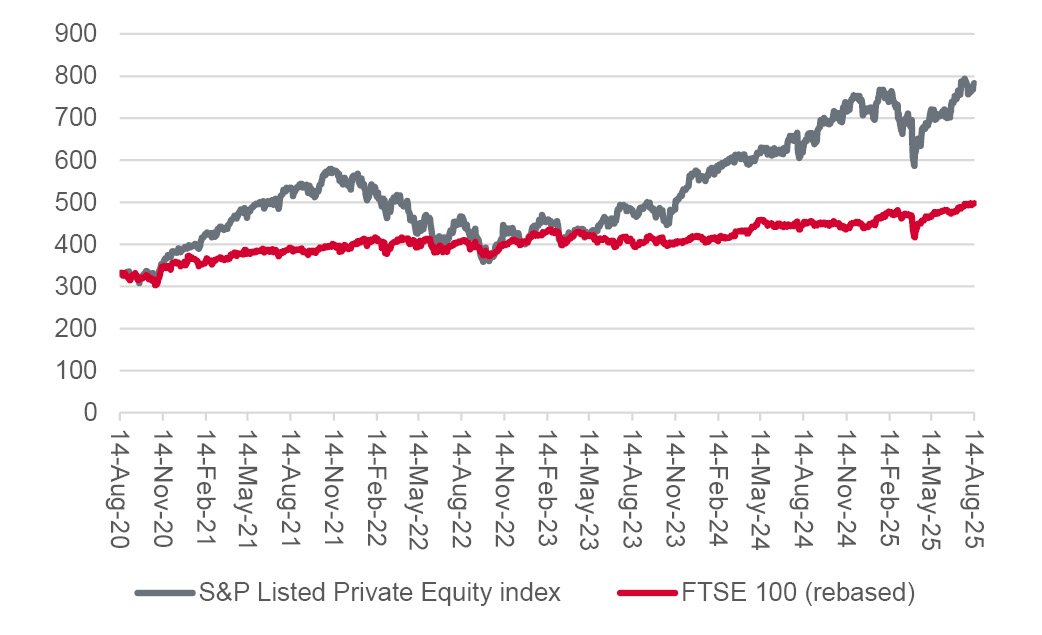

They say that mood follows price, and in this respect, it is easy to see why private markets, and private equity in particular, are garnering so much attention, from Downing Street downwards. Even as the FTSE 100 crosses the 9,000 mark for the first time and flirts with new all-time highs, the capital return from the UK’s leading index over the past five years is 50%. By contrast, the S&P 500 Listed Private Equity Index has ripped higher by more than 130%.

Granted, the FTSE 100 has been a happy hunting ground for income seekers over that time, and the total return is far more pleasing. The ‘Leeds Reforms’ proposed by Chancellor of the Exchequer Rachel Reeves do focus on public markets, as part of a wider plan to promote investment, deregulate and boost overall economic growth, but the bigger changes may lie in the prospect of permitting greater access to private markets, especially for retail investors.

The idea is that retail investors will be able to buy Long-Term Asset Funds (LTAFs), open-ended funds that offer exposure to long-term private markets, including private credit and private equity. The question now is whether this is an opportunity to be embraced or spurned.

“The performance of the private equity asset class explains why it looks such a beguiling option and potential portfolio diversifier beyond the standard options of equities, fixed income, commodities, property and cash.”

The performance of the private equity asset class explains why it looks such a beguiling option and potential portfolio diversifier beyond the standard options of equities, fixed income, commodities, property and cash.

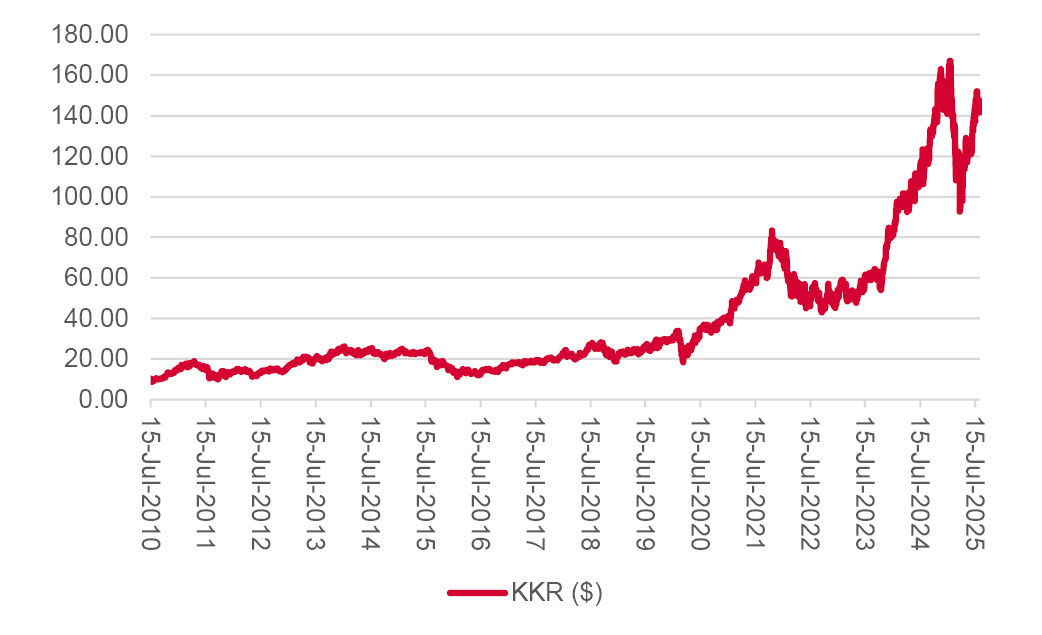

The S&P Listed Private Equity index is a good benchmark for that, and it shows how advisers and clients can already get access to the asset class through some of the index’s constituents, including Canada’s Brookfield, America’s Blackstone and KKR, Sweden’s EQT and the UK’s very own 3i, should they feel they fit with their overall strategy, target returns, time horizon and risk appetite.

Private equity has performed strongly as an asset class

Source: LSEG Refinitiv data.

And there are risks to consider, including the following:

“Private equity is long only. The funds own companies. It just happens to be all of them rather than a shareholding. In the event of a market or economic dislocation, they cannot go short or hedge.”

Private equity firms’ shares were not immune to prior equity market bouts of volatility

Source: LSEG Refinitiv data.

“There is a danger that new-found buyers of the asset class could simply be providing exit liquidity to shrewd sellers.”

This final point is particularly pertinent because the environment is now different from the one in which private equity’s strong, historic returns lie. Private equity’s use of debt to leverage returns looks great when interest rates are zero, but perhaps less so now benchmark borrowing costs are something vaguely akin to ‘normal.’

The debt piled onto acquired businesses now comes with a cost and could start to smother them, as the interest bills suck away cash that could otherwise be used to invest in the competitive position of the acquired company. A couple of UK supermarkets could be potential examples of this, after the acquisitions of Morrisons and Asda, as Aldi and Lidl (not to mention Tesco) continue to eat their lunch.

“Falling interest rates could yet provide a fresh tailwind for private equity so it may not pay to be too cynical.”

Falling interest rates could yet provide a fresh tailwind for private equity so it may not pay to be too cynical. An onrush of inflation, thanks to the Trump growth agenda of lower energy prices, lower interest rates, lower direct taxes and deregulation, coupled with central banks keeping borrowing costs down, could force advisers and clients to spurn cash and seek multiple hide-outs, including the real assets and businesses owned by private equity. But in that instance, portfolio builders may have to bear in mind the Swiss investor and publisher Marc Faber’s dark assertion that, “When things are really broken, the price of everything goes up.”

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.