Oil prices have moved sharply in recent months as markets reacted first to conflict involving Iran and disruption risk around the Strait of Hormuz, and then to signs of de-escalation. This is a natural topic for advisers discussing recent market moves with clients. It also provides a useful example of how our active asset allocation has led us to hold direct sector positions in 2026, most notably US energy, which have helped deliver a better overall journey than purely passive market exposure.

We added exposure to US energy in January on valuation and diversification grounds. The position was not dependent on a single macro view. It offered potential support from several different scenarios, including stronger power demand linked to artificial intelligence infrastructure, renewed inflation pressure and geopolitical risk. That breadth of rationale was important. The aim was to add a diversifying source of return within US equities, rather than make a short-term call on the oil price.

That positioning was tested during the recent period of geopolitical stress. Energy behaved broadly as expected: it was supported when investors focused on supply disruption, inflation risk and the potential for a wider conflict, before easing as those risks receded. The recent fall in oil therefore needs to be seen in context. It does not invalidate the allocation; it shows the sector responding to the changing risks it was partly selected to help address.

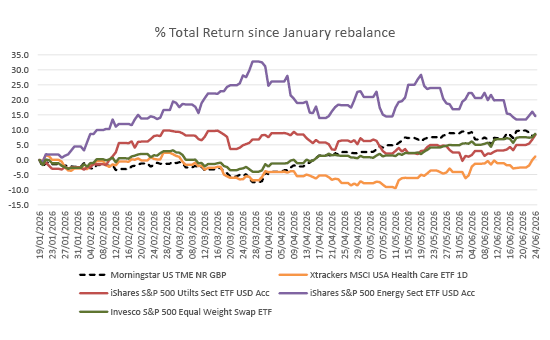

More importantly, energy has not been working in isolation. It has been part of a broader set of sector tilts designed to introduce different return drivers into portfolios. While energy has been more sensitive to oil and geopolitical risk, utilities have provided defensive support in lower-risk profiles, and healthcare has more recently begun to contribute across a wider range of portfolios. Taken together, these allocations have helped smooth the path for clients rather than relying solely on the direction of the broad US equity market.

Source: Morningstar Direct, Total Return 19/01/26 – 24/06/26 in GBP

The broader picture is that the sector mix has helped improve the overall shape of returns. Different positions have contributed at different points, which is exactly the purpose of diversifying across multiple rationales rather than relying on one theme to do all the work.

Energy is therefore only one part of the story, even if oil is the most visible short-term talking point. Across our US equity exposure, the combination of broad market holdings and selected sector positions has helped create a more balanced journey through market volatility.

This is the practical case for active sector allocation. Broad equity indices can become heavily influenced by a small number of themes or companies. Selective sector exposure can introduce different return drivers, reduce reliance on a narrow set of market leaders and provide a better experience for clients during periods when market leadership changes.

The recent move in energy does not undermine the rationale for holding the sector. It reinforces the need to look at portfolio construction in the round. Energy strengthened when geopolitical and inflation risks rose, and softened when those risks receded. At the same time, other sector allocations have helped support portfolios in different ways. That combined effect is the key message for advisers.

In our view, US energy continues to offer attractive longer-term prospects, supported by valuation discipline and the potential for demand growth linked to the energy needs of a more digital economy, amongst other factors. But the more immediate lesson is broader: thoughtfully combined sector allocations can help clients experience a smoother and more diversified journey through equity market volatility.

For clients, oil price volatility can make US energy the most visible part of the story. For advisers, the more useful message is that portfolios do not need to rely on one sector, one theme or one market driver. Recent volatility in US energy is a helpful case study, but the stronger point is that the combined effect of energy, utilities, healthcare and broad market exposure has helped provide a better journey through a changing market environment.

Past performance is not a guide to future performance and some investments need to be held for the long term.

This area of the website is intended for financial advisers and other financial professionals only. If you are a customer of AJ Bell Investcentre, please click ‘Go to the customer area’ below.

We will remember your preference, so you should only be asked to select the appropriate website once per device.